Global maritime trade grew by 2.4% in 2023, recovering from a 2022 contraction, but the recovery remains fragile.

Key chokepoints like the Suez and Panama Canals are increasingly vulnerable to geopolitical tensions, conflicts and climate change.

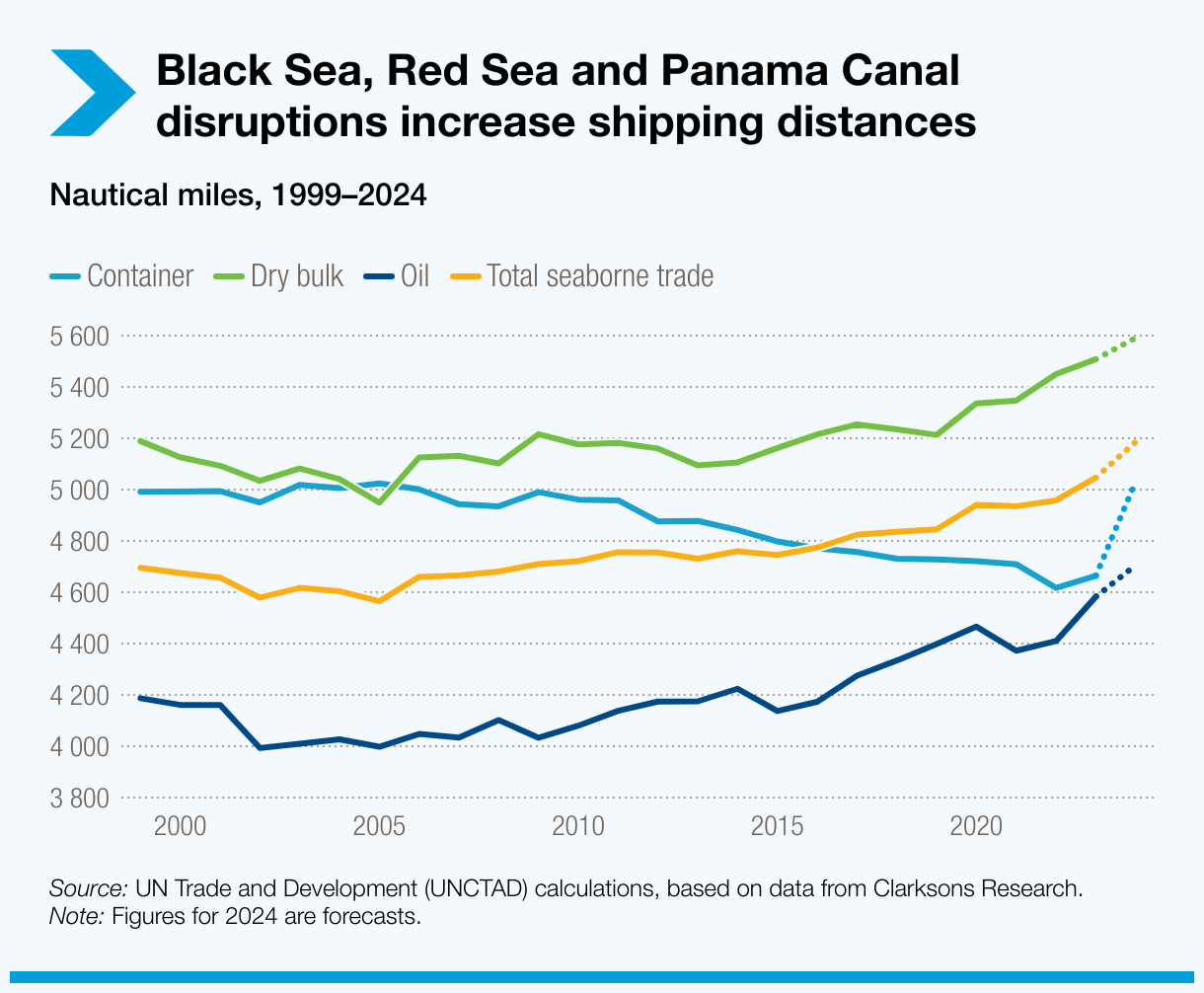

These disruptions are extending shipping routes, straining supply chains and raising costs, with profound impacts on food security, energy supplies and the global economy, as over 80% of world trade volume is carried by sea.

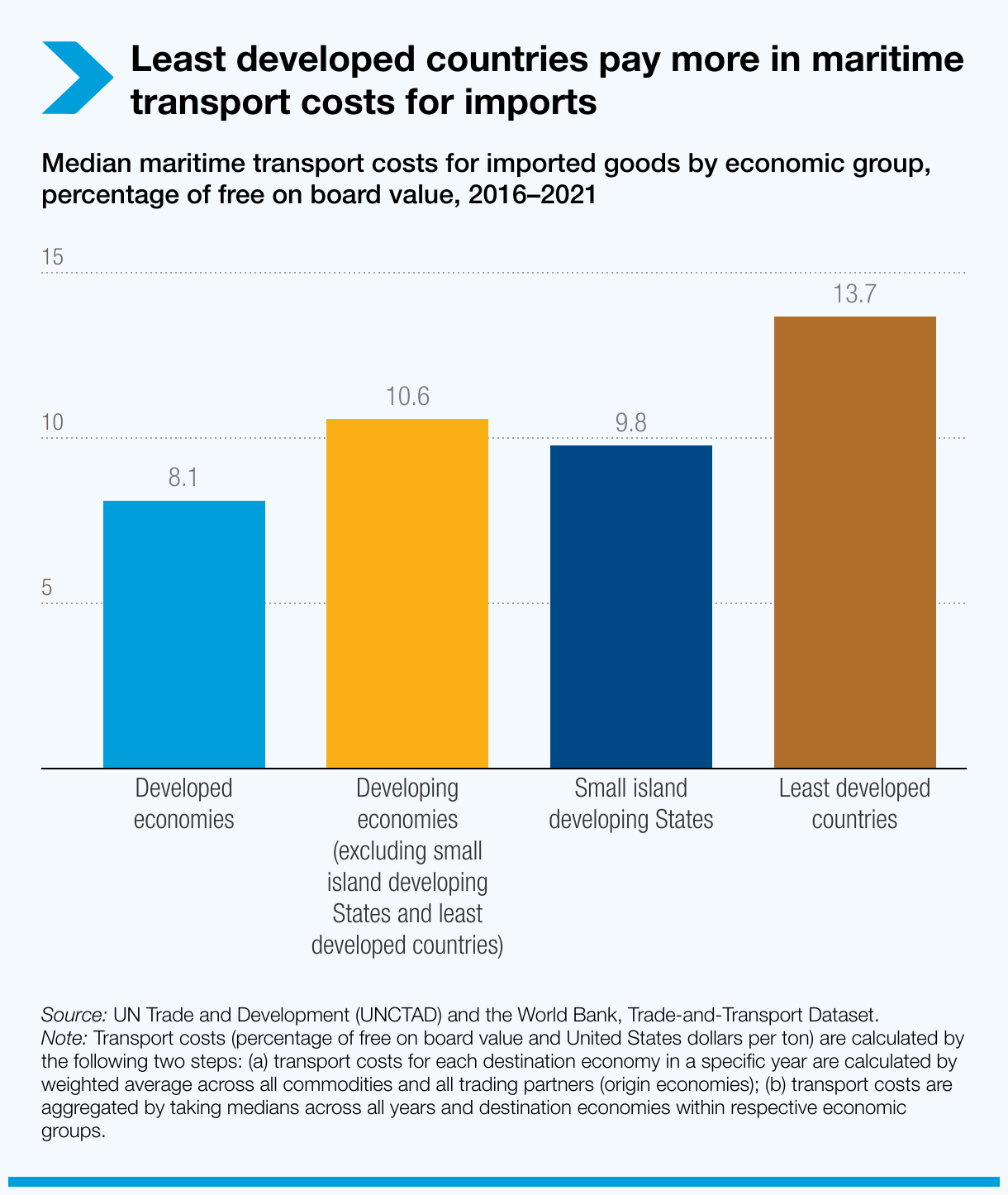

Vulnerable economies, especially small island developing States and least developed countries, are hit hardest by rising shipping costs from rerouted vessels.

The Review of Maritime Transport 2024 highlights these challenges, calling for urgent action to strengthen industry resilience, accelerate decarbonization and support vulnerable economies.

It underscores the need for new infrastructure that is sustainable and resilient, a faster transition to low-carbon shipping and a crackdown on fraudulent ship registrations to safeguard global trade.

Chokepoint vulnerabilities

threaten global supply chains

Food security, energy supplies and the global economy are at risk as key chokepoints like the Suez and Panama Canals and the Red Sea face growing pressure from geopolitical tensions and climate change.

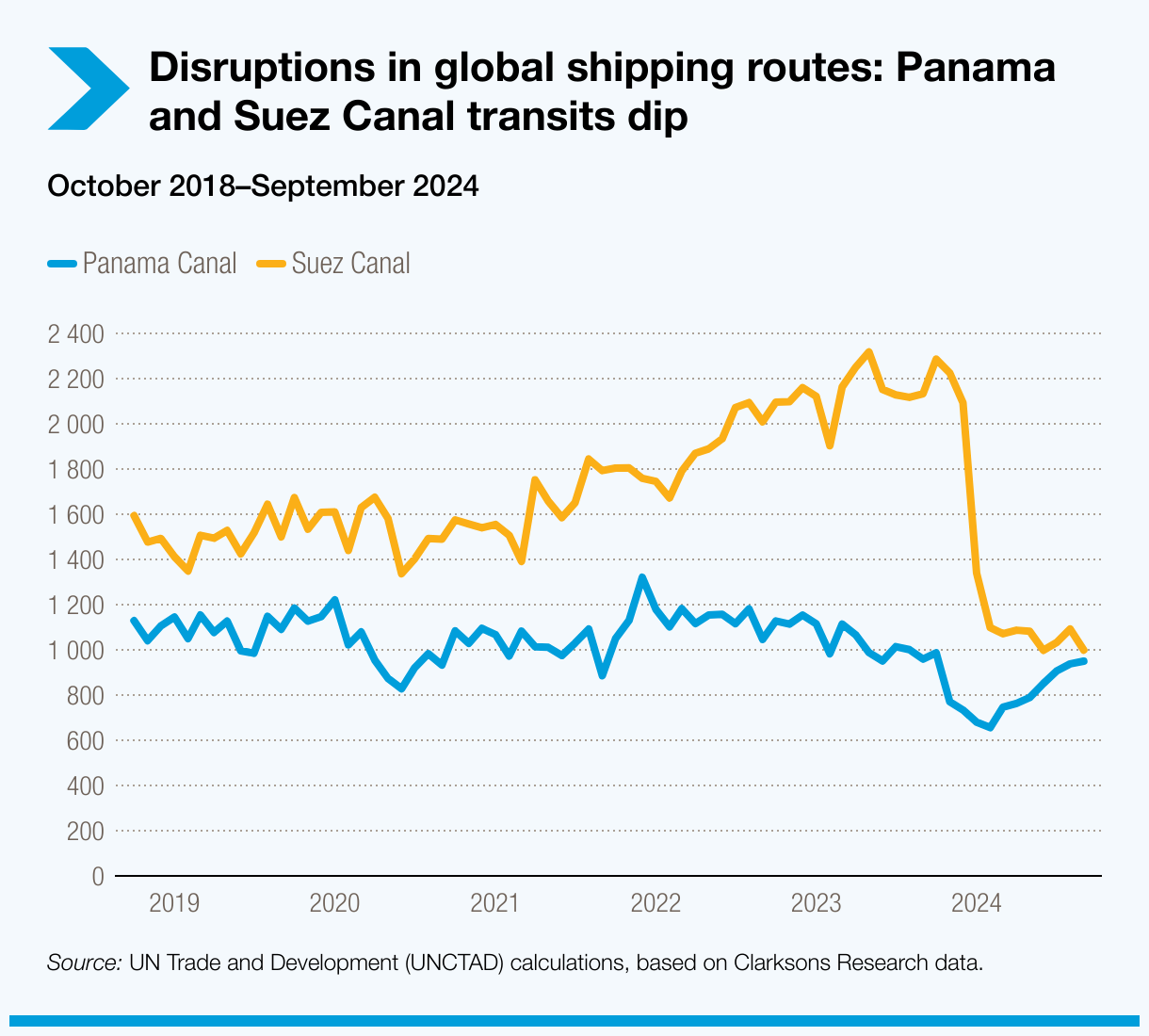

In 2023, ship transits through these canals dropped by about half, forcing costly rerouting around Africa's Cape of Good Hope.

By mid-2024, Suez transits fell further, with ship capacity (tonnage) crossing the Gulf of Aden down 76% and tonnage transiting the Suez Canal cut by 70%. Cape of Good Hope arrivals surged 89%. Longer routes raised global vessel ton-mile demand by 3% and container ship demand by 12%.

Longer routes have increased costs for fuel, wages, insurance and chartering while boosting emissions. For a 20,000-24,000 TEU vessel on the Far East-Europe route, CO2 emissions alone add $400,000 in costs under the European Union's Emissions Trading System.

Regional examples show the wider impact. East African nations like Djibouti and Sudan, reliant on the Suez Canal for a third of their trade, face severe disruptions. The Panama Canal disruption has increased sailing distances by 31% for affected routes.

Small island developing States, reliant on maritime imports, have seen shipping connectivity drop by 9% over the past decade, leaving them ten times less connected than the rest of the world.

UN Trade and Development calls for

-

1Strengthened international cooperation to stabilize trade routes, enhance resilience and minimize supply chain disruptions from geopolitical and climate-related risks.

-

2Improved monitoring systems for early detection of chokepoint disruptions and faster rerouting, as well as investment in early warning systems for ports.

-

3Support for regional trade to reduce reliance on vulnerable routes and boost intraregional supply chains.

-

4Enhanced global coordination to prevent protectionism and ensure open trade routes.

-

5Active support of all UN Member States and stakeholders for IMO efforts to combat fraudulent ship registration through better verification, information sharing and strengthening of the legal framework.

Maritime trade rebounds,

but geopolitical and climate risks persist

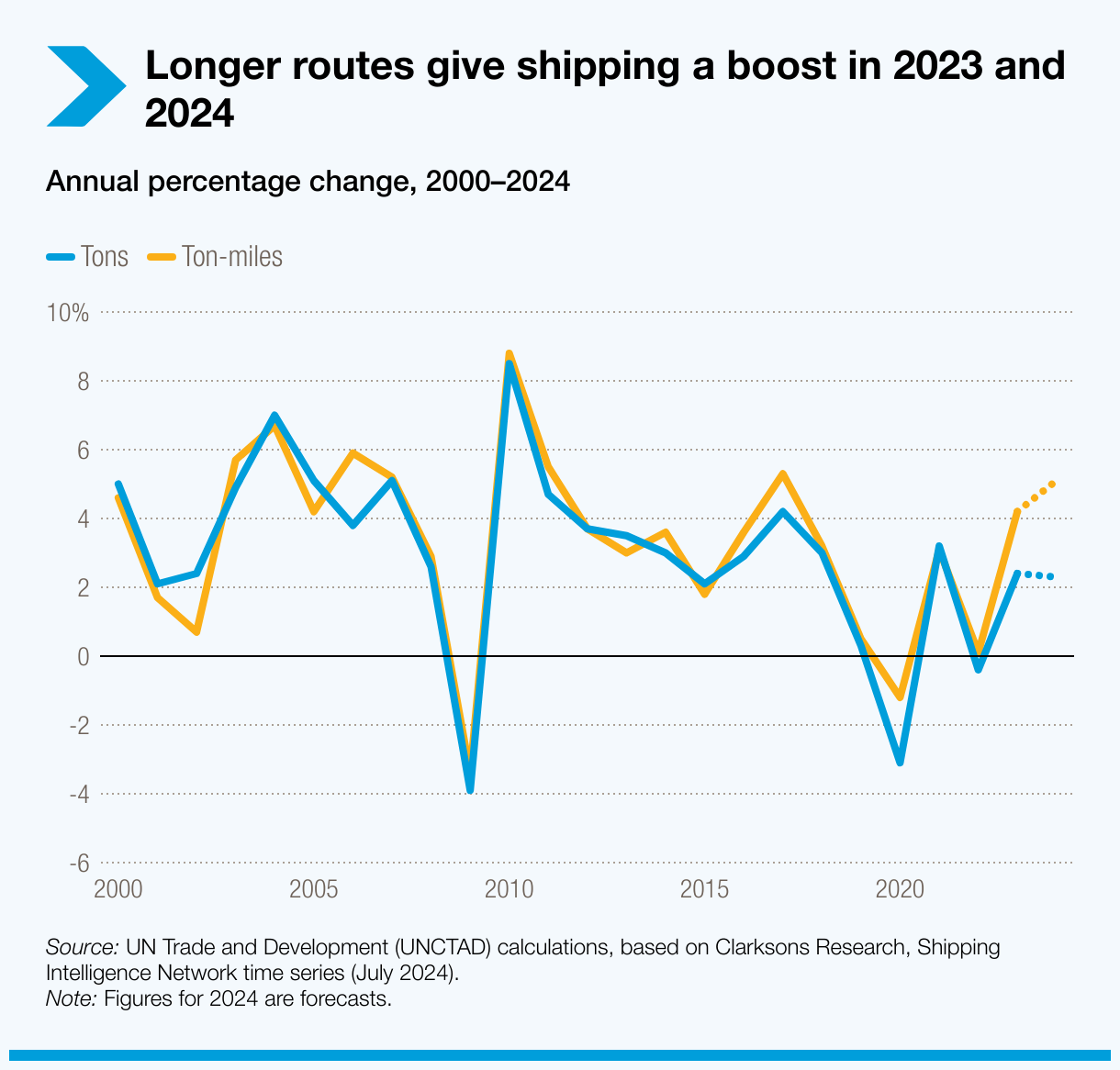

In 2023, global maritime trade grew by 2.4% to 12.3 billion tons, rebounding from the 2022 contraction. The sector is projected to grow by 2% in 2024 and an average of 2.4% annually through 2029.

However, soaring freight costs and an “exceptionally daunting operating landscape” driven by geopolitical conflicts and climate risks continue to weigh on a lasting maritime trade recovery.

Demand for iron ore, coal and grains remains strong, while the container trade – up just 0.3% in 2023 – is expected to rebound by 3.5% in 2024, contingent on supply chain stabilization.

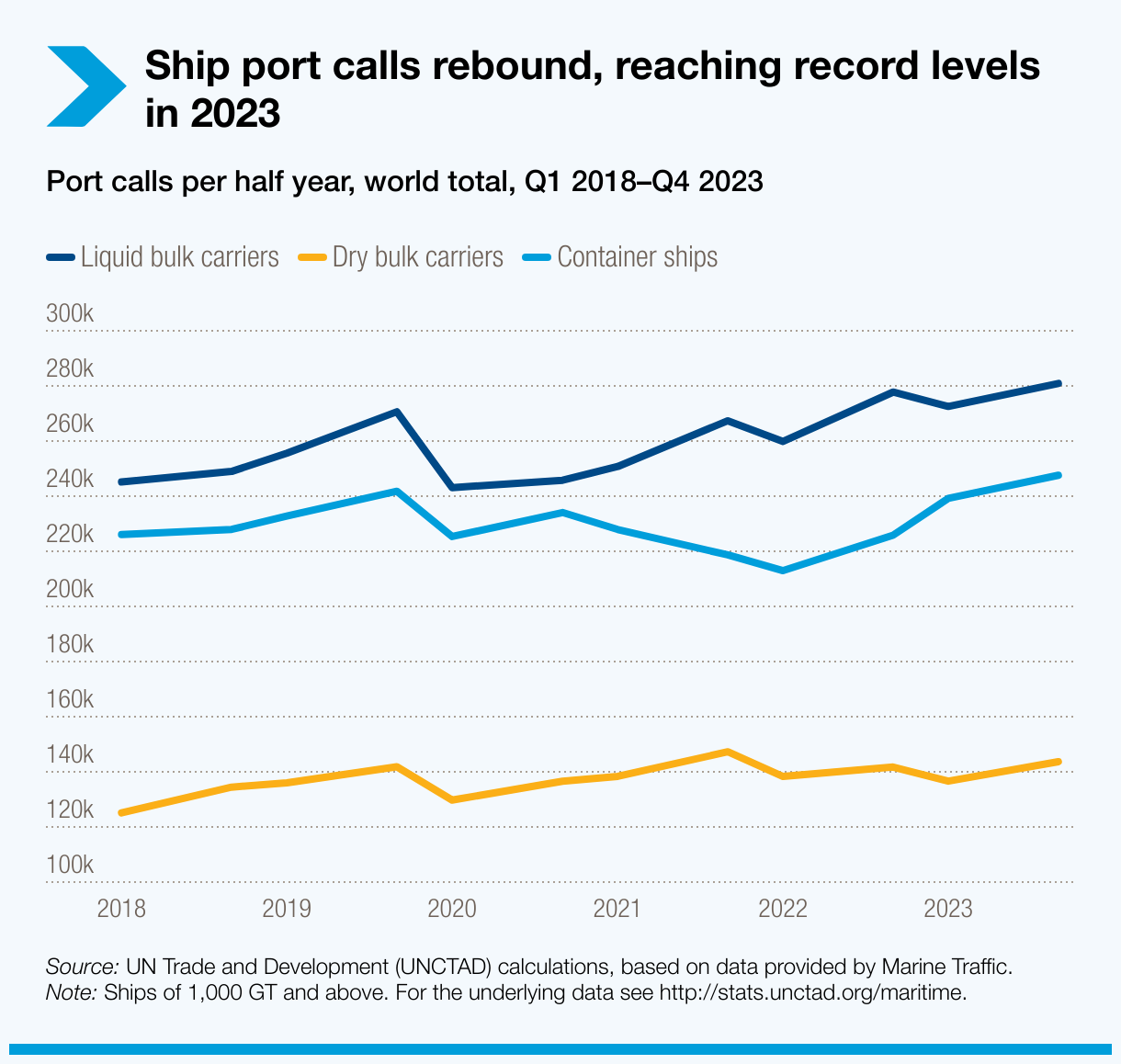

A record of almost 250,000 port calls by container ships in the second half of 2023 were driven by growing trade and longer routes, causing some congestion, especially in Asia, which handles 63% of global container trade.

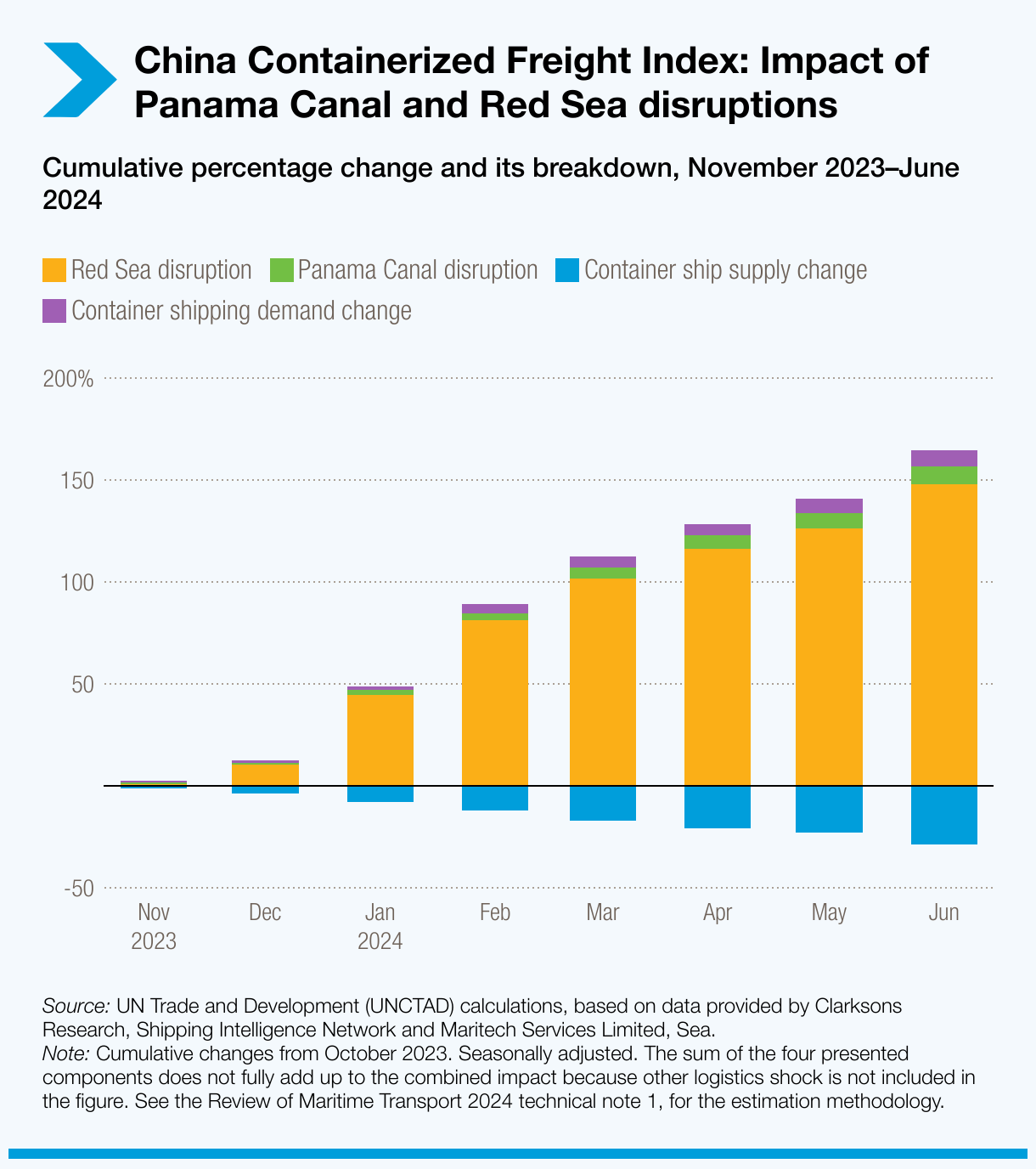

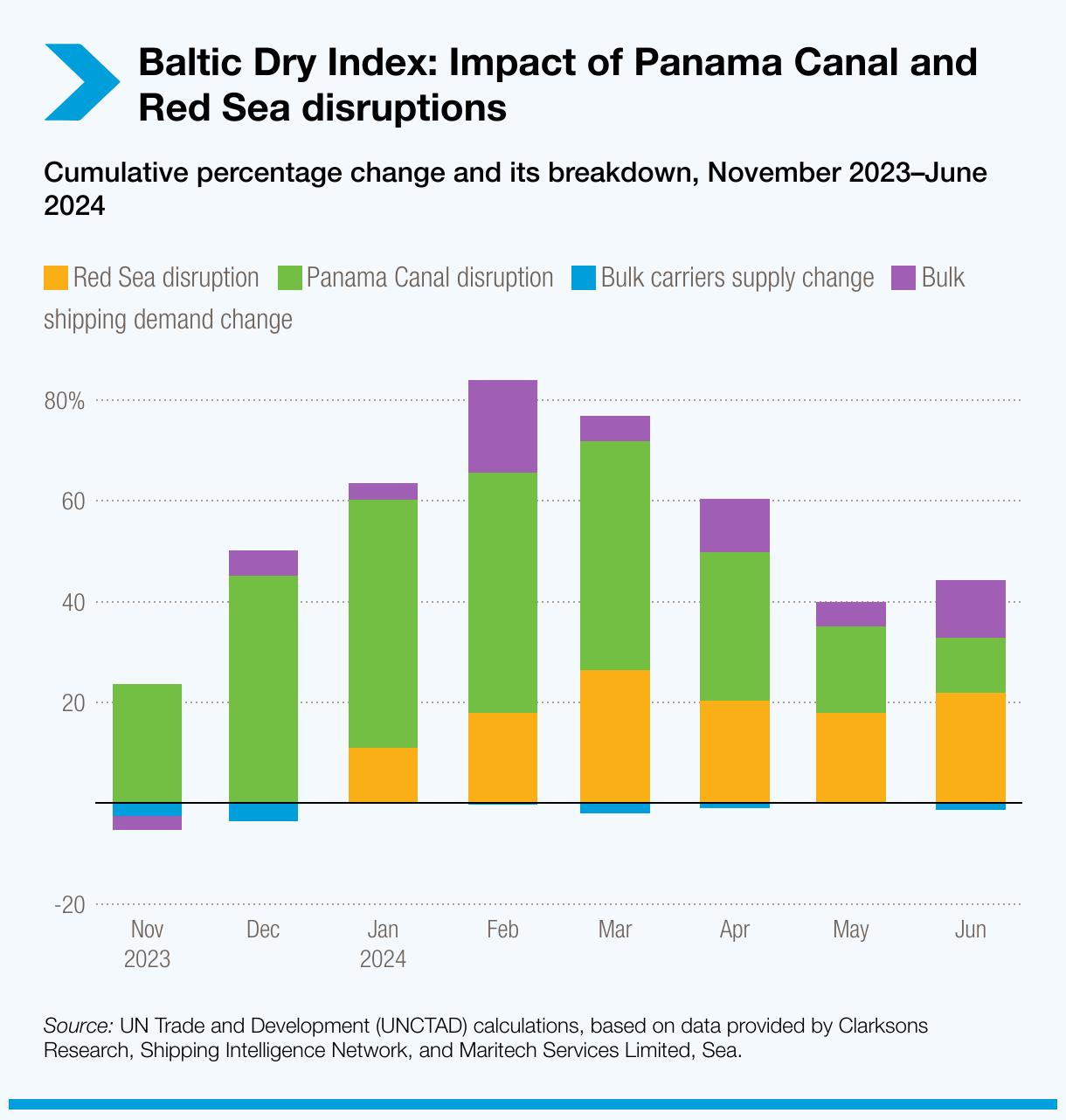

Ton-miles increased by 4.2% due to longer shipping distances from disruptions in key routes like the Suez and Panama Canals, further straining supply chains and adding to greenhouse gas emissions from shipping.

Concerns are growing about a rise in fraudulent ship registrations and registries undermining safety, security, pollution control and seafarer welfare. Ongoing efforts by the International Maritime Organization (IMO) to tackle fraudulent ship registration underscore the urgency of addressing this issue.

Demand for greener, more resilient supply chains is encouraging shorter, regionally focused trade, potentially boosting intraregional maritime connections.

See the key regional trends in Africa, Asia and Latin America.

UN Trade and Development calls for

-

1Urgent investment in resilient infrastructure at key chokepoints to minimize the impact of climate risks and conflicts.

-

2Diversification of shipping routes to reduce dependence on vulnerable maritime corridors like the Suez and Panama Canals.

-

3Increased international collaboration to monitor and mitigate risks at chokepoints, ensuring the free flow of goods.

-

4Enhanced support for SIDS and LDCs to alleviate the economic strain of rising shipping costs and safeguard food security.

Rising freight rates drive

inflation and threaten growth

Freight rates surged in 2024 due to rerouting, port congestion and rising operational costs.

By mid-2024, the Shanghai Containerized Freight Index (SCFI) had more than doubled from late 2023, driven by longer shipping distances, higher fuel consumption and rising insurance premiums.

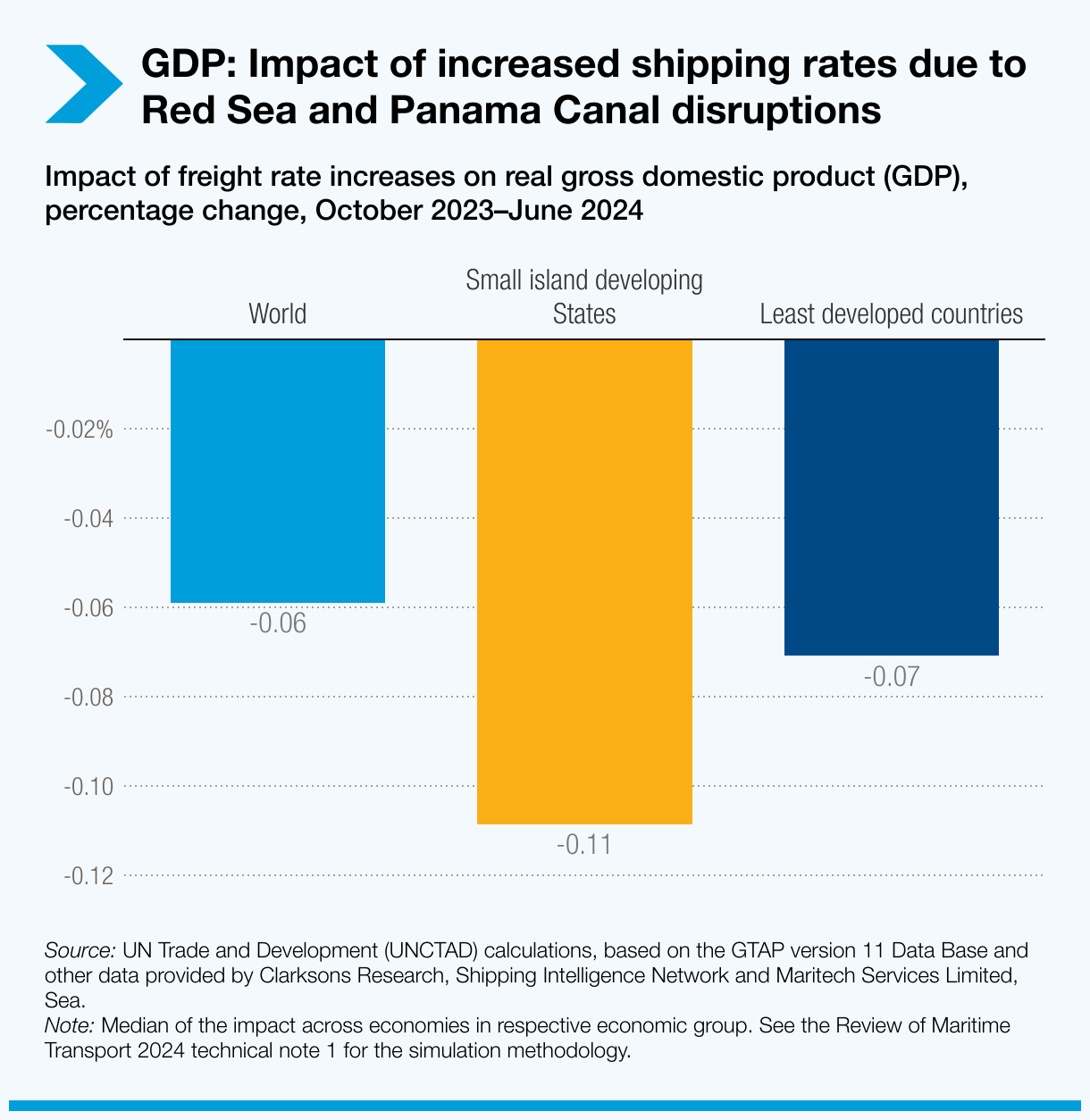

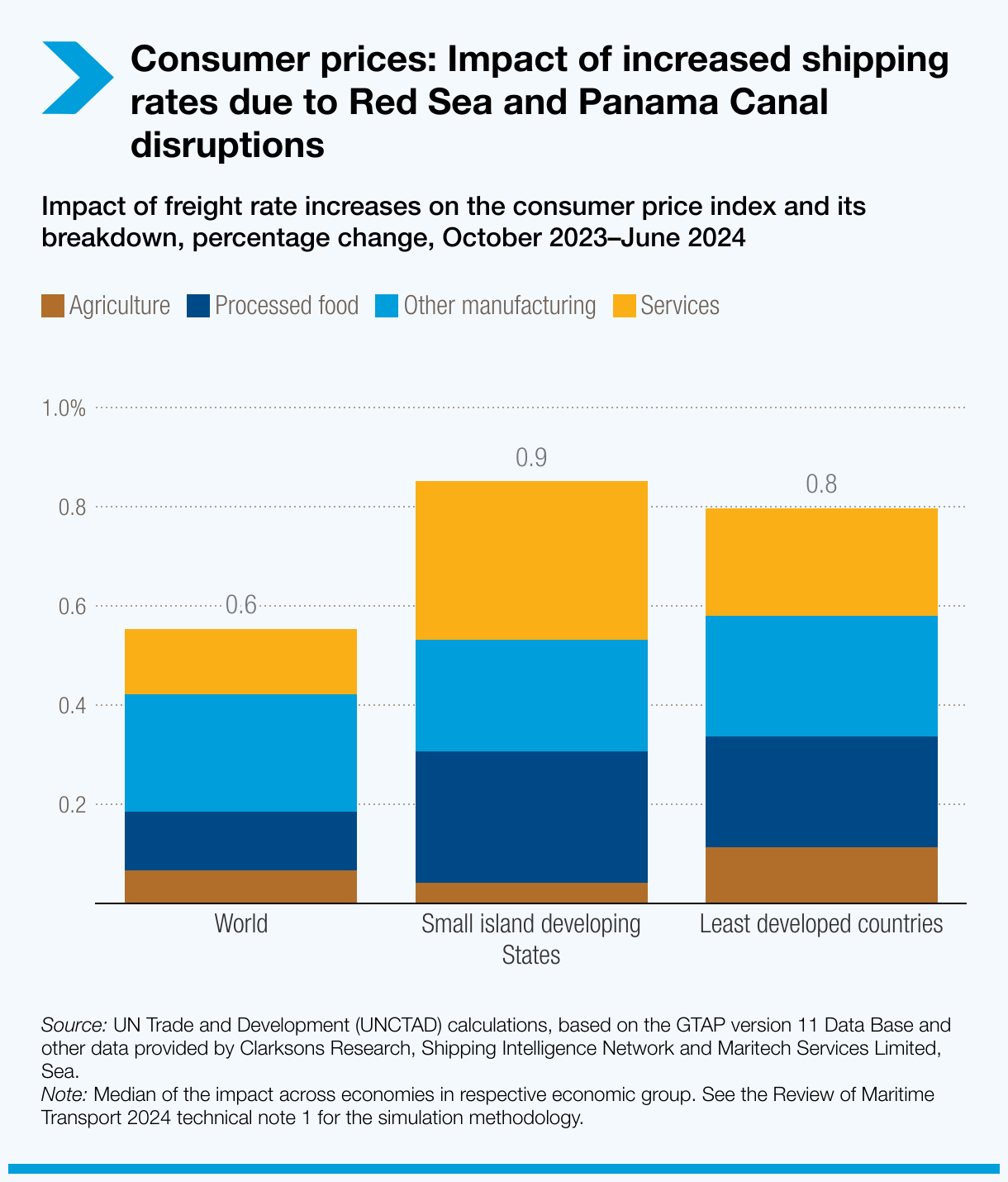

This surge in freight rates, if sustained, will push global consumer prices up, with UN Trade and Development projecting a 0.6% increase by 2025 due to higher shipping costs.

The impact is especially severe for vulnerable economies reliant on maritime transport, as rising costs erode trade competitiveness, threaten economic stability and drive inflation.

For example, small island developing States could see consumer prices rise by 0.9% by 2025, with processed food costs increasing by 1.3%, putting food security at risk.

Beyond the primary trans-Pacific and Europe-bound routes, spot freight rates also surged. From January to July 2024, the average rate on the SCFI Shanghai–South America route more than doubled to $9,026 per TEU, the highest level since September 2022.

During the same period, the SCFI Shanghai–South Africa route saw its average rate almost triple to $5,426 per TEU (the highest since July 2022), while the SCFI Shanghai–West Africa average rate jumped 137% to $5,563 per TEU (the highest since August 2022).

UN Trade and Development calls for

-

1Enhancing monitoring to better understand global freight markets.

-

2Implementing targeted policy measures to protect vulnerable economies from the inflationary impact of rising freight rates.

-

3Boosting global cooperation to streamline supply chains and reduce cost surges.

-

4Strengthening regional cooperation to reduce dependence on long-distance routes and enhance trade within developing regions.

Decarbonizing shipping demands

faster renewal of the world’s aging fleet

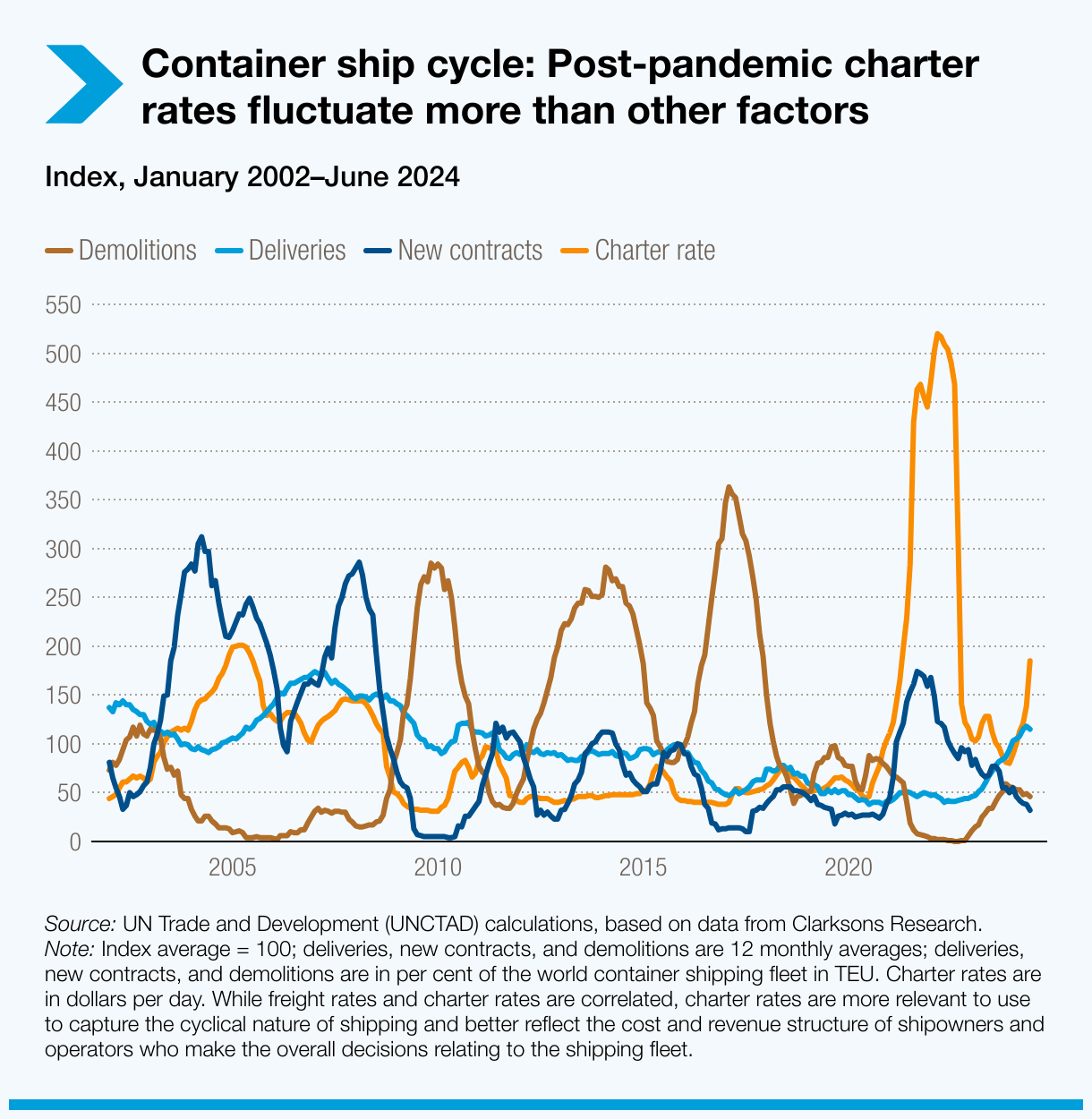

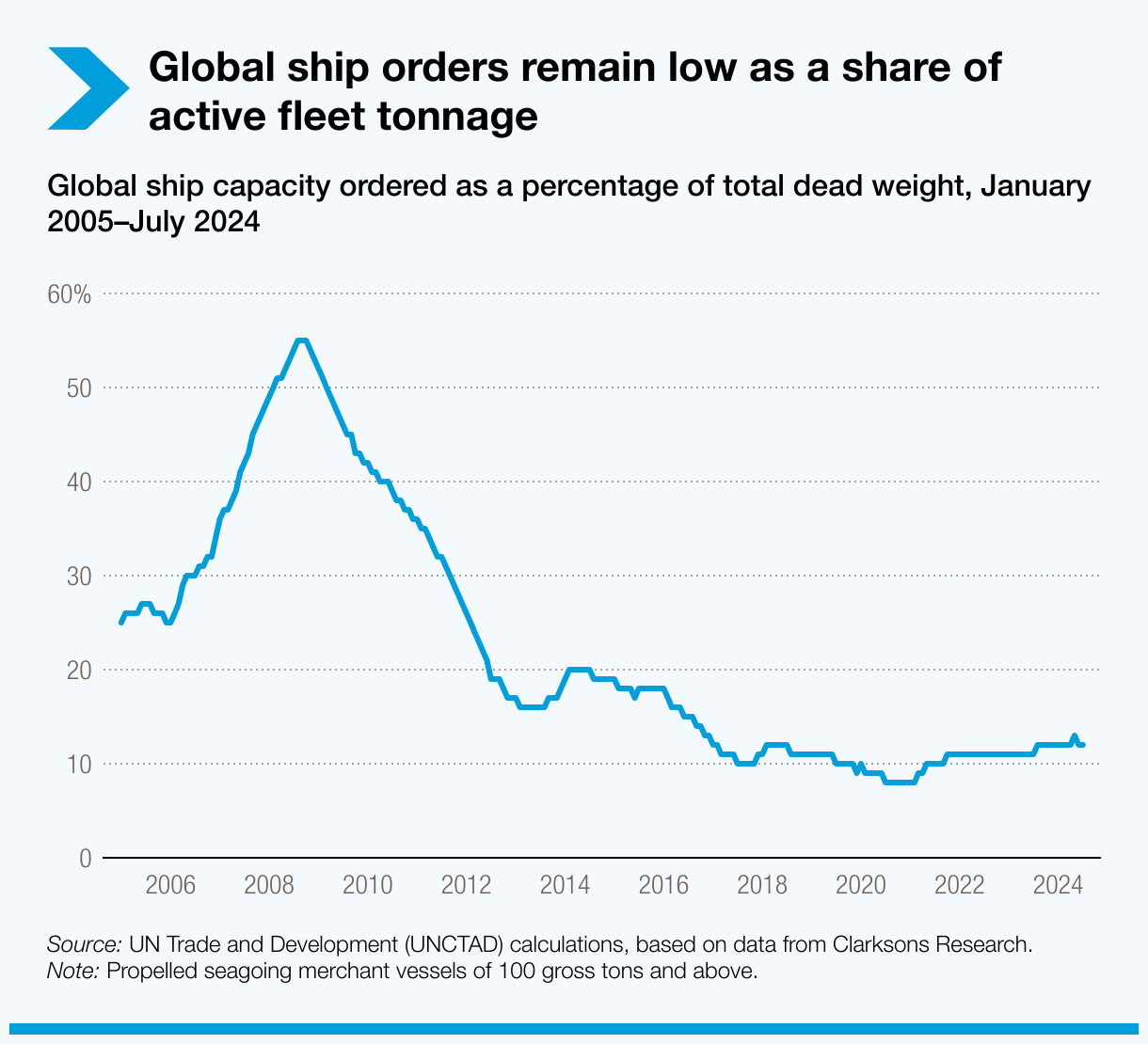

Shipping accounts for 3% of global greenhouse gas emissions. Despite growing pressure, the aging global fleet is renewing slowly due to high costs, uncertainty over future fuels and low ship scrapping rates.

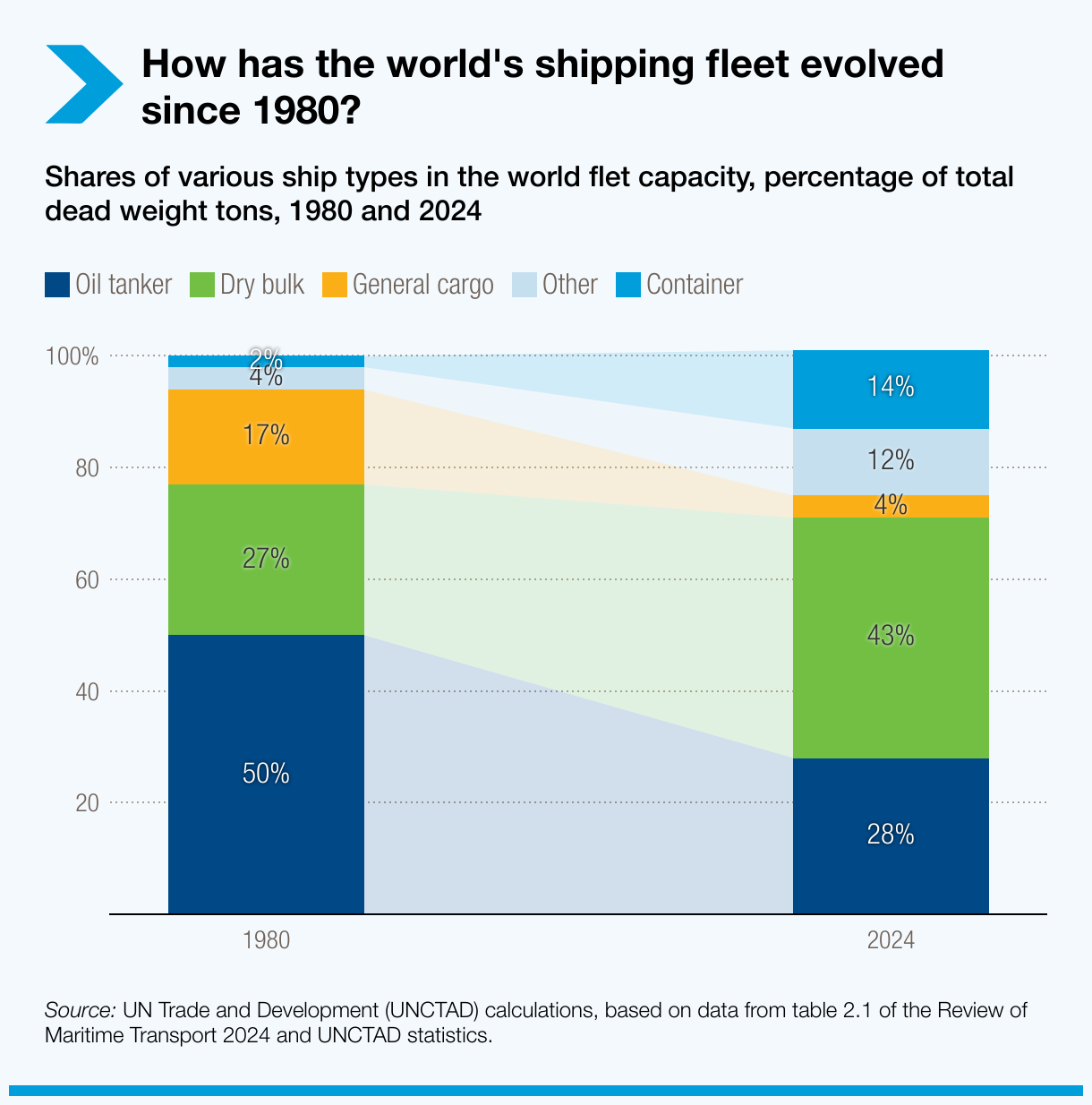

In 2023, the global fleet grew by 3.4%, surpassing trade growth but still below historical averages. Total cargo capacity reached 2.4 billion tons. Growth was driven primarily by container ships and liquefied natural gas (LNG) carriers, though bulk carriers and oil tankers continue to hold the largest share.

By early 2024, only 14% of new tonnage was alternative fuel-ready, with 50% fuel-capable. Failure to accelerate decarbonization could lead to higher costs, regulatory penalties and a loss of competitiveness as markets increasingly prioritize sustainability.

Global shipbuilding trends also influence fleet renewal. In 2023, China, Japan and the Republic of Korea dominated the market. They produced 95% of the global output, with China delivering over half of the world’s capacity for the first time.

UN Trade and Development calls for

-

1Increased investments in alternative fuel technologies and low-carbon shipping solutions.

-

2Stronger regulatory frameworks to incentivize fleet renewal and adoption of greener technologies.

-

3Economic measures and financial incentives and support for retrofitting older vessels and investing in energy-efficient ships.

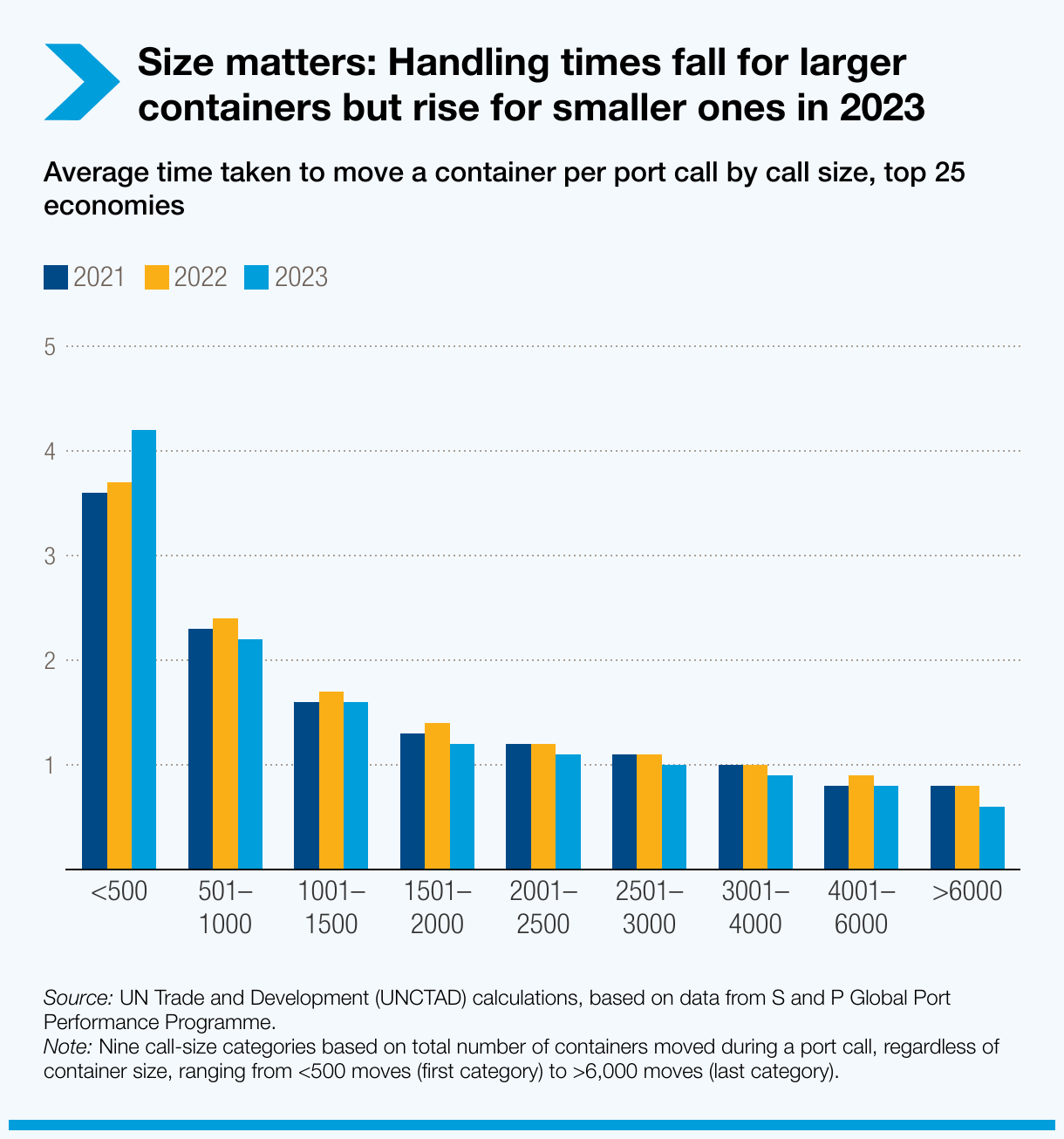

Enhancing trade facilitation, port performance

and mitigating climate risks to the maritime industry

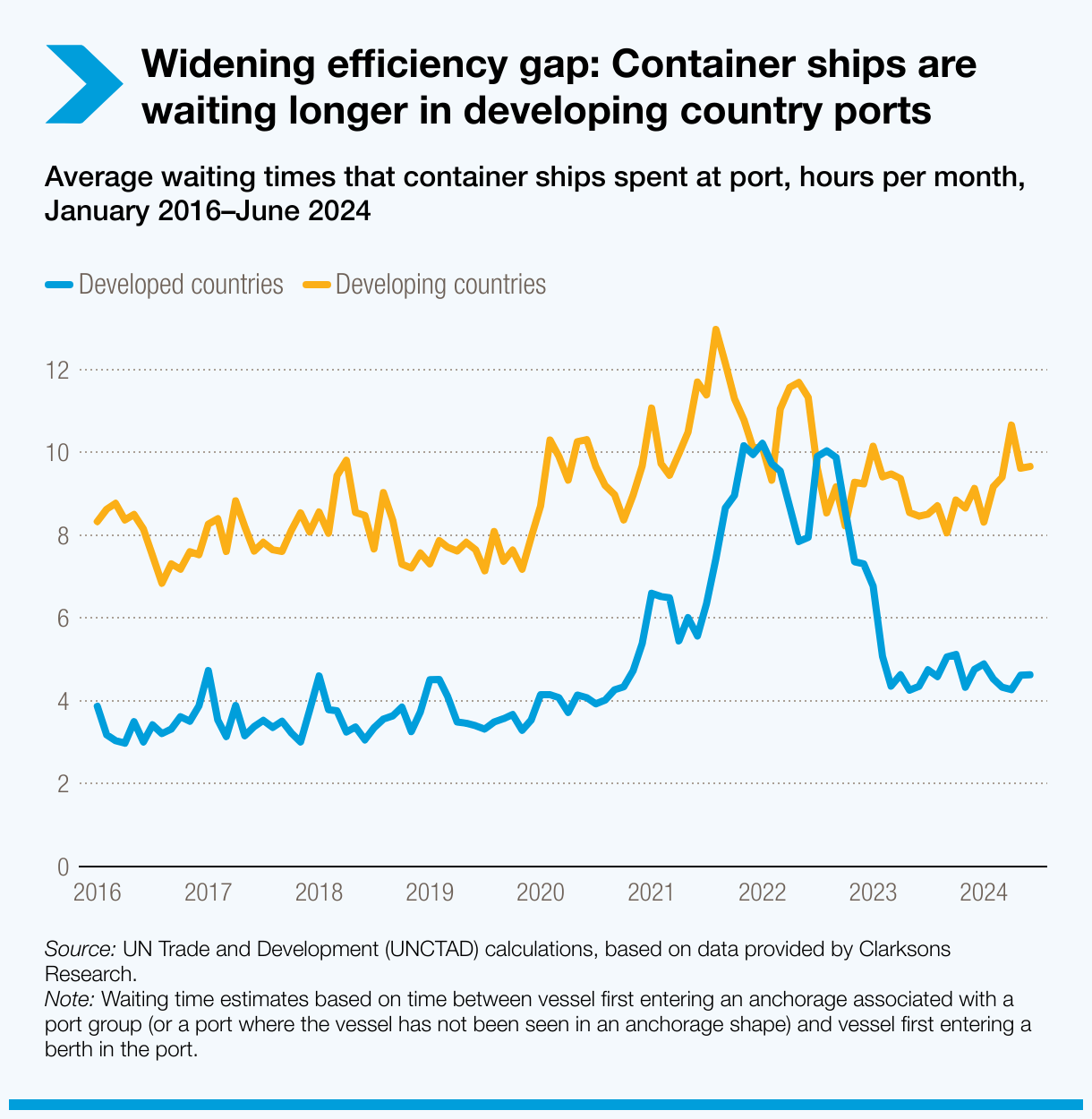

In 2023, container ship port calls hit record levels, with major ports like Singapore experiencing nearly double the waiting times due to rerouted vessels and rising shipping volumes.

Digitalization – through blockchain, artificial intelligence (AI) and automation – is key to improving port operations. Ports that have adopted these technologies report reduced waiting times, better cargo tracking and more efficient transshipment.

Asia is leading the way, with the region’s ports making significant strides in digital port management. Handling over 63% of global container port calls, they have maintained efficiency thanks to technological advancements.

Africa is pursuing important port and trade facilitation reforms. East African initiatives, like investments in dry ports in Ethiopia and Kenya, are reducing congestion and improving trade flows.

Caribbean ports face high operational costs and outdated infrastructure, which drive up expenses, reduce their competitiveness in global trade and leave them even more vulnerable to climate risks.

As climate change intensifies, the growing risks of damage, disruption and delay to port and shipping infrastructure and operations – along with implications for safety and contractual rights and obligations – need to be assessed and addressed before such risks and losses materialize. Doing so is important to minimize losses and legal disputes and keep trade flowing and insurance affordable.

UN Trade and Development calls for

-

1Accelerated investments in digital technologies like AI and blockchain to streamline port operations, reduce congestion and improve supply chain efficiency.

-

2Expanded inland terminals to decentralize port operations and boost regional trade flows.

-

3Public-private partnerships to enhance port infrastructure and ensure resilience to climate risks.

-

4The development of climate-proofed infrastructure to safeguard ports from extreme weather and future disruptions.

-

5Increased attention to the commercial law implications of weather and climate-related risks to ports and shipping, and the development of appropriate and balanced contractual approaches to risk allocation.