Developing countries entered 2025 facing a convergence of economic challenges. Major international policy shifts, escalating geopolitical tensions, tighter financial conditions and declining official development assistance (ODA) have weakened export performance, dampened growth prospects and constrained government revenues.

Although external debt growth moderated in 2024, fiscal and external buffers continued to erode across many developing countries – threatening debt sustainability and undermining investment for sustainable development.

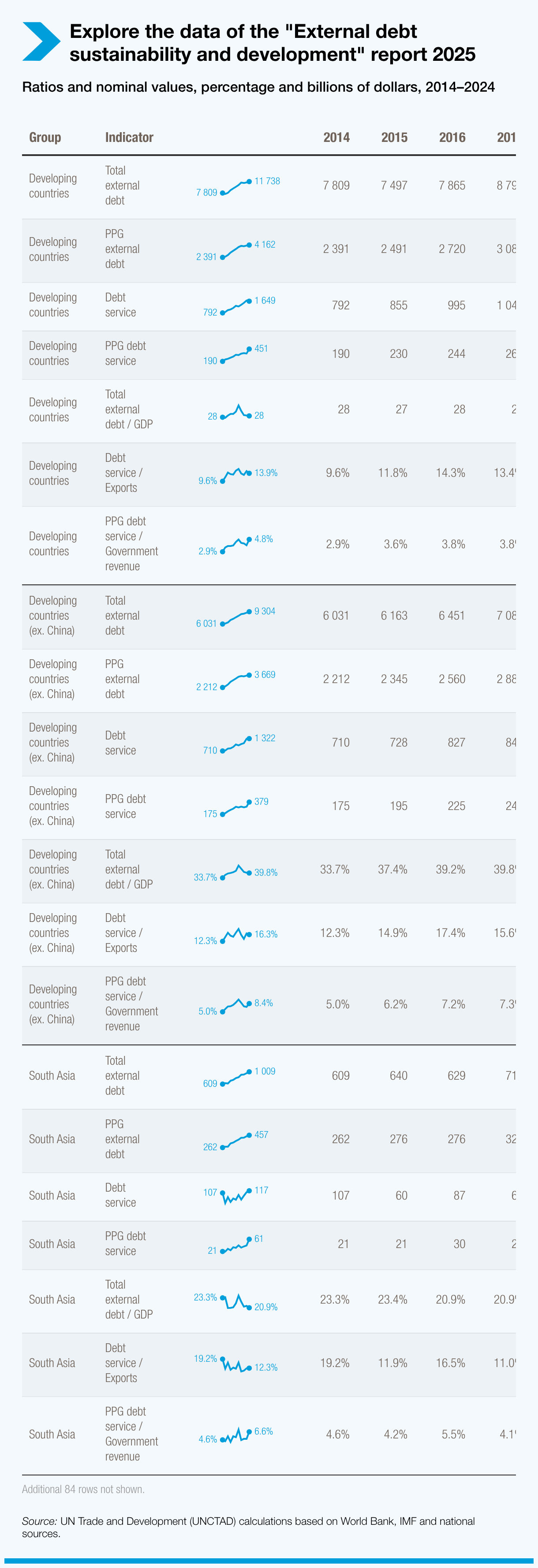

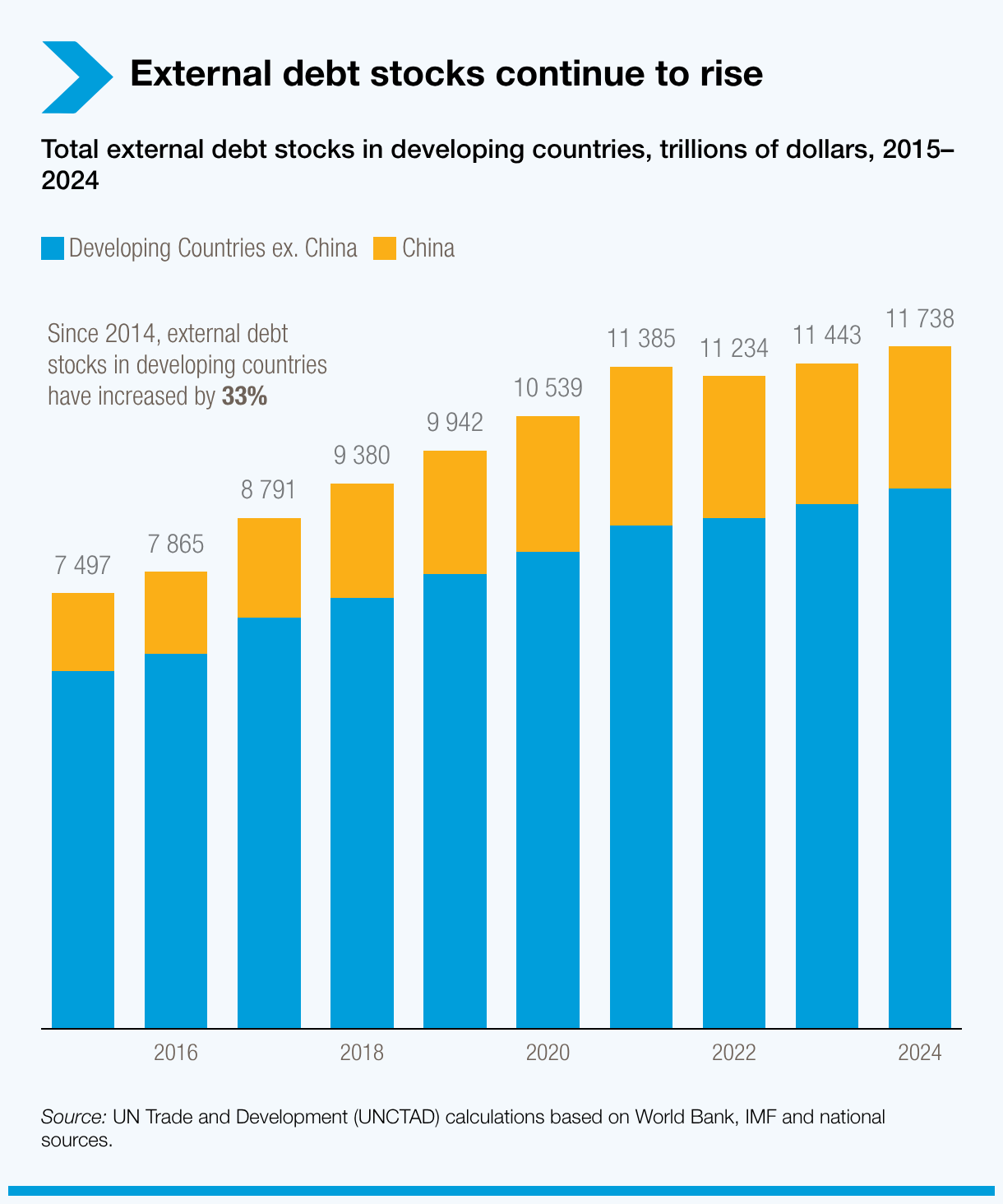

Total external debt in developing countries rose 2.6% to $11.7 trillion in 2024. Although their debt accumulation has slowed, servicing costs remained high, with an estimated $1.6 trillion due in 2024 – diverting critical resources from education, health, infrastructure and other development priorities.

Debt sustainability under threat across developing countries

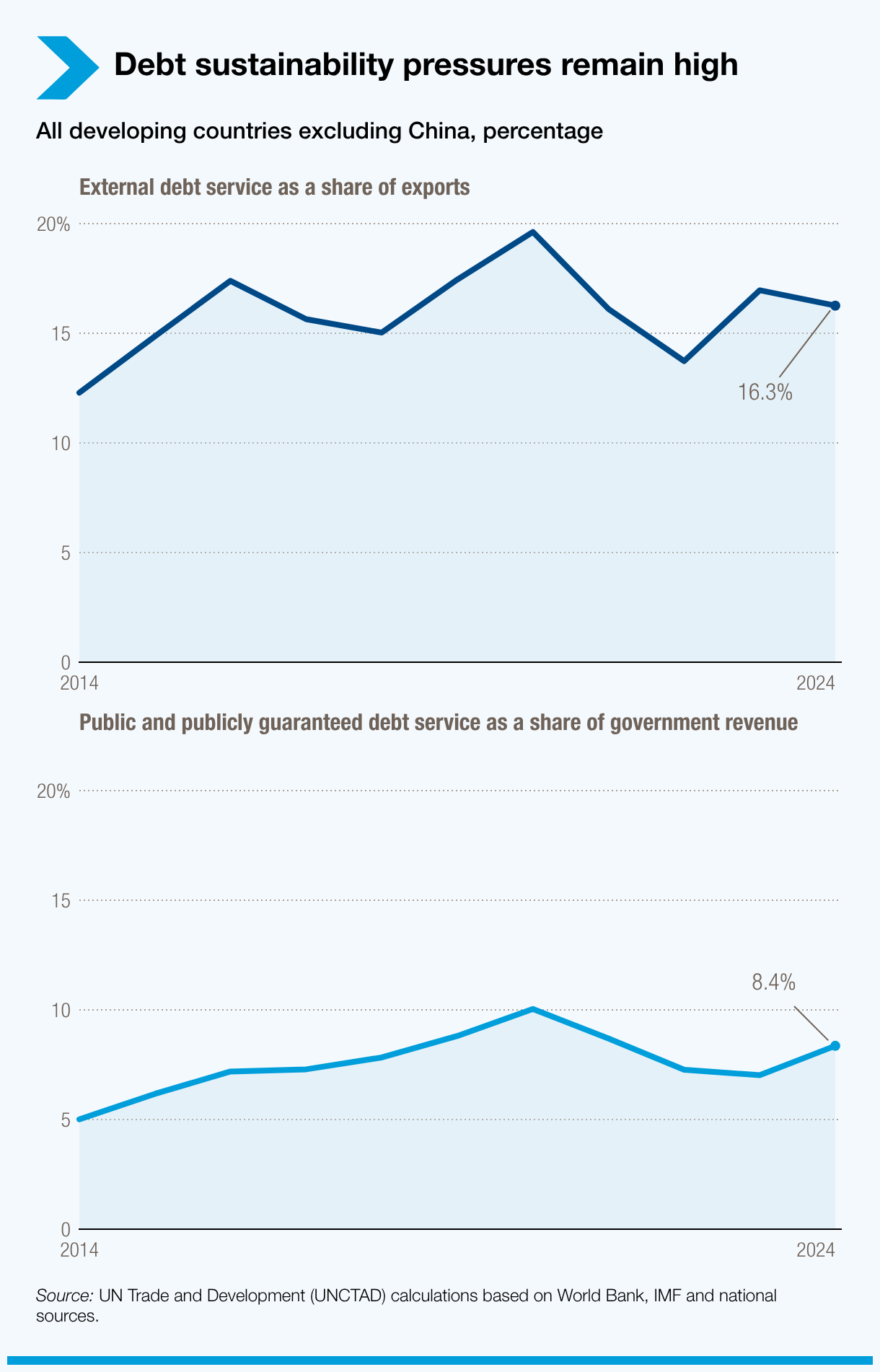

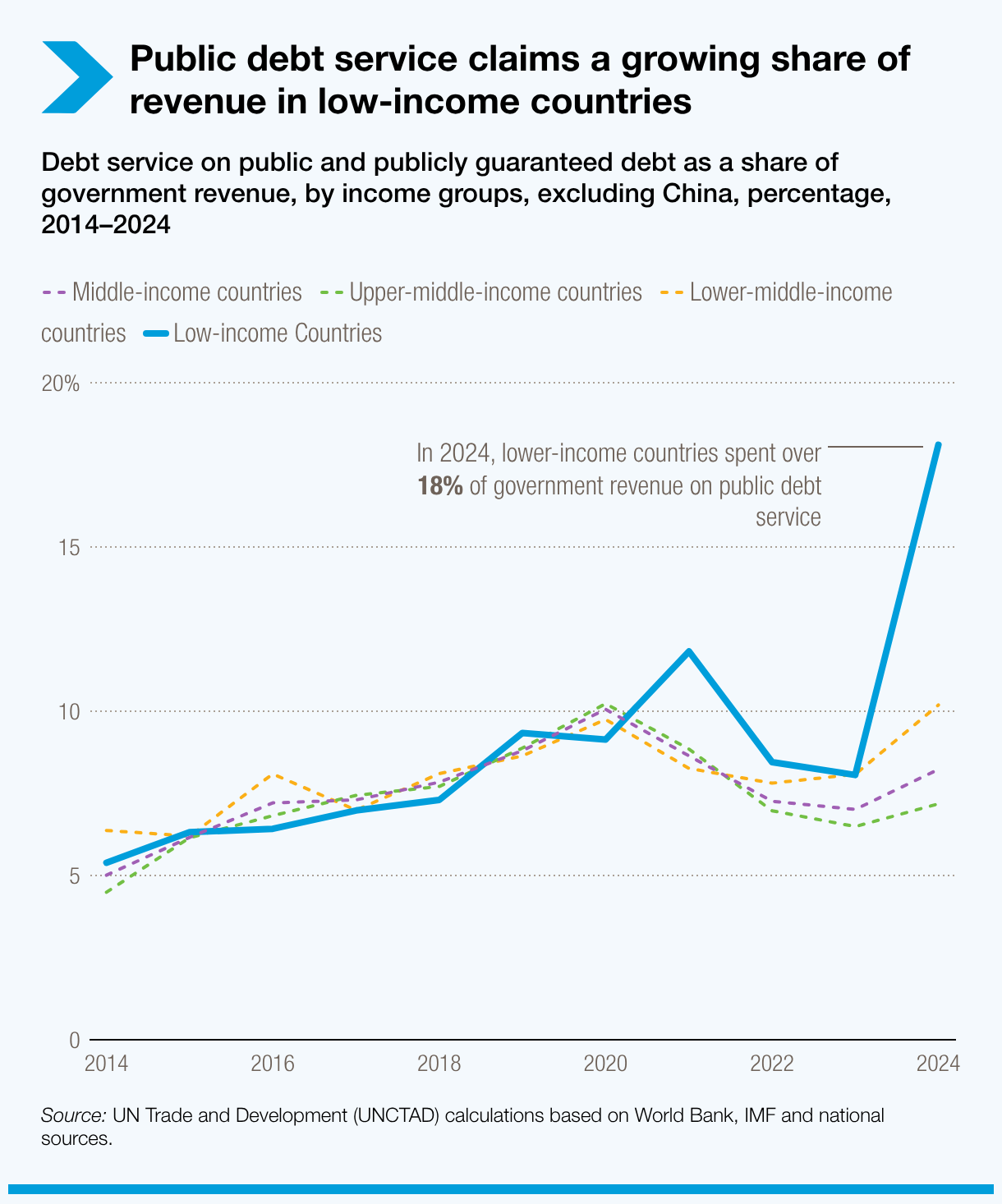

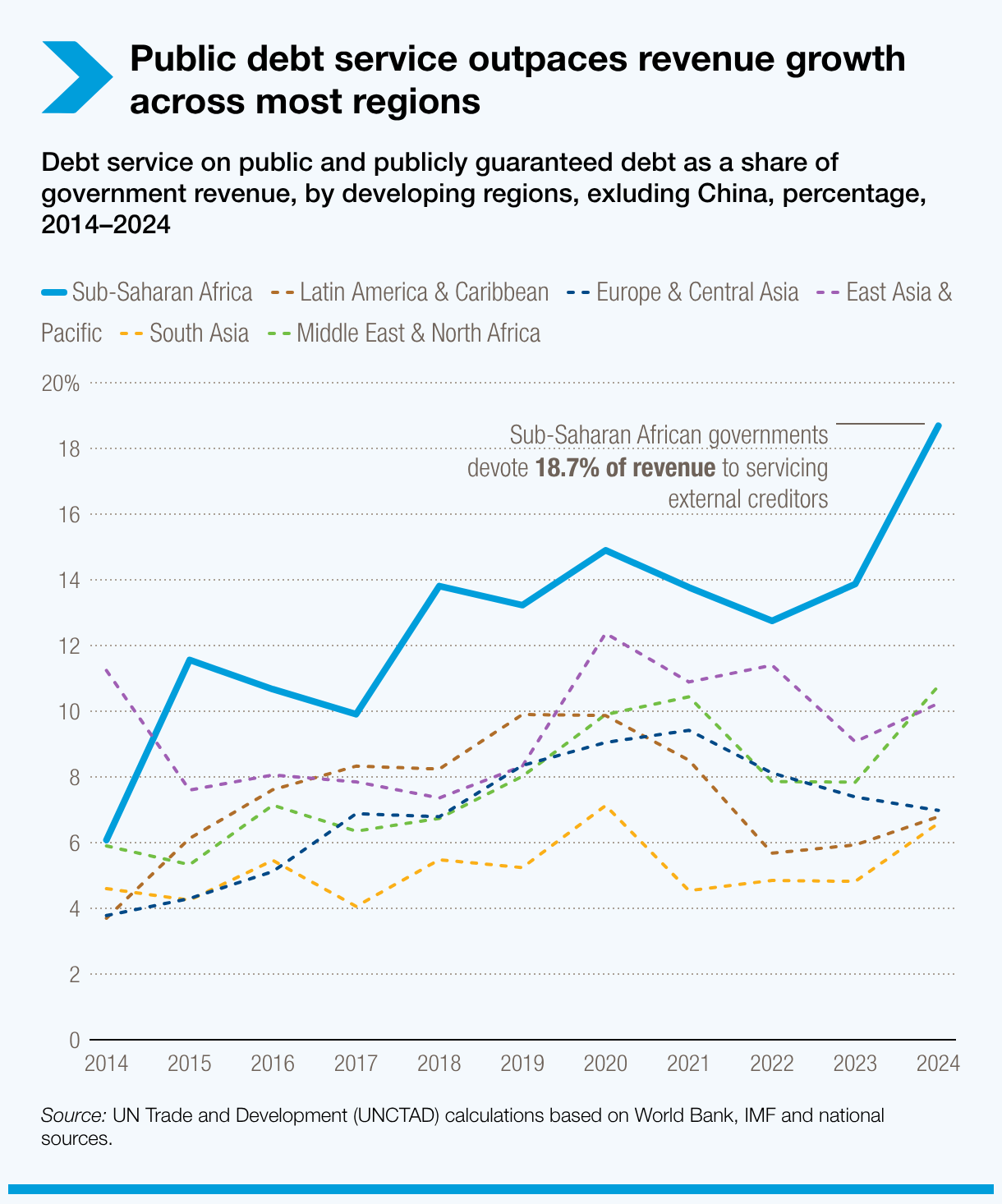

Although overall debt stocks and service levels appeared relatively stable, key debt sustainability indicators deteriorated across many developing countries. Excluding China, public and publicly guaranteed (PPG) external debt service in the Global South rose to 8.4% of government revenue in 2024, up from 7% in 2023.

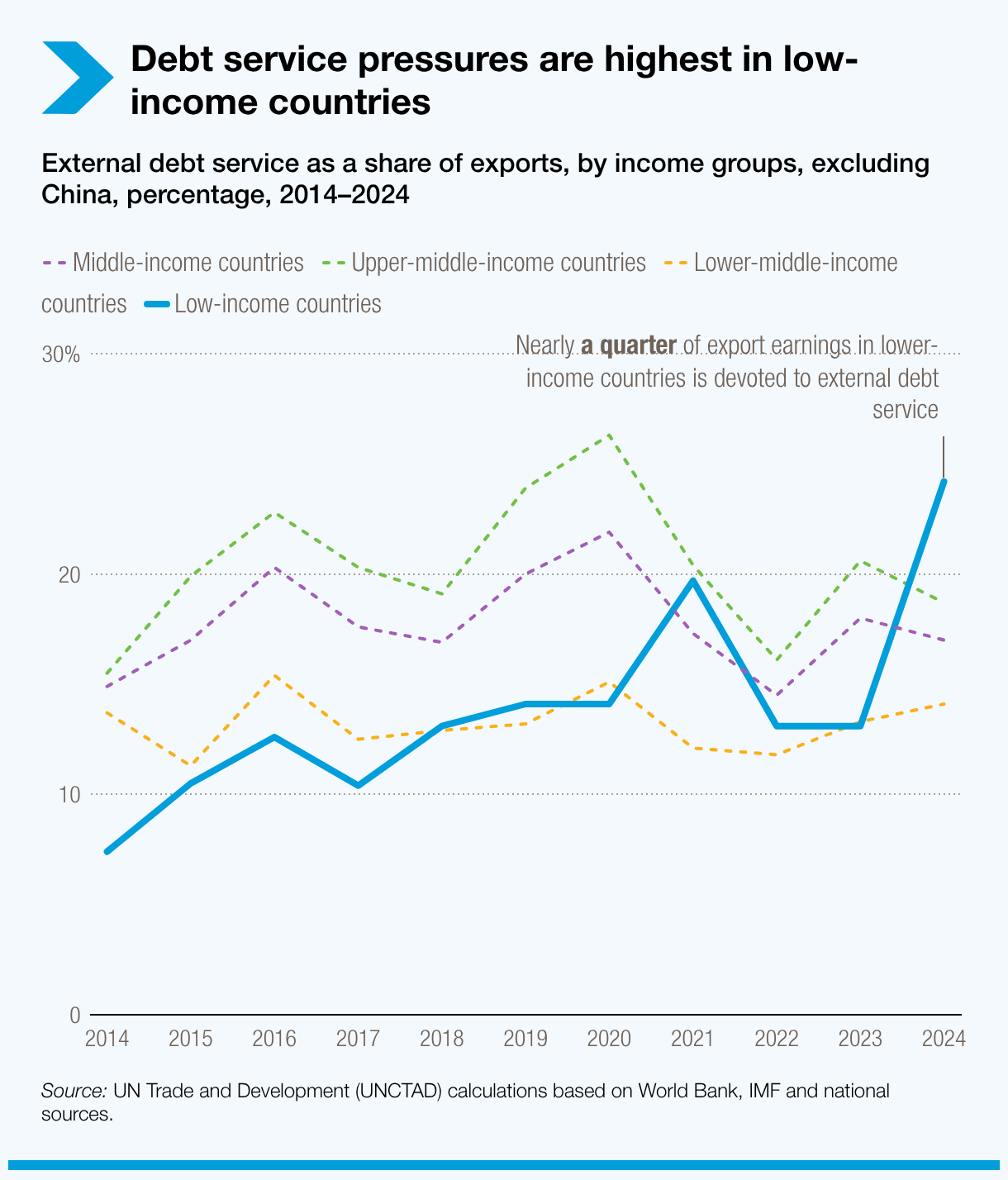

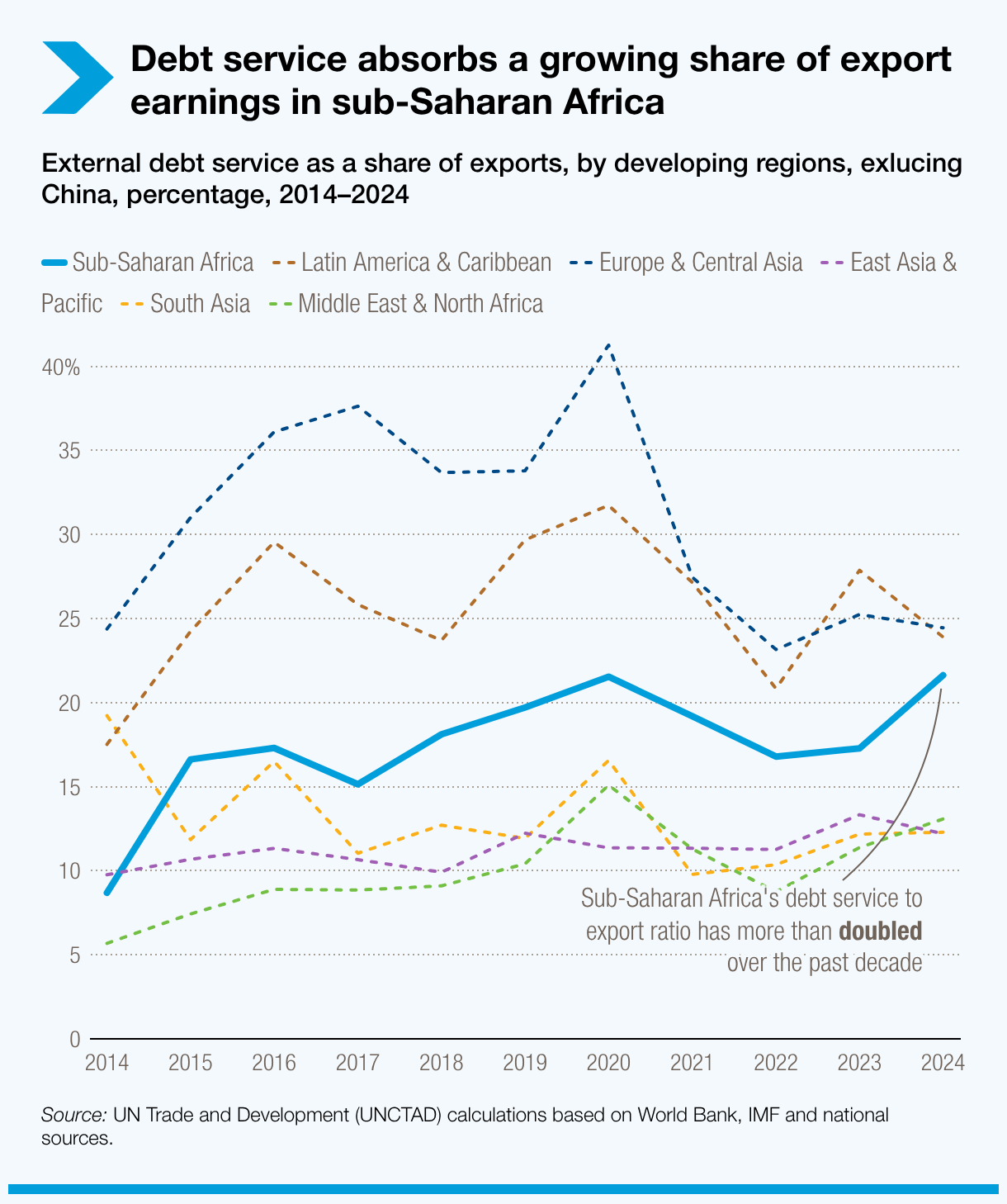

Total external debt service absorbed 16.3% of export earnings, down slightly from 17% in 2023. But the improvement was driven mainly by upper-middle-income countries, masking worsening conditions in low and lower-middle-income countries.

Low-income countries were hit hardest. Their debt service payments nearly doubled in 2024, as low economic growth and falling commodity prices squeezed exports and government revenue. They spent a record 24.2% of export earnings on external debt service and 18.1% of government revenue on servicing PPG debt. Lower-middle-income countries also saw their external debt sustainability deteriorate due to a wall of principal repayments falling due in 2024.

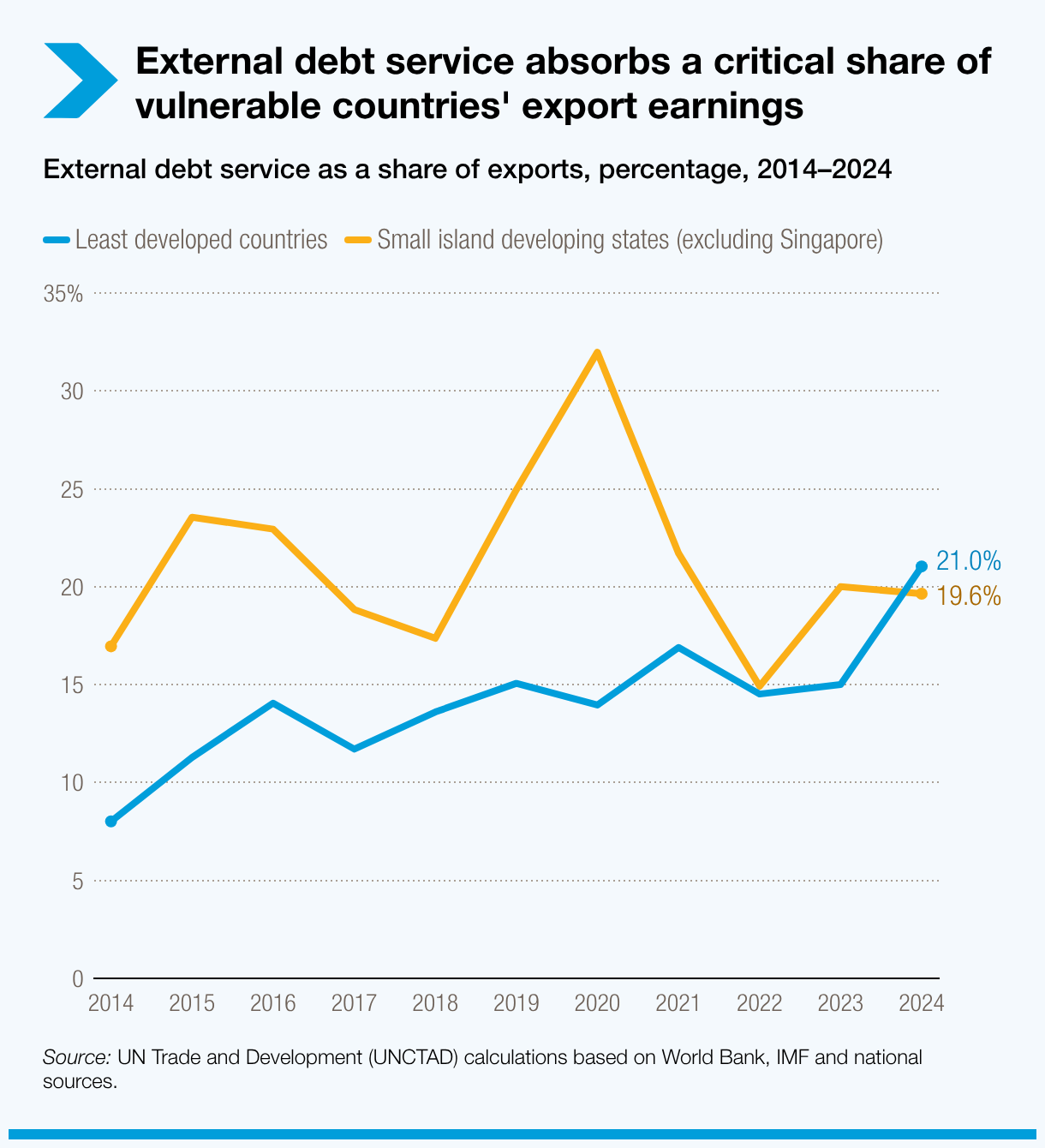

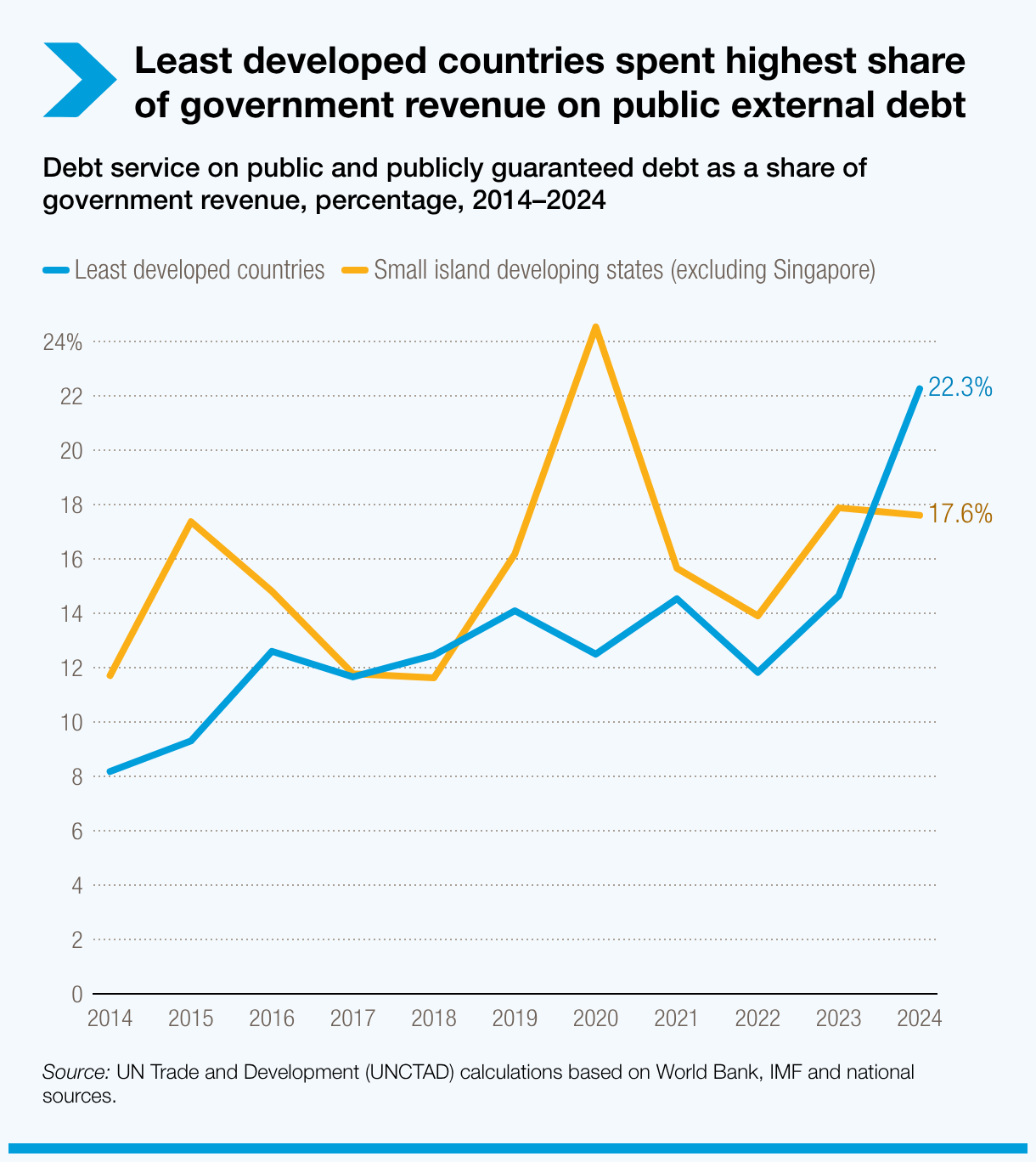

Debt sustainability also continued to deteriorate in least developed countries (LDCs), where economic growth slowed and government revenues weakened amid conflicts and rising geopolitical tensions. In 2024, LDCs spent around 22.3% of government revenue on servicing PPG debt – the highest share among all developing country groups – and 21% of export revenue on total external debt service.

Small island developing states saw a slight improvement following the sharp deterioration during the 2020 COVID-19 shock. A rebound in tourism – a key source of foreign exchange – and stronger economic growth helped reduce external debt service to 19% of export earnings and lower PPG debt service to 17.6% of government revenue in 2024. Even so, their debt burdens remain at critically high levels.

Across developing regions, public sector external debt sustainability deteriorated in 2024, except in Europe and Central Asia. Sub-Saharan Africa recorded the steepest decline, with governments spending 18.7% of revenues on servicing external public and publicly guaranteed debt – three times the level in 2014. The region’s ratio of total debt service to exports has more than doubled since then.

Aid declines even as financing needs rise

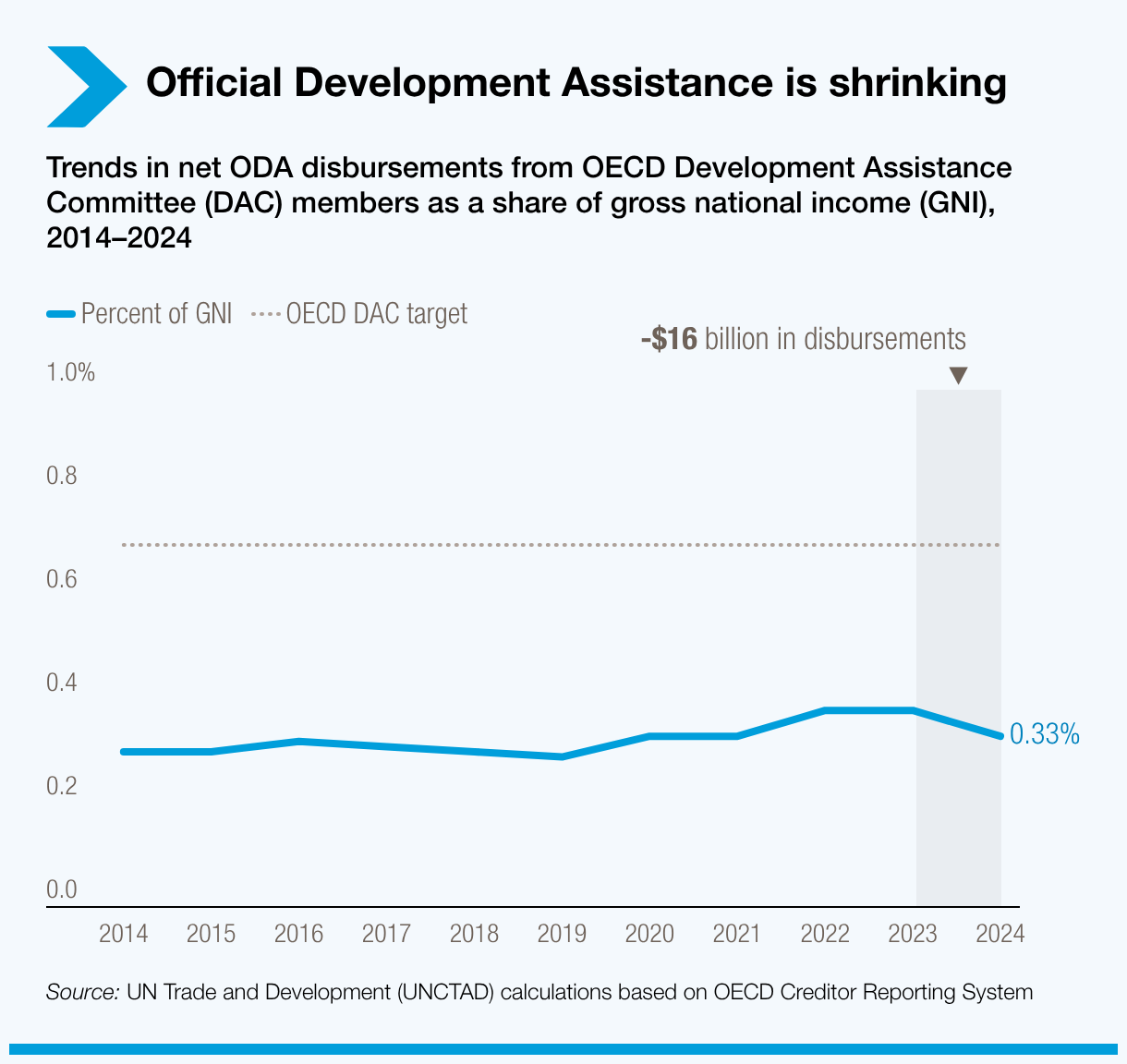

Official development assistance (ODA) has declined sharply, even as fiscal pressures intensify and the Sustainable Development Goal financing gap widens.

Development Assistance Committee (DAC) member countries disbursed 7.3% less ODA in 2024 than in 2023, reducing aid to only 0.3% of donor countries’ gross national income – less than half of the internationally agreed target.

Driven by shifting global priorities and new crises, the decline in low-cost development financing risks pushing the most vulnerable countries into a deeper debt and development crisis.

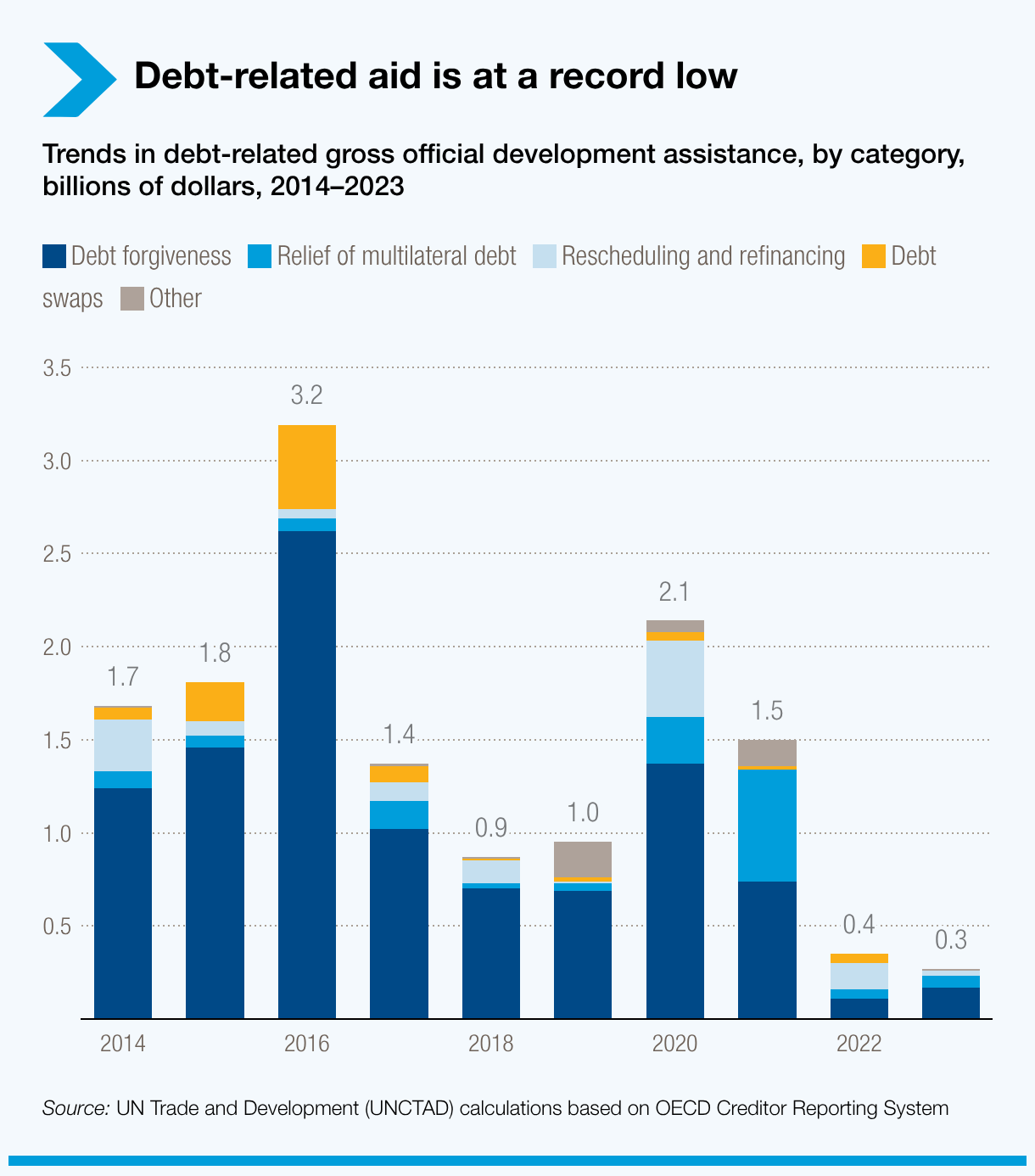

Debt-related ODA fell to a record low $270 million in 2023, following a temporary rise during the G20 Debt Service Suspension Initiative period (2020–2021). Aid for debt forgiveness, restructuring, rescheduling and refinancing has also decreased significantly, and bilateral debt-for-development swaps have almost completely disappeared.

How UNCTAD helps address debt and development challenges

UN Trade and Development (UNCTAD) plays a central role in helping developing countries address debt and development challenges through policy-oriented analysis, consensus-building and technical assistance.

A core pillar of this work is the Debt Management and Financial Analysis System (DMFAS) Programme, which strengthens national capacities to record, monitor and manage public debt and its risks. Effective debt management is essential to ensure countries can meet their debt obligations sustainably while making informed financial decisions – promoting transparency, fiscal sustainability and good governance.

In response to increasing complexity in debt portfolios, UNCTAD has launched a new generation of its debt management software (DMFAS 7), offering a more comprehensive and integrated solution. The programme currently supports 63 countries.

UNCTAD also supports different UN-led policy initiatives to address developing countries’ debt and development challenges. These include the Pact for the Future, adopted by member states in September 2024; the Expert Group on Debt appointed by the UN Secretary-General in December 2024; and the 4th International Conference on Financing for Development, whose outcome document, the Seville Commitment, points the way to improved development finance.

Policy recommendations

Achieving sustainable development while ensuring debt sustainability requires addressing both the cost and composition of debt. This means reducing existing debt stocks where necessary while also mobilising additional long-term, affordable and stable financing.

UNCTAD puts forward the following policy recommendations across three levels of action:

Actions at the multilateral level:

- Scale up affordable financing by multilateral and regional development banks.

- Enhance the global financial safety net to make it more effective, accessible and predictable for developing countries.

- Address the shortcomings of the G20 Common Framework for Debt Treatments.

- Reform debt sustainability analyses to make them sensitive to development.

- Create a borrower’s platform to serve as a venue for knowledge and experience sharing and elevate the collective voice of borrowers.

Actions at the country level that require coordination, technical assistance and capacity-building:

- Increase technical assistance and capacity-building for debt management offices.

- Provide technical assistance to support investment pipeline development.

- Promote the development of low-cost foreign currency guarantees and other hedging and currency conversion mechanisms.

- Establish a debt-for-development swap platform that provides information and technical assistance for developing countries.

Actions at the national level:

- Enhance the quality of investment project pipelines or country platforms.

- Reduce debt-swap transaction costs through scale and standardisation and align the associated key performance indicators with national development strategies.

- Improve the profile of existing debt stocks by changing the currency denomination, lowering its cost, and increasing its maturity.

- Enhance the communication strategy with investors and credit rating agencies.

- Market investment opportunities to non-traditional bilateral lenders.