The region cements its status as the largest recipient of global foreign investment, but trends vary across economies and sectors.

© Shutterstock/ Hien Phung Thu | A high-tech manufacturing facility in Ho Chi Minh City, Viet Nam. Despite global uncertainties, foreign investment in Southeast Asia remains resilient.

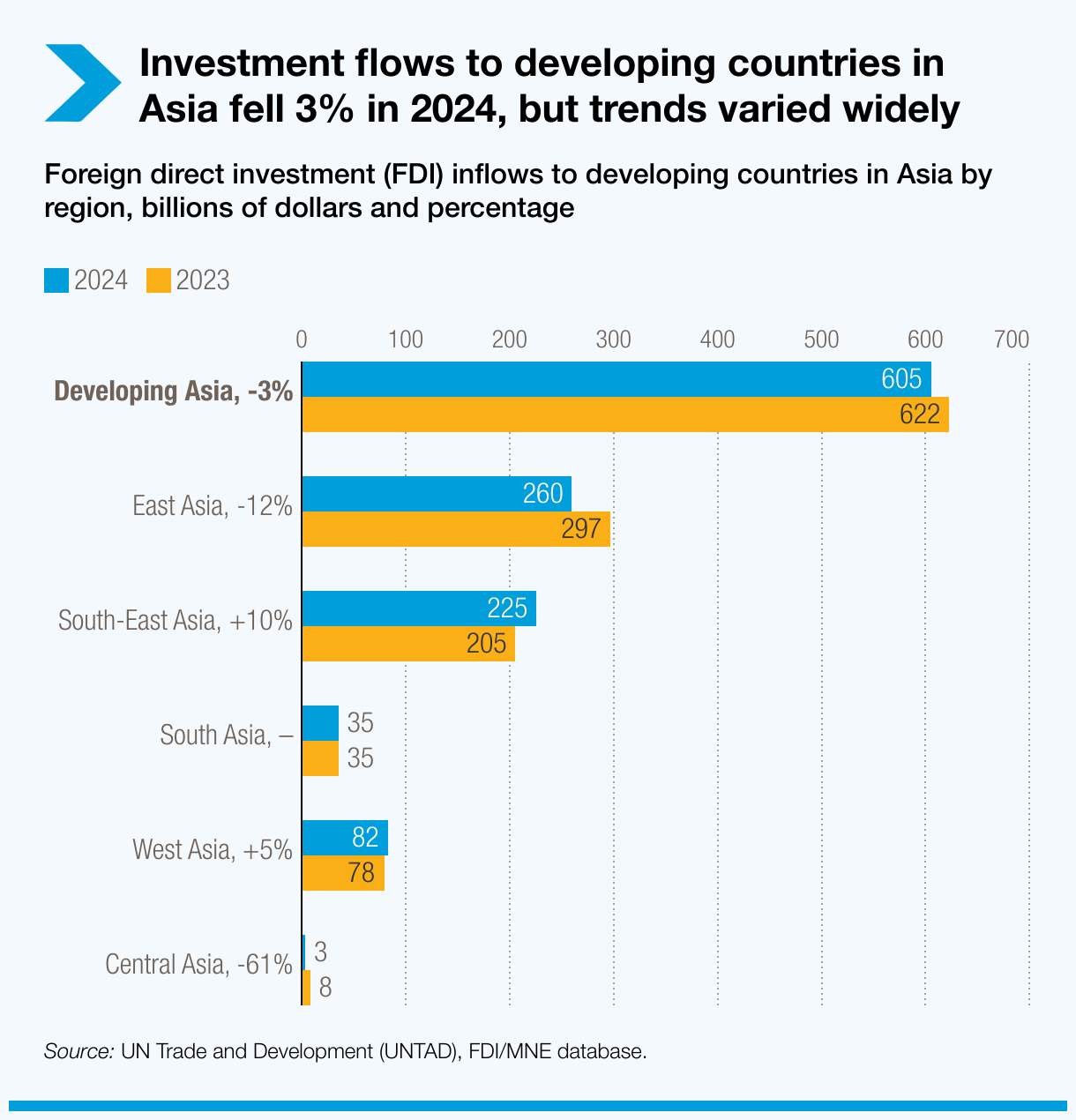

In 2024, developing economies of Asia attracted $605 billion in foreign direct investment (FDI), according to the latest World Investment Report released by UN Trade and Development (UNCTAD) on 19 June.

Despite a 3% dip in value from the year before, developing Asia remains the world’s leading destination for inward foreign investment.

In 2024, the region received 40% of the world’s total FDI and 70% of inflows to developing economies.

Regional trends mirror global investment challenges

The report shows that foreign investment remains volatile, fragmented and highly concentrated, with many countries – especially in the Global South – at risk of being left behind.

While developing Asia continues to attract a large share of global FDI, the region’s mixed performance reflects broader global patterns: Declining infrastructure investment, growing digital flows and rising policy uncertainty.

Trends differ across economies

Looking at East Asia, foreign investment flows to China – the largest FDI recipient among developing economies – were down 29% in 2024.

The Association of Southeast Asian Nations, also known as ASEAN, remained a hot spot for foreign capital. In 2024, FDI to the bloc was up 10% at $225 billion, powered by growth across Indonesia, Malaysia, Singapore, Thailand and Vietnam.

FDI remained stable in South Asia, with increases in Pakistan and Sri Lanka. India, despite a slight fall, still receives the most foreign investment in this subregion.

Central Asia, in contrast, had a steep decline in FDI, mainly due to a sharp decrease in Kazakhstan.

Turning to members of the Gulf Cooperation Council, the United Arab Emirates stood out with a rebound in foreign investment, while declines were observed in other parts of the bloc – namely Bahrain, Kuwait, Oman, Qatar and Saudi Arabia.

How different forms of foreign investment performed

Developing Asia is home to nearly a third of global greenfield projects by number and over a quarter by value. This type of investment indicates a company is setting up new operations overseas.

In 2024, the number of greenfield projects rose 5% across the region, but total value fell by 23% to $363 billion.

Growth in sectors related to the digital economy and metal production was offset by declines in electricity, gas supply and petroleum processing, which dropped over $70 billion in combined value.

For country highlights, India led with a 28% increase in capital expenditures for announced projects reaching $110 billion. Azerbaijan, Bahrain, Qatar and Türkiye also showed strong growth.

International project finance (IPF) – crucial to funding infrastructure and public services – fell sharply across developing Asia.

The number of deals was down 27% in 2024 – broadly in line with the global average – but the total value dropped by a steeper 43% .

Such discrepancy suggests that the global downturn in IPF activities is affecting emerging markets more discretionally, due to elevated capital costs and higher risk perceptions linked to their macroeconomic, fiscal or political climate.

Meanwhile, cross-border mergers and acquisitions sales in developing Asia dropped 57% to $25 billion, driven largely by a 49% decline in China and divestments in India – from which Disney partially exited – and the United Arab Emirates.

Redirecting capital: Global recommendations

The UN Trade and Development report highlights that globally, redirecting capital to where it’s most needed will require:

- Reforms to global financial frameworks.

- Greater use of blended finance and regional digital infrastructure.

- Investment rules that help all economies benefit from the digital and clean transitions.