Global economic fracturing and shifting investment patterns

A diagnostic of 10 FDI trends and their development implications

The report spotlights 10 major shifts in global foreign direct investment (FDI).

It reveals how the combination of structural transformations in global value chains (GVCs), external shocks like the COVID-19 pandemic and rising geopolitical tensions are increasingly influencing investment decisions and hindering development.

Here are some key findings.

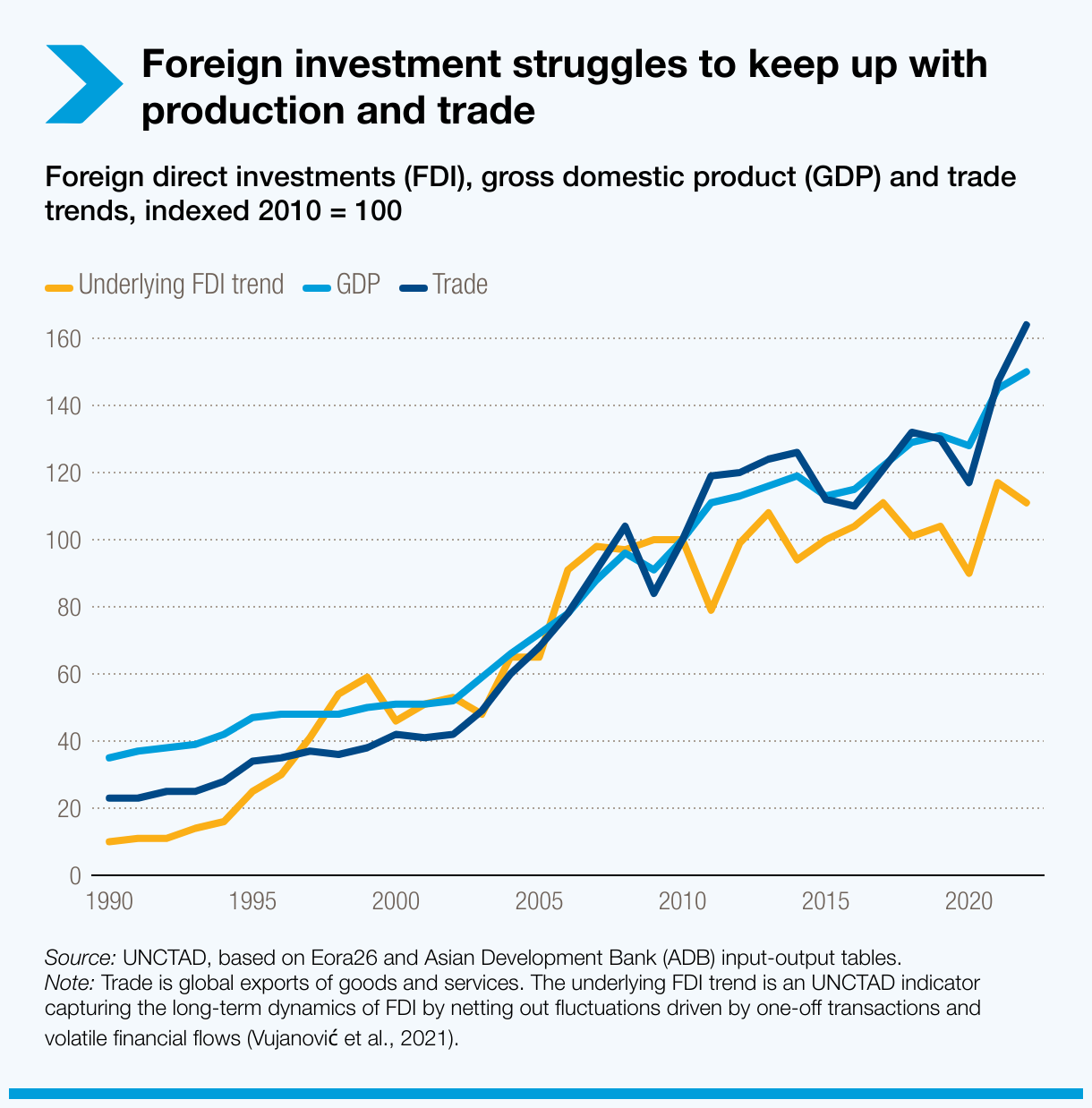

FDI struggles to keep pace with trade and GDP

- Since 2010, global GDP and trade have grown annually by an average of 4% and 4.2%, respectively, even amidst rising trade tensions. By contrast, FDI growth has stagnated near zero.

- This lag reflects increased investor caution as a result of shifts in international production and GVCs, rising protectionism and growing geopolitical tensions. It highlights the vulnerability of developing economies that are dependent on FDI.

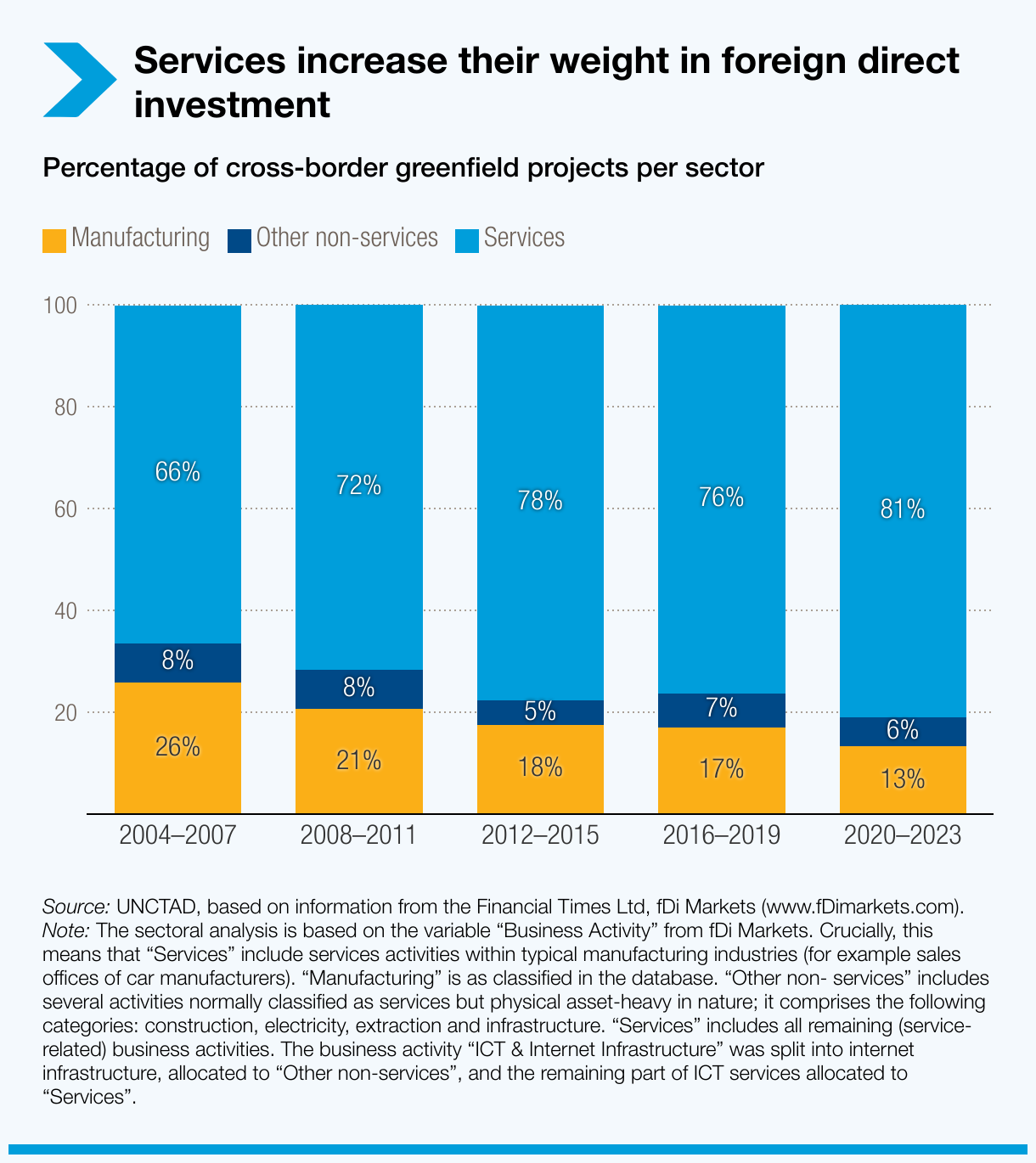

Shift from manufacturing to services

- The share of cross-border greenfield projects in the services sector rose from about 65% two decades ago to over 80%. And services-related investment within manufacturing industries nearly doubled to about 70%, driven by technological advances.

- Meanwhile, FDI in manufacturing has seen a significant downturn, with a compound annual growth rate of -12% in the three years following the outbreak of the pandemic. The decline severely hinders developing economies’ efforts to leverage participation in GVCs for economic development and industrial transformation.

Diminishing role of FDI in China

- The geography of global FDI has been significantly re-shaped by China’s reduced role as a recipient country over the past two decades, a process that accelerated after the outbreak of the COVID-19 pandemic.

- Over the past three years, the number of greenfield projects to China has hovered at a level around one third the same figure a decade ago.

- However, China continues to play a dominant role in global manufacturing and trade, suggesting that its “global factory” mode has not downsized but instead transitioned from globally integrated production networks to more domestically focused ones.

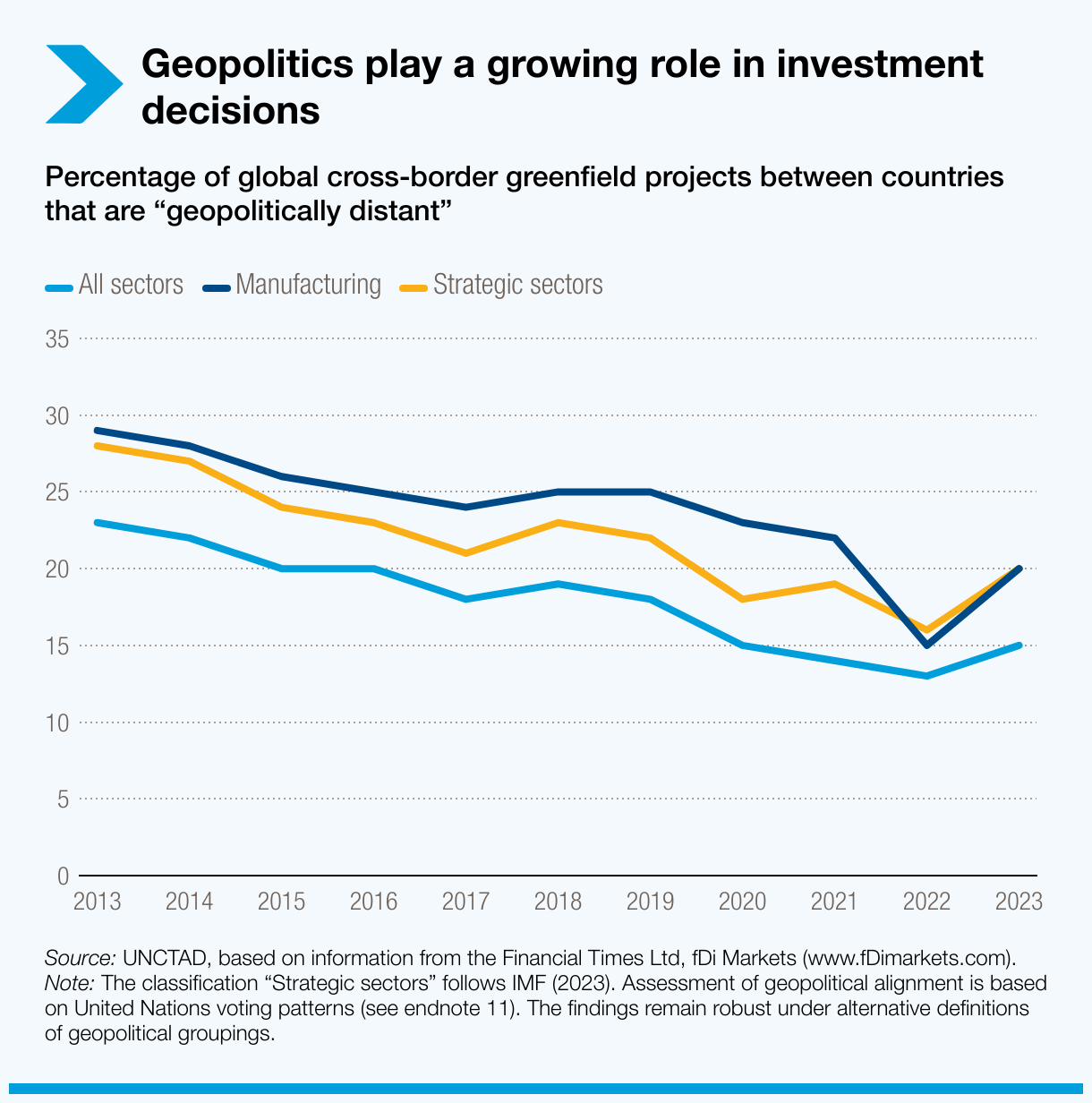

Geopolitical tensions increasingly affect FDI flows

- Investments between geopolitically distant countries – those with divergent political interests or foreign policies – decreased from 23% in 2013 to 13% in 2022.

- This trend particularly affected the manufacturing sector as trade tensions began to escalate in 2019.

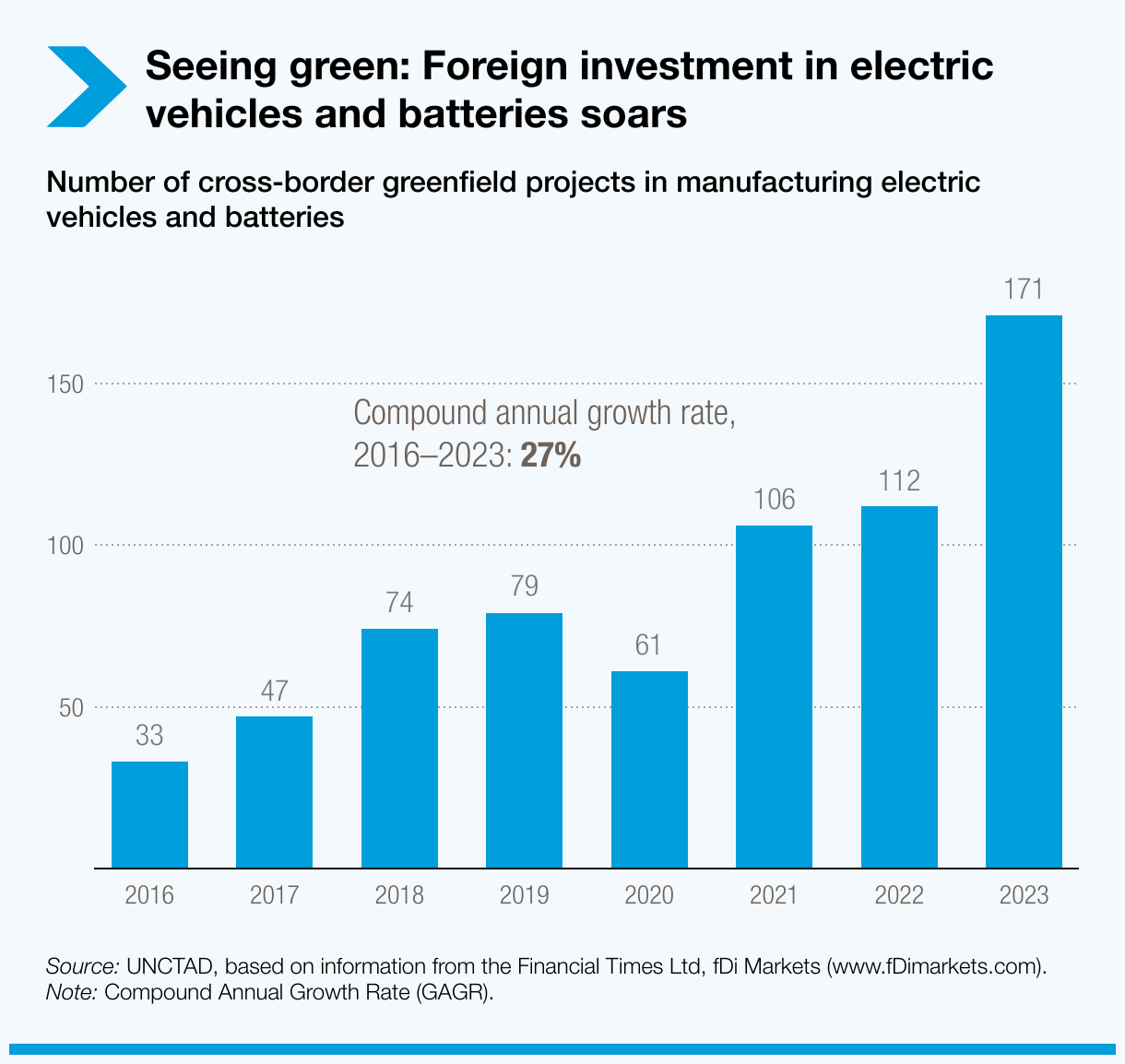

Rising investments in environmental technologies…

- Investments in environmental technologies like wind and solar energy have surged. Their share of total greenfield projects in non-services sectors jumped from 1% in the early 2000s to 20% by 2023. Likewise, FDI in the manufacturing of electric vehicles and batteries has seen 27% annual growth over the past decade.

- However, this growth only partially offsets the decline in other manufacturing sectors. It also primarily benefits developed countries, while least developed countries (LDCs) continue to struggle with reduced FDI in traditional sectors.

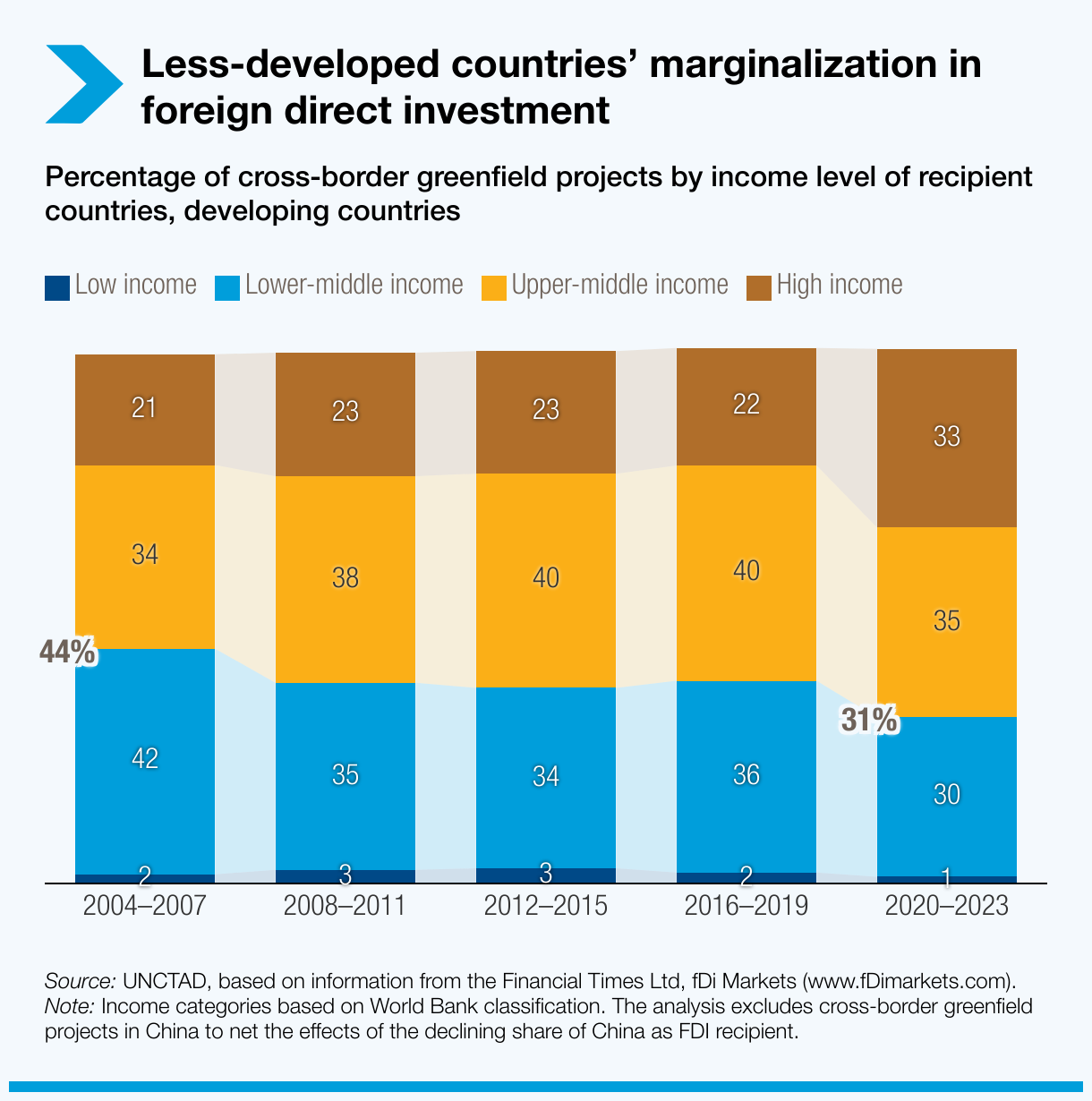

…But worsening marginalization of developing countries

- Global investment flows are increasingly concentrated in developed and major emerging markets, exacerbating economic vulnerabilities in smaller and less developed countries.

- The share of total greenfield FDI projects in LDCs has dwindled from 3% in the mid-2010s to just 1%. And the share of FDI in developing countries that goes to low-income and lower-middle-income economies has decreased by a third over the past decade.

Key recommendations

The report stresses the urgent need to align strategies with evolving investment trends to ensure that FDI benefits are distributed equitably and support broad developmental goals.

For global Institutions:

- Provide financial and strategic support to developing countries, particularly LDCs, to review their FDI and GVC-based development strategies and enhance their attractiveness to foreign investors.

- Strengthen international cooperation to manage geopolitical risks, ease tensions and ensure a stable and open investment climate.

For governments in developing countries:

- Revise their economic development strategies, as traditional reliance on manufacturing investments no longer guarantees sustained growth and economic development.

- Consolidate links with neighboring countries and cooperate at the regional level to strengthen regional value chains.

- Promote investments in sustainable and green technologies as well as in other sectors driven by the sustainability imperative and policy considerations.

Global economic fracturing and shifting investment patterns - A diagnostic of 10 FDI trends and their development implications (UNCTAD/DIAE/2024/1)

23 Apr 2024