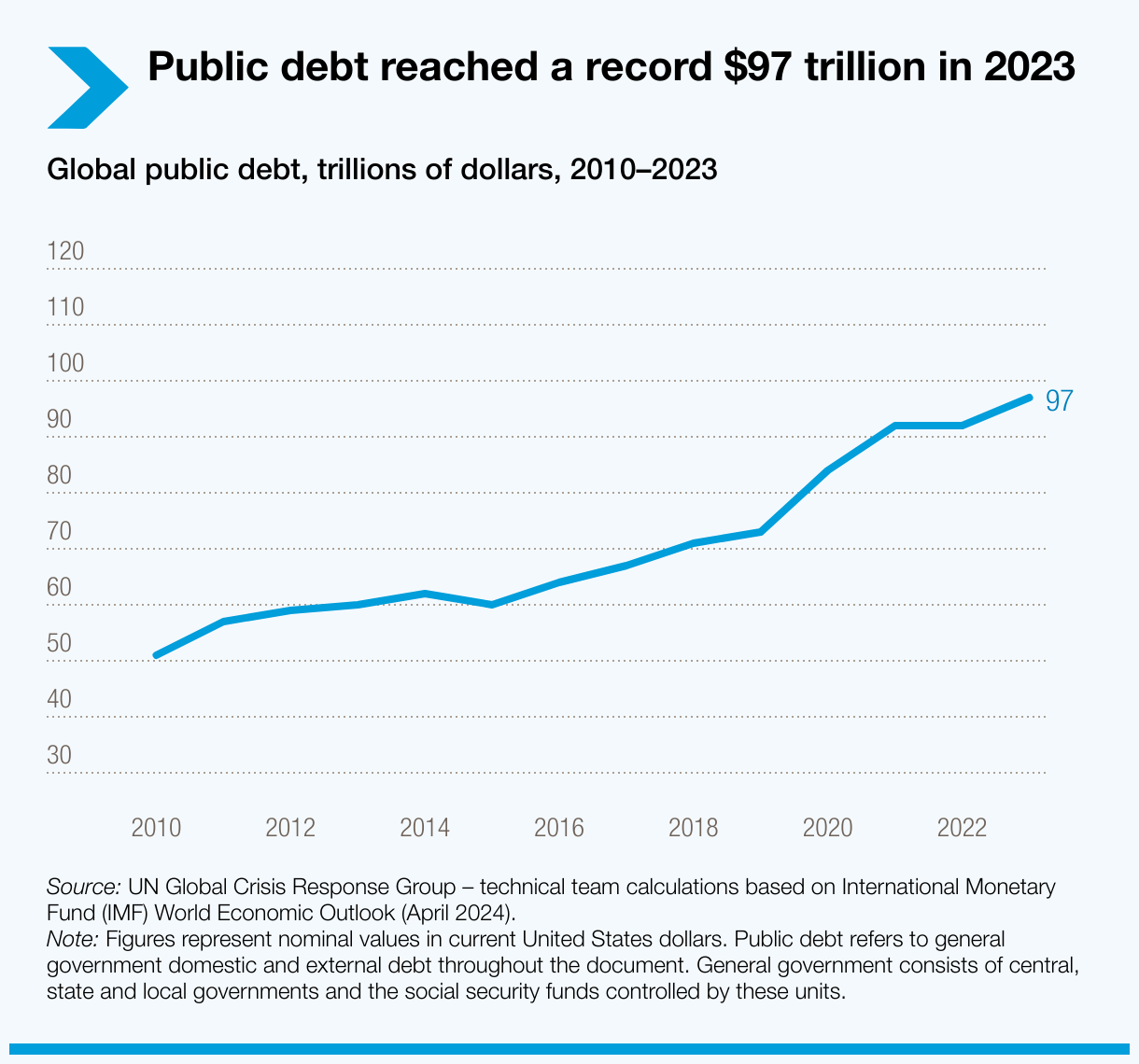

La deuda pública mundial se ha duplicado desde 2010, alcanzando un máximo histórico de $97 billones en 2023. Más del 40% de la población mundial vive en países que gastan más en pagos de intereses de la deuda que en educación o salud.

En el marco del 60 aniversario de ONU Comercio y Desarrollo (UNCTAD), es importante examinar los temas que marcarán el futuro del comercio y del desarrollo.

La serie "Avanzando juntos" explora temas cruciales que presentan grandes promesas y significativos desafíos para los países en desarrollo, como la deuda pública.

La serie Avanzando juntos

- Navegando los crecientes desafíos de la deuda pública y externa

- Hacer que el comercio electrónico y la economía digital funcionen para todos

- Construir economías más diversas y resilientes

- Hacer que el comercio funcione mejor para el planeta

El aumento de la deuda pública restringe profundamente el crecimiento económico y limita la inversión en sectores críticos para el desarrollo, como la infraestructura, la salud y la educación. Una alta deuda pública también conduce a un ciclo vicioso de endeudamiento y reembolso, arriesgando incumplimientos y crisis económicas, como se vio durante la crisis de la deuda latinoamericana de los años 80, un período a menudo referido como la “década perdida”.

La deuda pública mundial se ha duplicado desde 2010, alcanzando un máximo histórico de 97 billones de dólares en 2023. Actualmente, alrededor de 3.300 millones de personas – más del 40% de la población mundial – viven en países que gastan más en pagos de intereses de la deuda que en educación o salud.

Además, en 2023, un histórico de 54 países en desarrollo, casi la mitad de ellos en África, dedicaron un mínimo del 10% de los fondos gubernamentales al pago de intereses de la deuda.

"Hay una tendencia alarmante en la comunidad internacional a considerar sostenibles las deudas en el mundo en desarrollo porque, después de algún sacrificio, pueden ser pagadas," dice Rebeca Grynspan, Secretaria General de ONU Comercio y Desarrollo.

"Esta visión pasa por alto las comidas saltadas, la inversión en educación no realizada y la falta de gasto en salud, por no mencionar la reducción de la inversión en infraestructura, que forzosamente dan lugar a los pagos de intereses."