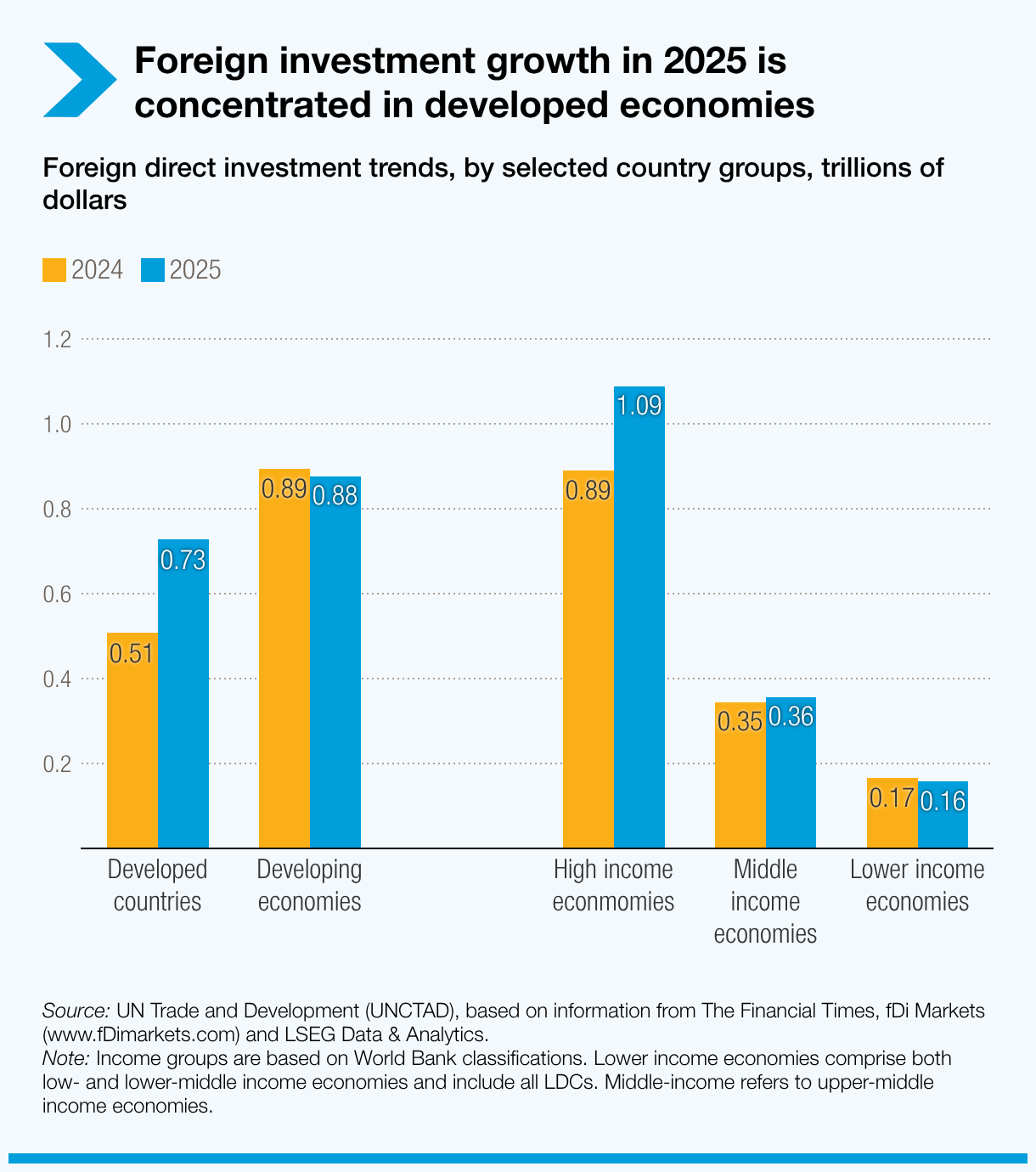

FDI surged in developed economies but declined in developing countries, becoming increasingly concentrated in capital-intensive sectors such as data centres.

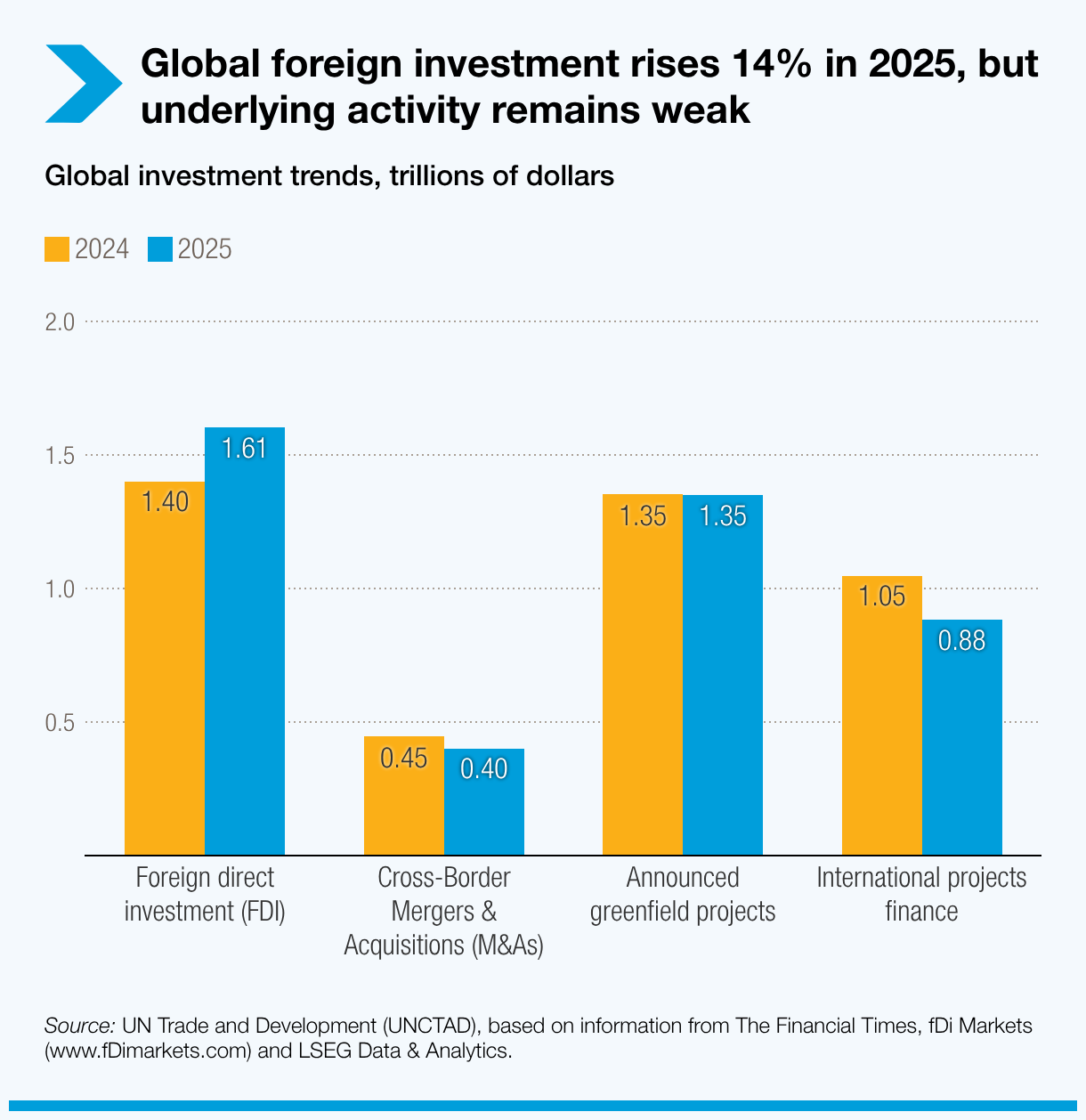

Global foreign direct investment (FDI) rose 14% in 2025 to $1.6 trillion, based on preliminary estimates published on 20 January in a report by UN Trade and Development. The increase marks a rebound after two years of decline.

But the report highlights that the headline growth overstates the recovery. A large share of the increase came from flows through global financial centres, while real investment activity remained fragile.

Investment patterns point to widening divides between developed and developing economies, growing concentration in a small number of strategic sectors, and persistent weakness in projects most critical for sustainable development.

Financial centres drive growth

More than $140 billion of the increase came from higher flows through global financial centres. Without these “conduit flows”, global FDI rose by only about 5%. This highlights the limited recovery in underlying investment activity.

Key indicators of investor sentiment remained weak.

- The value of international mergers and acquisitions fell by 10%.

- International project finance fell 16% in value and 12% in deal numbers, marking the fourth straight year of decline and reaching levels last seen in 2019.

- Announcements of greenfield projects dropped by 16% in number. These are new, from-scratch foreign investment projects. Total values were high but driven by a small number of mega-projects.

FDI flows jump 43% in developed economies

FDI flows to developed economies jumped 43% to $728 billion in 2025, driven by Europe and financial hubs. The European Union saw a 56% increase, supported by large cross-border acquisitions and a rebound in major economies including Germany, France and Italy.

By contrast, flows to developing economies declined by 2% to $877 billion. Lower-income countries were hit hardest, with three quarters of least developed countries seeing stagnant or declining flows.

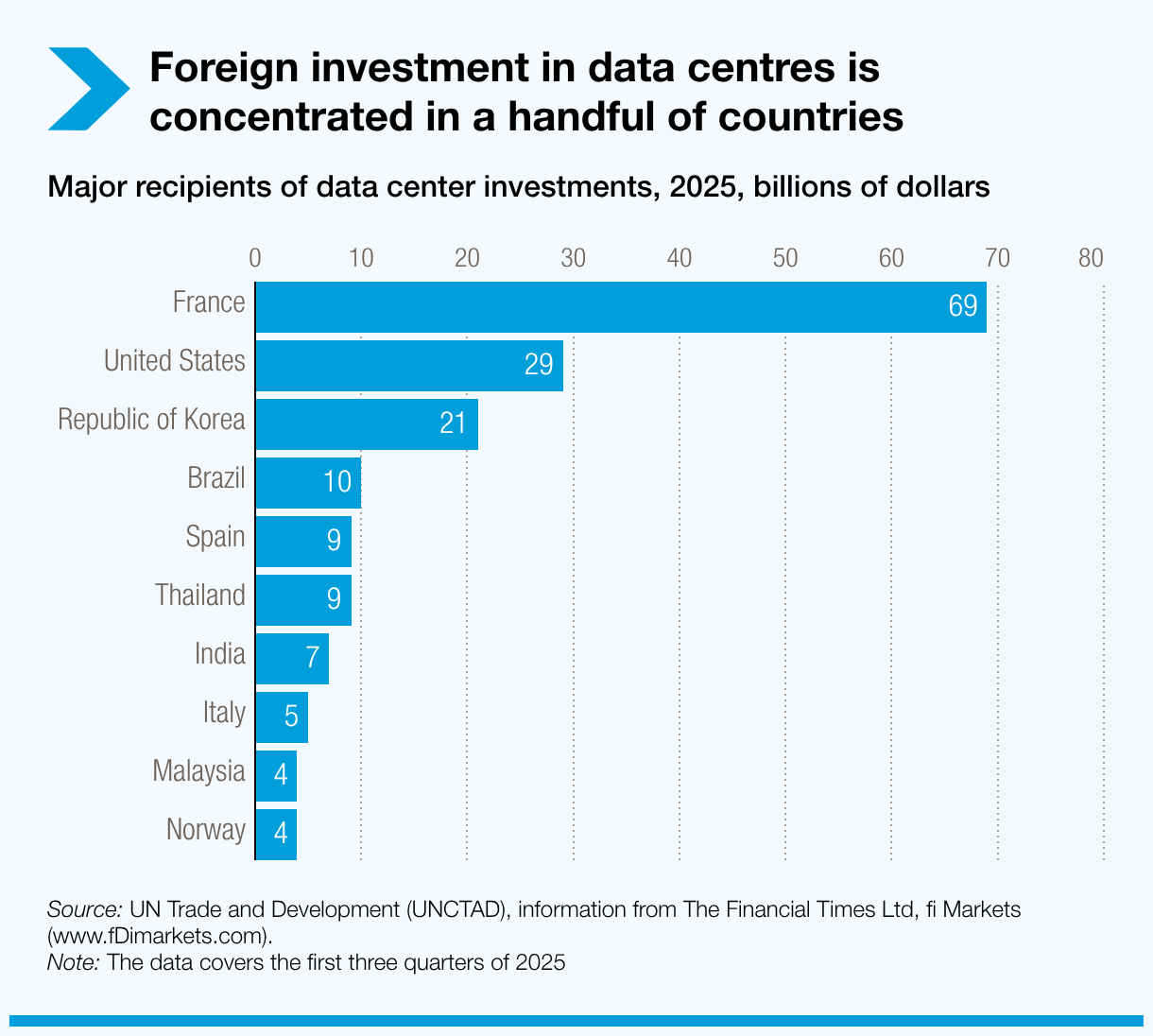

Investment surges in data centres and semiconductors

The report highlights a growing concentration of FDI in projects that are capital intensive and technology driven.

Data centres attracted more than one fifth of global greenfield project values in 2025, with announced investment exceeding $270 billion. Demand was driven by AI infrastructure and digital networks.

France, the United States and the Republic of Korea led as host countries, while emerging markets such as Brazil, India, Thailand and Malaysia also attracted major projects.

Similarly, the value of newly announced semiconductor projects rose by 35%.

By contrast, project numbers fell sharply by 25% in tariff-exposed, global value chain-intensive sectors. Textiles, electronics and machinery were particularly affected.

While investment in technology-driven, capital-intensive projects lifts overall FDI figures, flows remain highly concentrated and generate limited spillovers. Policies should aim to link digital infrastructure investment more closely to skills development, innovation systems and local value creation.

Infrastructure and renewable energy investment remain weak

International infrastructure projects fell by 10%, largely due to a sharp pullback in renewable energy as investors reassessed revenue risks and regulatory uncertainty.

Domestic investors increasingly filled the gap, with domestically led infrastructure projects rebounding strongly. But this shift risks widening investment gaps in countries that depend on international financing for large-scale infrastructure projects.

Outlook for 2026 remains uncertain and fragile

Looking ahead, downside risks are mounting. FDI flows could increase modestly in 2026 if financing conditions continue to ease and cross-border mergers and acquisitions pick up.

But real investment activity is likely to remain subdued, weighed down by geopolitical tensions, policy uncertainty and economic fragmentation. Without coordinated action, global investment risks becoming more concentrated in a few regions and sectors.