Factors beyond economic determinants are increasingly shaping investment decisions, sidelining smaller economies and hindering FDI-based development.

A new UN Trade and Development (UNCTAD) report sheds light on major shifts in global foreign direct investment (FDI) shaped by trends in global value chains, technological advancements, geopolitical dynamics and environmental concerns.

The report, entitled “Global economic fracturing and shifting investment patterns”, cautions that factors beyond economic determinants are increasingly shaping investment decisions, complicating standard approaches to investment promotion.

Five graphs illustrate the impact of these shifts on FDI-based development.

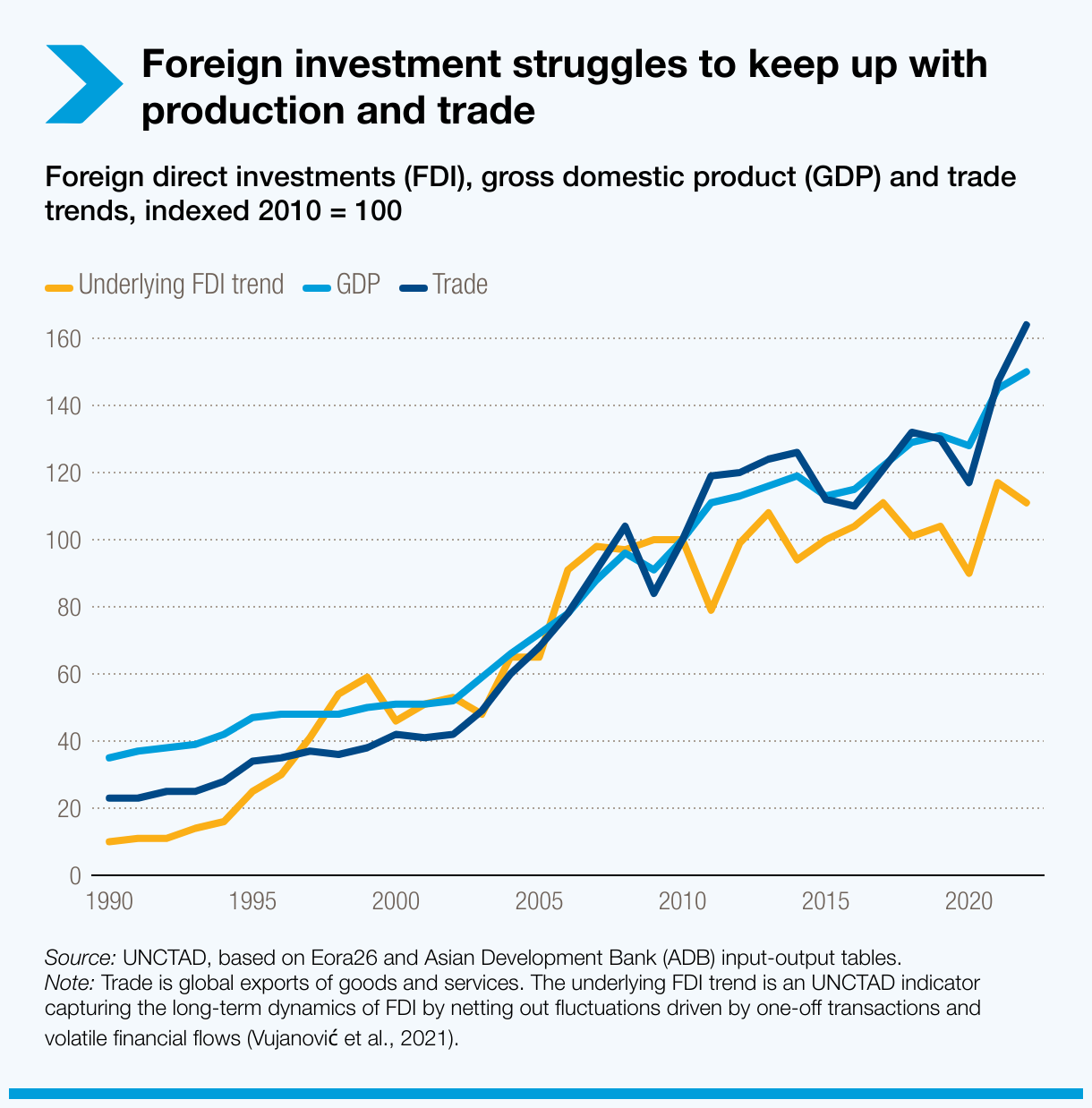

FDI struggles to keep pace with GDP and trade

The growth of FDI and global value chains (GVCs) is no longer aligned with GDP and trade growth, indicating a significant shift in the global economy.

Since 2010, global GDP and trade have grown annually by an average 3.4% and 4.2%, respectively, even amidst rising trade tensions. Meanwhile, FDI growth has stagnated near zero.

This lag reflects increased investor caution due to shifts in international production and GVCs, rising protectionism and growing geopolitical tensions.

It also highlights that developing countries that are dependent on FDI for economic development are particularly vulnerable to fluctuations in global investment flows.

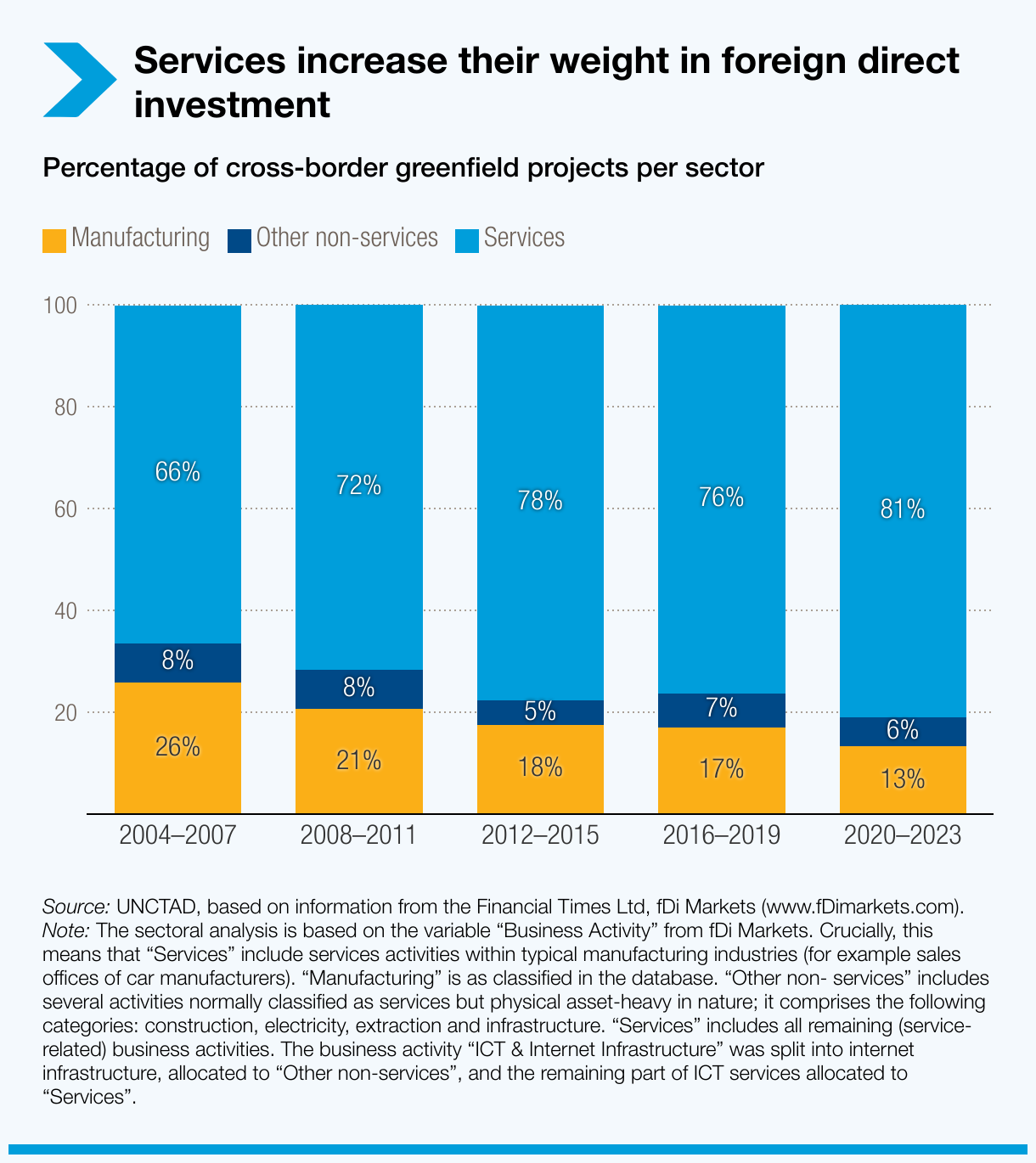

Shift from manufacturing to services

FDI is increasingly favouring services over manufacturing, widening the gap between the two sectors.

From 2004 to 2023, the share of cross-border greenfield projects in the services sector jumped from 66% to 81%. Simultaneously, investment in services within manufacturing industries nearly doubled to about 70%, propelled by rapid technological advances.

In contrast, FDI in manufacturing stagnated for two decades before experiencing a significant downturn, with a negative compound annual growth rate of -12% in the three years after the COVID-19 outbreak.

The expansion of the services sector mainly benefits larger developing economies that can effectively compete, creating an imbalance that leaves smaller ones at a disadvantage. Additionally, the decline in FDI flows to manufacturing severely hinders less-developed economies’ ability to upgrade production methods and adopt new technologies.

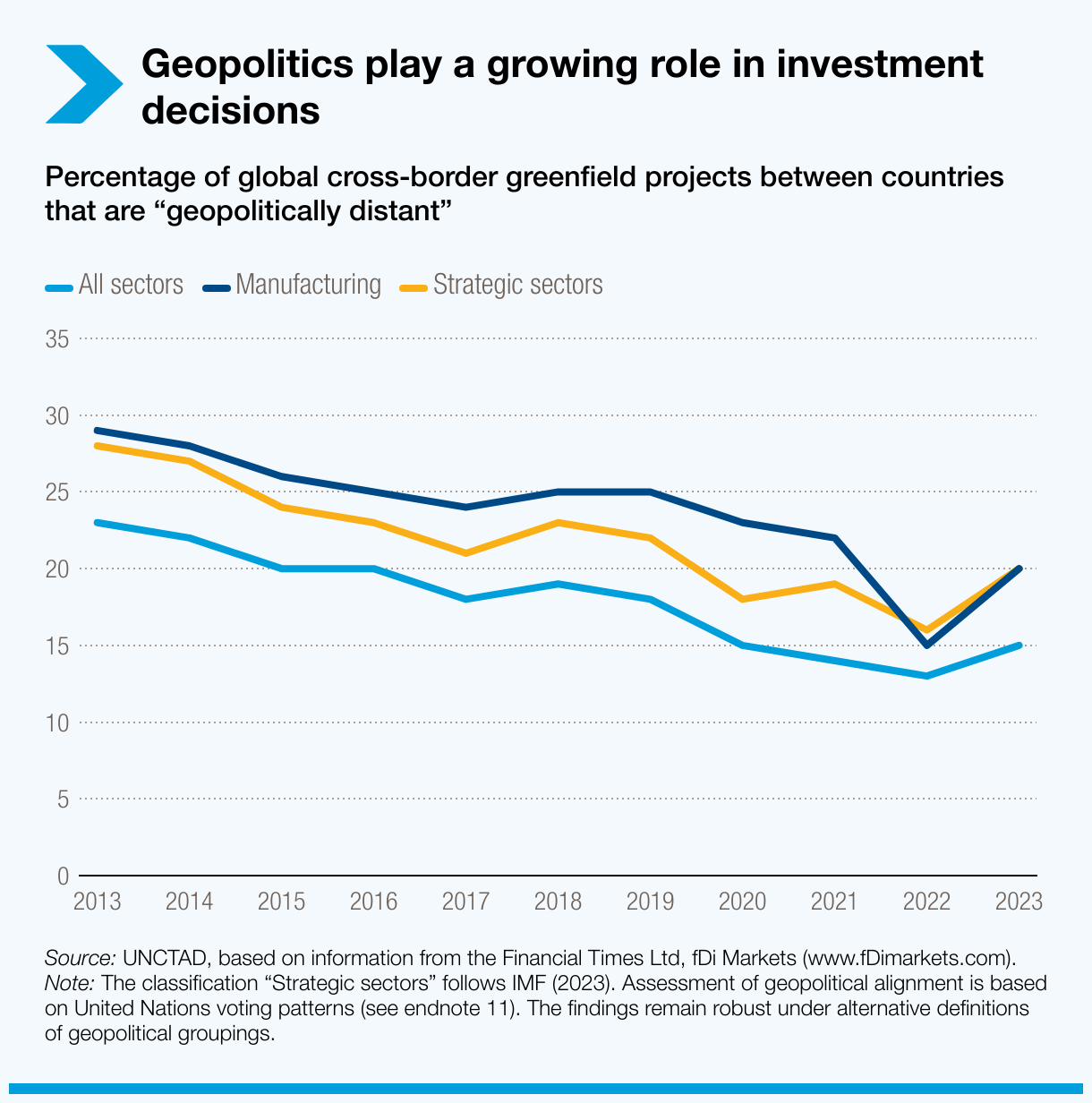

Geopolitical tensions increasingly affect FDI flows

Recent global conflicts and crises have disrupted usual investment patterns, leading to unstable investment relationships and limited chances to benefit from strategic diversification.

Investments between geopolitically distant countries – those with divergent political interests or foreign policies – decreased from 23% in 2013 to 13% in 2022.

This trend became particularly pronounced in manufacturing as trade tensions began to escalate in 2019.

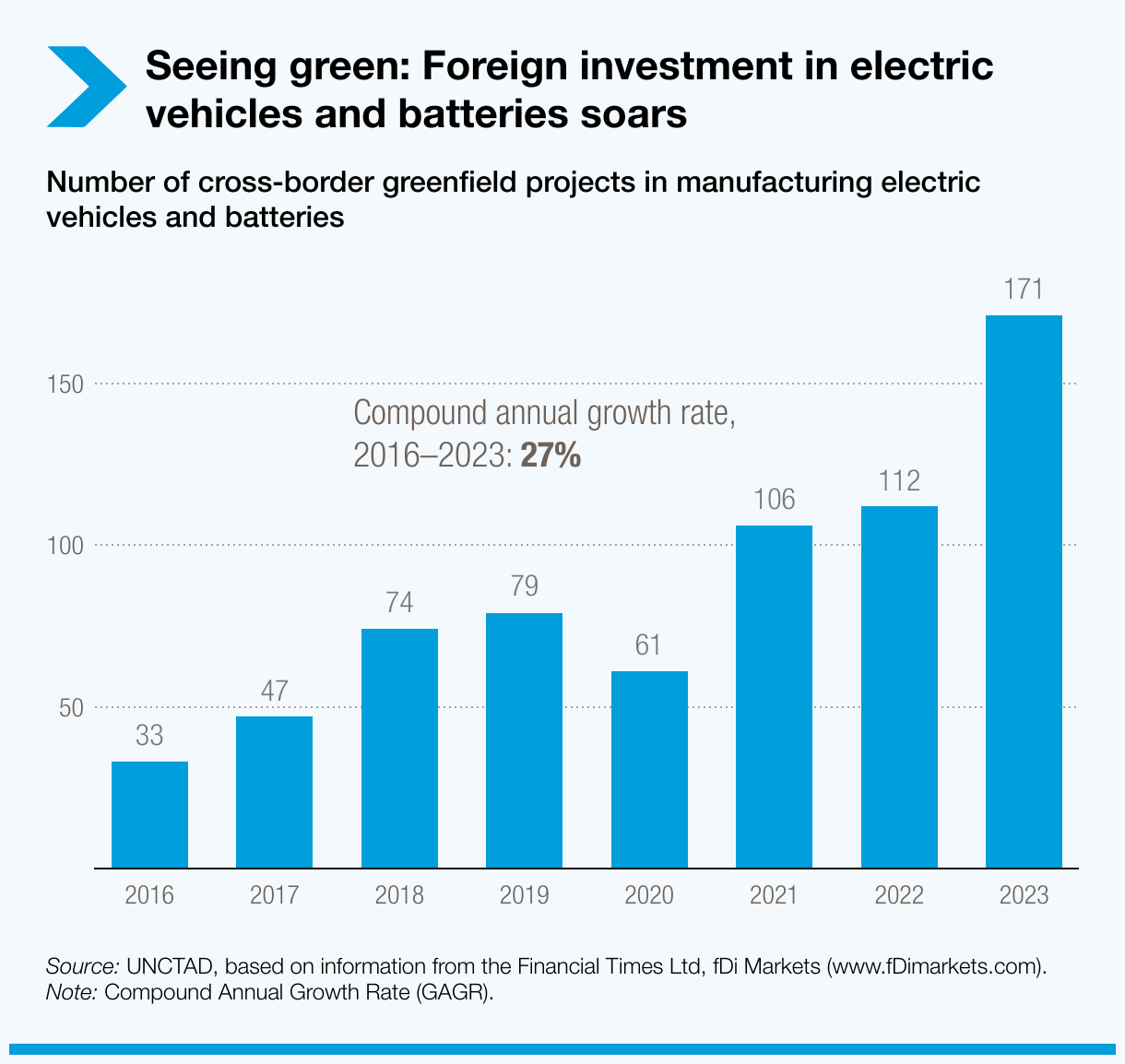

Investment in environmental technologies soars

As concerns over climate change intensify, FDI in environmental technologies like wind and solar energy has emerged as the fastest-growing sector outside of services.

Their share of total greenfield projects in non-services sectors has climbed from 1% to 20% over the past two decades. Similarly, FDI projects in the manufacturing of electric vehicles and batteries have grown 27% annually since 2016.

Beyond the green energy sector, other environmental technologies – from hydrogen production to sustainable aviation fuels and eco-friendly packaging – are expected to open new opportunities for countries to attract investment and develop new industries.

However, the surge in FDI for environmental technologies only partially offsets the decline in investment across other manufacturing sectors. Moreover, the focus on high-tech sectors mainly benefits developed economies, while smaller and less-developed economies continue to struggle with dwindling FDI in traditional sectors.

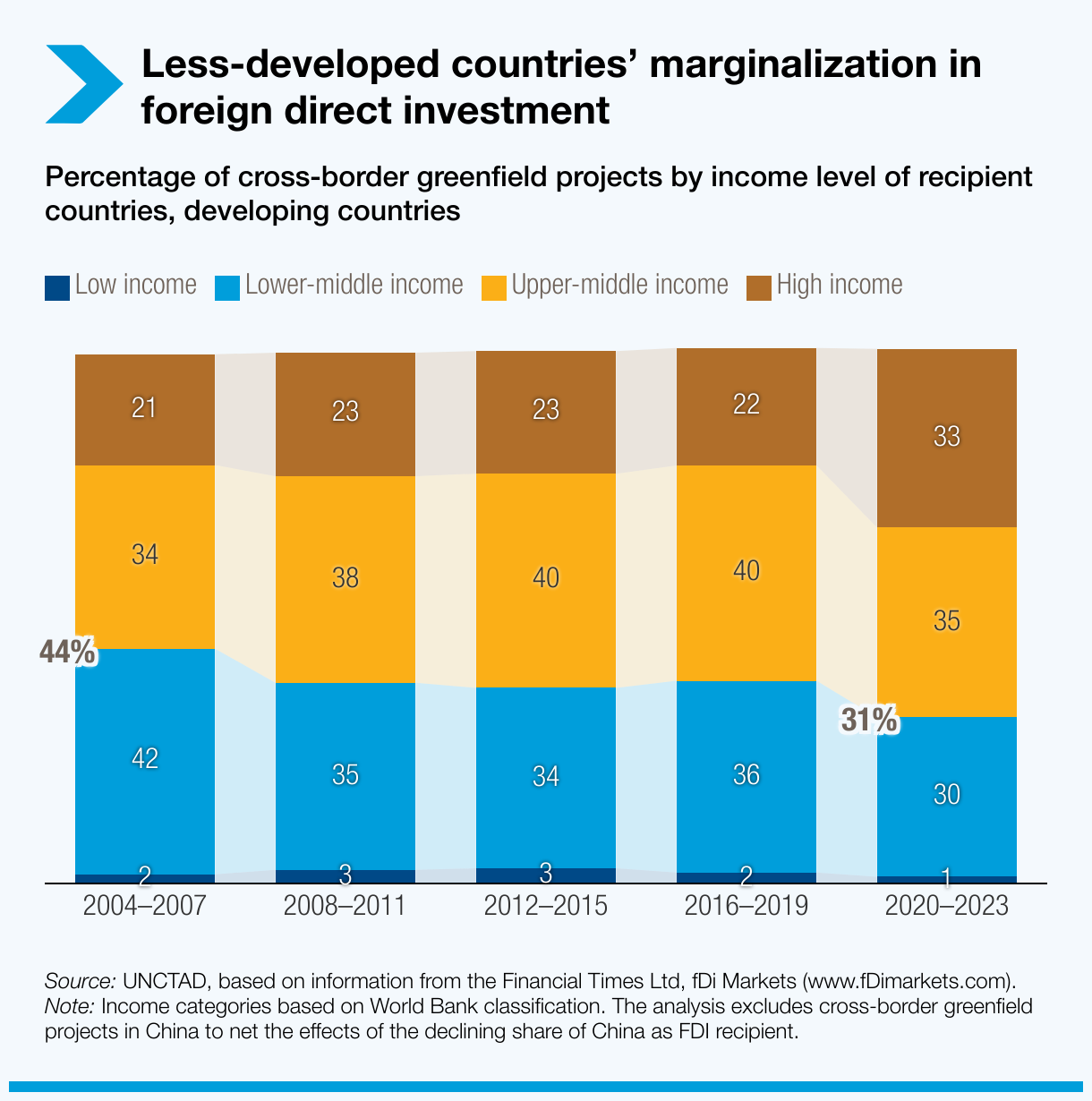

Less-developed countries’ marginalization worsens

Global investment flows increasingly favor sectors in developed and major emerging markets. This narrow focus tends to exclude smaller and less-developed countries, worsening their economic vulnerabilities.

The share of total greenfield FDI projects in least developed countries (LDCs) has dwindled from 3% in the mid-2010s to just 1%. Additionally, FDI in low-income and lower-middle-income countries has decreased by a third over the past two decades.

The narrowing focus of FDI, both geographically and sectorally, sidelines smaller and less-developed countries, heightening their economic fragility and undermining their aspirations for sustained growth and economic development.

Key recommendations

UN Trade and Development calls for immediate action to ensure that the benefits of investment are distributed more equitably and aligned with overarching developmental objectives.

For global institutions

- Provide financial and strategic support to developing countries, particularly LDCs, to review their FDI and GVC-based development strategies and enhance their attractiveness to foreign investors.

- Strengthen international cooperation to manage geopolitical risks, ease tensions and ensure a stable and open investment climate.

For governments in developing countries

- Revise their economic development strategies, as traditional reliance on manufacturing investments no longer guarantees sustained growth and economic development.

- Consolidate links with neighboring countries and cooperate at the regional level to strengthen regional value chains.

- Promote investments in sustainable and green technologies as well as in other sectors driven by sustainability objectives and policy considerations.