In the era of hyperglobalization, debt has become a dominant driver of global growth but has failed to deliver a strong surge in productive investment, instead fuelling financial speculation, according to UNCTAD’s Trade and Development Report 2019.

In this environment, developing countries have seen debt transformed from a long-term financing instrument to help unleash their future growth potential into a potentially high-risk financial asset subject to the vagaries of international financial markets and proliferating short-term creditor interests.

This is of particular concern given that structural transformation in developing countries implied by a Global Green New Deal and reflected in the Sustainable Development Goals (SDGs) will require an unprecedented scale-up of financing productive investment in these countries – at conservative estimates in the range of at least US$2 trillion to $3 trillion per year to meet only the most basic SDGs on time.

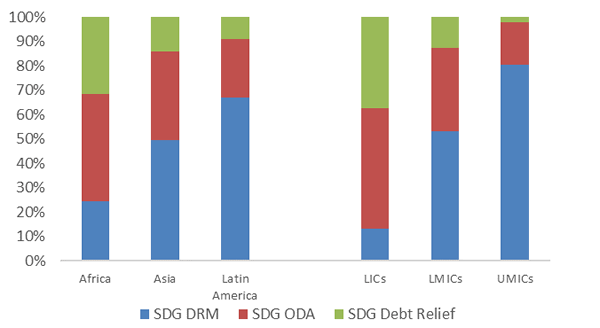

As the report shows, for a sample of 30 developing countries across all income categories, given flagging multilateral support, developing countries would either see their debt-to-GDP ratios rise to around 185% on average by 2030, or else they would require average annual GDP growth rates of around 12% to meet the investment needs of only the first four SDGs (eliminate poverty, promote nutrition, good health and quality education).

Neither scenario is remotely realistic. Instead, putting debt financing in developing countries on a more sustainable footing will require concerted and urgent multilateral action to release developing countries from current debt traps, support improved domestic resource mobilization and promote environmental protection alongside developmental growth.

Actions suggested include:

A global SDG-related concessional lending programme for developing countries designed to allow participant countries to borrow on concessional terms and an additional lending facility designed specifically to cover the external share of gross financing needs of the public sector until 2030. A global SDG Fund to serve this purpose could be capitalized by donor countries paying in their (unfulfilled) commitments to the official development assistance target of 0.7% of gross national income over the past four decades.

Expanding Special Drawing Rights linked directly to the provision of public goods in developing countries, including environmental protection and the implementation of SDGs uncontentionally recognized as public goods and therefore relying on public funding. This would provide an additional and goals-focused flexible and scalable debt-financing mechanism to support environmentally friendly and sustainable late development.

A dedicated SDG-related debt relief programme to alleviate immediate liquidity constraints and help put debt sustainability in developing countries on a long-term footing without strict policy conditionalities or limiting eligibility criteria.

Stronger regional monetary cooperation among developing countries to refinance and promote intraregional trade and develop intraregional value chains, moving beyond regional reserve swap and pooling agreements to promote the full-scale development of regional payment systems and internal clearing unions.

A rules-based framework to facilitate an orderly and equitable restructuring of sovereign debt that can no longer be serviced according to original contracts, and governed by a set of agreed principles and body of international law. The report suggests first steps towards such a rules-based internationally recognized framework for the resolution of sovereign debt restructurings, including stand-still, debtor-in-possesion financing and lending into arrears provisions.