The accountability system

UNCTAD is part of the United Nations Secretariat and operates under the United Nations Secretariat accountability framework. Key elements are described below.

A good overview of the accountability framework can also be found in annex 1 of the Secretary General's report "Towards an accountability system in the United Nations Secretariat" (A/64/640).

The accountability system of UNCTAD has seven main components:

1. The United Nations Charter

The basis of the UNCTAD accountability system is the United Nations Charter. According to the Charter, Member States are responsible for giving mandates (directives, priorities and targets) to the secretariat through the resolutions and decisions. The UNCTAD Secretary-General is responsible for implementing these mandates and reporting on outcomes and resources used.

UNCTAD's mandates come from the General Assembly and its subsidiary organs, ECOSOC and other conferences. The UNCTAD quadrennial conference (a subsidiary organ of the General Assembly) sets the four-year mandate and work priorities of the UNCTAD secretariat. UNCTAD also has its own separate governing body, the Trade and Development Board, established as a permanent subsidiary organ of the Conference, to oversee the work of the secretariat between quadrennial sessions.

In discharging responsibilities, the UNCTAD Secretary-General reflects these mandates in the programme and planning documents of the organization (the strategic framework and the programme budget). Programme managers and individual staff members — down the chain of responsibility —prepare their respective workplans with the purpose of achieving the results established therein.

2. The strategic framework and the programme budget

One of the main elements of the accountability system is the UNCTAD programme planning and budget documents reflecting the mandates of Member States and represent the commitments of UNCTAD to implement those mandates with the approved resources.

As UNCTAD is part of the UN Secretariat, the basic principles of the Organization’s budgetary process are set out in Article 17 of the Charter of the United Nations, which provides that the General Assembly shall consider and approve the United Nations budget, and apportion the expenses of the Organization among the States Members of the United Nations. As chief administrative officer of the Organization, the UN Secretary-General is responsible for preparing and submitting a budget proposal to cover the costs of the activities of the United Nations Secretariat funded under the regular budget. The Organization relies on Member States to provide adequate resources and to pay their contributions on time and in full.

The Committee for Programme and Coordination and the Advisory Committee on Administrative and Budgetary Questions, review the planning and budgeting proposals formulated by the Secretary-General, in accordance with their respective mandates, and submit their conclusions and recommendations, through the Fifth Committee, to the General Assembly for consideration and approval.

The process is also governed by the United Nations Regulations and Rules Governing Programme Planning, the Programme Aspects of the Budget, the Monitoring of Implementation and the Methods of Evaluation (ST/SGB/2018/3) provide the legislative directives established by the Assembly governing the planning, programming, monitoring and evaluation of all activities undertaken by the United Nations, irrespective of their source of financing.

With the aim of continued strengthening of planning, budgeting and financial management of the United Nations, in 2018 the UN Secretary-General, in his reports to the General Assembly (A/72/492 and A/72/492/Add.1) on shifting the management paradigm in the United Nations proposed that the biennial budget be replaced with an “integrated annual programme budget”, in order to allow for the preparation of more realistic and responsive programme plans and resource estimates.

The proposed change from a biennial to an annual budget period was approved in 2018 on a trial basis, beginning with the programme budget for 2020, as per resolution A/RES/72/266. In December 2022, as per resolution A/77/673, the General Assembly decided to lift the trial period effective from 2023, and requested the Secretary-General to continue with the submission of the programme budget according to an annual cycle.

In line with this, the UNCTAD annual programme budget document reflects the translation of legislative mandates into its programme of work for the budget period, for each subprogramme, reflecting the following:

- The overall orientation;

- The strategy for the implementation of related mandates;

- The results to which it has contributed in the previous budget period, as compared with the original plan for the same year (two carried-forward results per subprogramme);

- Lessons learned and prior-period programme performance (one prior performance result per subprogramme);

- Planned results for the proposed budget period (one planned highlighted result per subprogramme);

- Main deliverables (outputs) planned for the budget period and achieved in the prior period;

- Overview of proposed post and non-post resource requirements for the budget year.

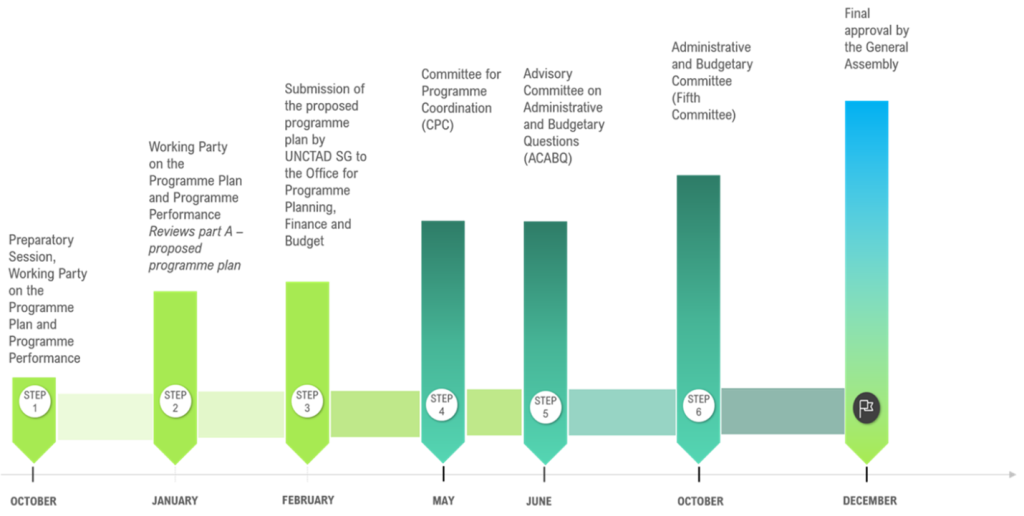

The planning and budgeting process for UNCTAD consists of the preparation, submission, consideration and approval of the document, as follows:

Part A, the draft annual programme plan is prepared in consultation with UNCTAD Member States, in the framework of the Preparatory Session of the Working Party, based on their priorities and needs, and which agree on strategic directions, expected accomplishments and deliverables. The programme plan is subsequently formally reviewed by the Working Party on the Programme Plan and Programme Performance and approved by the Trade and Development Board. It is further submitted, as Section 12 “Trade and Development” of the UN Secretariat fascicle, for the review of the Committee for Programme Coordination (CPC) and the Fifth Committee, and adoption of the General Assembly.

Part B, proposed annual programme budget, is prepared by UNCTAD in line with the budget instructions issued by the Office for Programme Planning, Finance and Budget, reflecting the priorities of the UN Secretary-General. The budget proposal is further submitted to the Controller, and reviewed by the Advisory Committee for Administrative and Budgetary Questions (ACABQ) and the Fifth Committee for recommendation to the General Assembly for adoption.

The final issued document contains both Part A and Part B, as part of Proposed programme budget document, Part IV International cooperation for development, Section 12 Trade and development, Programme 10 Trade and development.

Proposed programme budget documents: 2020 | 2021 | 2022 | 2023 | 2024 | 2025

The UNCTAD Secretary-General is responsible for achieving the objectives and delivering the results and activities as approved in the Proposed programme budget document for Section 12 “Trade and Development”, by the General Assembly.

The annual programme budget is set against the specific results and deliverables designed to contribute to the achievement of the strategic objectives, in line with the annual programme plan, and reflects the allocation of human and financial resources required to implement these activities.

Results and performance refer to the obligation of the Organization to deliver on the outcomes and outputs reflected in the programme planning and budget documents and to report accurately on those results to Member States.

This is done through the following existing mechanisms and tools:

Organizational performance, presented in the budget documents, including the results that were achieved in the last completed budget cycle

As part of the Secretariat, UNCTAD presents in the budget documents the results that were achieved by the Organization in the last completed budget cycle. This information includes highlighted results to which UNCTAD contributed during the budget cycle and implemented deliverables, including the results of the evaluations and self-evaluations carried out during the period and the lessons learned. This information is also presented to UNCTAD Member States, in the framework of the Working Party on the Programme Plan and Programme Performance.

Monitoring performance , results and the implementation of the annual programme plans and projects through Umoja Extension 2

Programme managers at the level of each subprogramme (division) are accountable for the delivery of outputs and results contained in the approved programme budget. They are also responsible for fairly and accurately reporting on this through enterprise resources planning system Umoja, Strategic Management Application (SMA). It allows the monitoring of the implementation of the approved Annual Results Frameworks (ARF) against set targets and commitments, as per approved proposed programme budget document.

3. Delivering results and performance

Results-based management (RBM) In 2006, the General Assembly mandated the United Nations Secretariat to implement RBM (A/RES/60/257). RBM is an overall approach to managing projects and programmes that goes beyond the achievement of outputs (publications, training workshops, intergovernmental meetings, etc.) to focus on their results (did we achieve what was intended with these outputs, what was the impact, how can we adapt or change to have greater impact, and so on).

It supports better performance and greater accountability by applying a clear logic: plan, manage and measure your intervention with a focus on the results you want to achieve. For UNCTAD, this means:

- Defining measurable results and the means to achieve those results;

- Aligning planning, programming and budgeting to desired results;

- Establishing monitoring, reporting, knowledge management and evaluation systems to track and assess the achievement of results; and

- Establishing a change management process that promotes organizational and cultural reforms necessary for the use of results information for learning, improvement and accountability.

The benchmarks and methodologies for implementing RBM have evolved over the last decade.

While key policies and standards on which to build a more results-oriented Secretariat already exist, the United Nations Secretary General has acknowledged that the availability of support, consistent guidance and procedures, tools and training needs to be increased (A/64/640, p.31).

On-going initiatives to improve RBM Therefore, in line with the RBM principle of continuously assessing what works/what does not and improving to deliver more effective results, UNCTAD has several on-going initiatives to improve the implementation of RBM throughout the organization.

For technical cooperation activities, the UNCTAD Deputy Secretary General launched on 1 July 2016 the Technical cooperation results framework (PDF) and a set of 'minimum requirements for RBM' (PDF). These are basic steps to be taken to ensure a focus on results throughout the project cycle. For example,

- In-depth analysis of how the project can sustainably address the problems related to UNCTAD's mandate,

- UNCTAD projects that add value to the market for technical cooperation,

- Clearly defined indicators to measure the impact of UNCTAD projects,

- Systematic and comprehensive monitoring and evaluation of results,

- Regular reporting on results, including to our member states, and

- Lessons about what works/what does not reflected in future projects.

Prior to the minimum requirements, implementation of these steps was ad hoc. The minimum requirements serve, inter alia, to:

- bring all programme managers to the same minimum level for RBM;

- offer sufficient flexibility to managers, while ensuring a high standard for RBM;

- increase the relevance, efficiency, effectiveness (including impact) and sustainability of technical cooperation projects;

- systematise the collection and analysis of evidence on results; and

- increase evidence-based management decision-making.

Implementation of the minimum requirements supported by internal guidelines, project document templates, checklists to assess whether the minimum requirements are met, and clearly defined internal roles and responsibilities at each stage of the project cycle.

By the end of 2016, UNCTAD is aiming to also launch initiatives to improve RBM for its research and analysis work, and support to intergovernmental meetings.

4. Evaluation and learning

The Independent Evaluation Unit (IEU)

Evaluation is a core function of the United Nations Conference on Trade and Development (UNCTAD), supporting effective programme planning, design, and implementation. It serves as a key accountability tool, strengthening the organization's credibility and relevance by providing evidence-based insights for informed decision-making.The UNCTAD Evaluation Policy defines the guiding principles, institutional framework, roles and responsibilities, and key processes and mechanisms for evaluation at UNCTAD. It applies to all projects and programmes under the regular budget as well as activities funded from extra-budgetary resources.

The Independent Evaluation Unit (IEU) is the custodian of UNCTAD's Evaluation Policy and is responsible for ensuring that evaluations are independent, credible, and of high quality. It establishes evaluation standards, ensures quality assurance, tracks management responses, disseminates findings, and fosters accountability and learning.

Evaluations at UNCTAD follow the norms and standards established by the United Nations Evaluation Group (UNEG), an inter-agency professional network that brings together all UN evaluation units to ensure system-wide collaboration and quality in evaluation across the UN system.

Evaluations conducted by UNCTAD are of two main types:

- Independent Evaluations - managed by the Independent Evaluation Unit and conducted by IEU or external professional evaluators. These evaluations can be requested directly by donors or member States through the Working Party or commissioned by the UNCTAD Secretary-General. An independent terminal evaluation is required for any project with a budget of USD 1 million or above, or if requested by the funding entity for projects with a budget below USD 1 million.

- Self-Evaluations - managed by the programme or project teams themselves, mainly for the purpose of self-reflection and lessons learned. IEU can support self-evaluations and ensure minimum quality standards by reviewing the evaluation plan and questions, proposed methodology, and self-evaluation report.

Each year, IEU also conducts an independent evaluation of a UNCTAD subprogramme or division. Since 2012, the UNCTAD Working Party has reviewed one subprogramme evaluation annually on a rotating basis, ensuring regular coverage and compliance with the UN Secretariat's "Regulations and Rules Governing Programme Planning, the Programme Aspects of the Budget, the Monitoring of Implementation and the Methods of Evaluation" (ST/SGB/2018/3).

For questions or further information on evaluation at UNCTAD, please contact: evaluation@unctad.org

- Independent Evaluations - managed by the Independent Evaluation Unit and conducted by IEU or external professional evaluators. These evaluations can be requested directly by donors or member States through the Working Party or commissioned by the UNCTAD Secretary-General. An independent terminal evaluation is required for any project with a budget of USD 1 million or above, or if requested by the funding entity for projects with a budget below USD 1 million.

5. Internal systems and controls

In achieving our objectives, UNCTAD staff members respect the regulations, rules and policies and follow the processes and procedures (i.e. the set of internal systems and controls) that guarantee the correct functioning of the organization.

These systems and controls provide reasonable assurance regarding operational effectiveness, adequate resource utilization, reliable financial reporting and compliance with relevant regulations, rules and policies. They include:

- Staff Regulations and Rules and the Human Resources Handbook;

- Financial Regulations and Rules and the Finance Manual;

- Organizational systems for the selection and contracting of personnel;

- The Ombudsman and/or administration of justice process to guarantee fairness in the functioning of the internal systems and controls.

UNCTAD also has a system of segregation of duties to strengthen internal controls and reduce the risk of errors and irregularities. Under this system, no single individual has control over all phases of a decision or transaction that involves organizational resources. This reduces the possibility that a single individual can breach the regulations, rules or procedures causing financial loss to the organization.

6. Ethical standards and Integrity

The core values and principles governing staff conduct and behaviour (ST/SGB/2002/13) are contained in the Charter of the United Nations, the standards of conduct for the international civil service, and the Staff Regulations and Rules. In addition, the Code of Ethics (A/64/316, annex) outlines the fundamental values and principles applicable to the discharge of official UNCTAD duties and responsibilities.

Additional information can be found on the Ethics Office website.

The Secretariat Ethics Office develops standards, training and provides confidential advice and guidance to staff on ethical issues such as conflicts of interest. The Office also oversees the ethics helpline, has responsibilities related to the protection of staff against retaliation for reporting misconduct or cooperating with duly authorized investigations, and administers the United Nations financial disclosure programme.

7. Independent oversight

Independent oversight of UNCTAD is carried out by four main bodies: the Office of Internal Oversight Services, the Joint Inspection Unit, the Board of Auditors and the Independent Audit Advisory Committee. A description of these four bodies follows.

The UN Secretariat Office of Internal Oversight Services (OIOS)

The mandate of OIOS is to promote good governance and accountability in the Organization by providing independent and objective oversight. It covers 38 UN Secretariat departments and programmes, as well as peacekeeping operations and special political missions. It is comprised of 1) internal audit, 2) inspection and evaluation, and 3) investigations. Internal audit and evaluation have a risk-based workplan that ensures cyclical coverage of UNCTAD. The Office looks at a range of areas e.g. internal controls, strategic planning, risk-management and programme performance. Audits, inspections and evaluations covering UNCTAD are either programme-based (e.g. Audit of UNCTAD projects on strengthening institution and capacity building in the area of competition and consumer protection) or theme-based (e.g. Evaluation of gender mainstreaming in the UN Secretariat). OIOS reports are public and reviewed by various UN governing bodies, including subsidiary bodies of the General Assembly and Economic and Social Council (such as the Committee for Programme and Coordination) and the Advisory Committee on Administrative and Budgetary Questions (ACABQ).Consult OIOS Internal Audit and Evaluation reports for more.

The UN Joint Inspection Unit (JIU)

Coverage of the JIU extends beyond the UN Secretariat to UN Funds, Programs and Specialized agencies. The JIU is the only independent UN oversight body mandated to conduct evaluations, inspections and investigations across the UN system. It reports to the General Assembly and to the 28 legislative organs of the specialized agencies and other international organizations within the United Nations system that have accepted its Statute (which includes UNCTAD). It is comprised of 11 Inspectors appointed by the General Assembly for a maximum of 10 years. The Unit has a strong focus on management and administration issues, but also reviews other system-wide issues of importance to the UN. Reports of the JIU can cover single organizations, multiple organizations or the UN system as a whole. They are addressed to the respective governing bodies of the organizations or to the Executive Heads. JIU reports often provide comparisons and good practices across the UN system.JIU reports are available here.

The Board of Auditors (BoA)

The BoA is the external auditor of the United Nations, mandated to certify the financial accounts of the UN Secretariat and the Funds and Programmes, and report its findings and recommendations to the General Assembly. It is comprised of the heads of the Supreme Audit Institutions from three Member States, with a non-consecutive term of six years each. BoA recommendations are aimed at strengthening accountability for the use of public resources and improving the delivery of international public services. It reports its findings and recommendations to the General Assembly through the Advisory Committee on Administrative and Budgetary Questions.BoA reports are available here.

The UN Independent Audit Advisory Committee (IAAC)

The IAAC serves in an expert advisory rather than operational capacity and assists the General Assembly in fulfilling its oversight responsibilities. It comprises five members (with a mix of UN, audit, private sector and geographic backgrounds) appointed by the General Assembly, for up to six years, to advise the latter on the scope, results and effectiveness of audit and other oversight functions; and on measures to ensure the compliance of management with audit and other oversight recommendations.IAAC reports are available here.