As the world confronts intertwined climate and finance crises while seeking to advance on the Sustainable Development Goals (SDGs), carbon markets are increasingly seen as key drivers of climate ambition and capital flow.

They enable countries to trade carbon credits – permits to offset a specific amount of emissions – allowing sellers to earn revenue and contribute to climate action.

The least developed countries (LDCs) are already engaged in carbon markets and among the early movers in emerging trading mechanisms under Article 6 of the Paris Agreement.

The Least Developed Countries Report 2024 examines how these markets could bridge gaps between economic growth and climate action in LDCs and mobilize capital for sustainable development.

It makes clear that while carbon markets offer promise, they are not a substitute for official development assistance or climate finance. Instead, they serve as one of many tools to support LDCs’ green structural transformations and global emissions goals.

Using data-driven analysis and case studies, the report provides a roadmap for LDCs and their development partners to unlock the potential of carbon markets for sustainable growth.

» See the map and list of the 45 LDCs

Navigating fragmented,

complex global carbon markets

While LDCs contribute less than 4% of global emissions, they bear some of the most severe climate impacts.

Under certain conditions, carbon markets offer these countries a potential pathway to bridge critical funding gaps, helping finance renewable energy, conservation and infrastructure projects, while supporting emissions reductions and technology transfer.

However, global carbon markets remain fragmented and uncertain, split between compliance markets under the Paris Agreement and voluntary markets driven by private entities.

Compliance markets, structured around Emissions Trading Systems (ETSs), differ in scope, design and pricing. In December 2023, for instance, the European Union’s ETS traded at $77.36 per ton of CO2 – over ten times the price in the Republic of Korea’s ETS.

Voluntary markets present their own challenges. After peaking in 2021 at 362 million metric tons of carbon dioxide equivalent (MtCO2e), demand has since declined amid concerns about greenwashing. By 2023, the stock of unretired credits reached 877 MtCO2e. Carbon futures prices tumbled to historic lows in 2023 and 2024, deepening market uncertainty.

While participation in carbon markets under Article 6 of the Paris Agreement could unlock significant financial benefits for LDCs, access alone is not enough. Resilient policies, high standards and a cohesive market framework are essential to support equitable participation.

UN Trade and Development calls for the international community to

-

1Develop policies that enhance LDC access to compliance markets, emphasizing the need for inclusion in schemes like Emissions Trading Systems.

-

2Address market fragmentation by establishing standardized rules and protocols that make it easier for LDCs to navigate and participate in global carbon markets.

-

3Enhance carbon market trust, integrity, transparency and credibility by adopting and implementing forthcoming UN principles for carbon markets.

Seizing opportunities and

overcoming challenges in carbon markets

Carbon markets offer LDCs a potential pathway to additional finance for climate resilience and sustainable development, but capturing significant revenue remains challenging. Most carbon credit revenues benefit others, while structural barriers limit returns for LDCs.

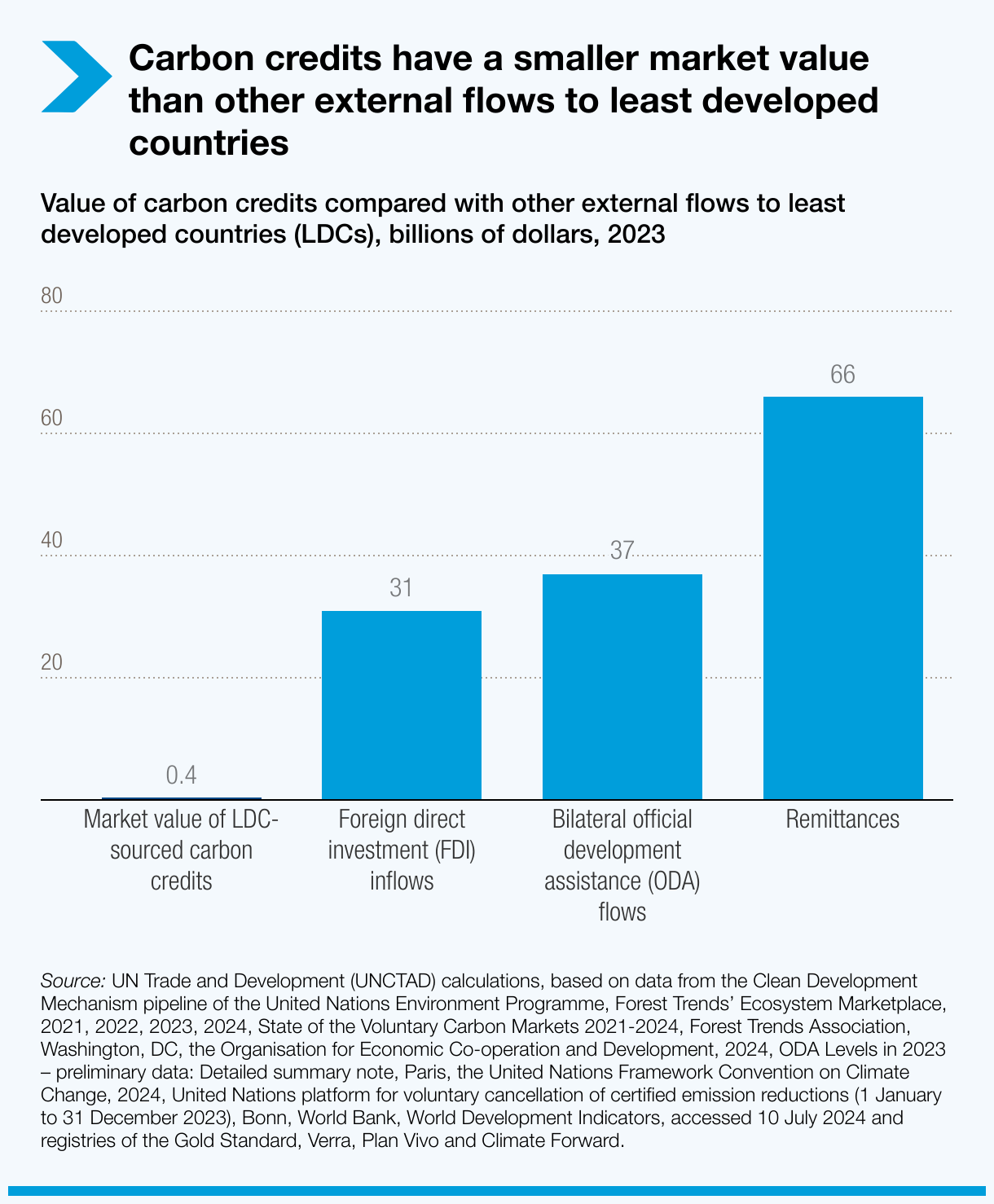

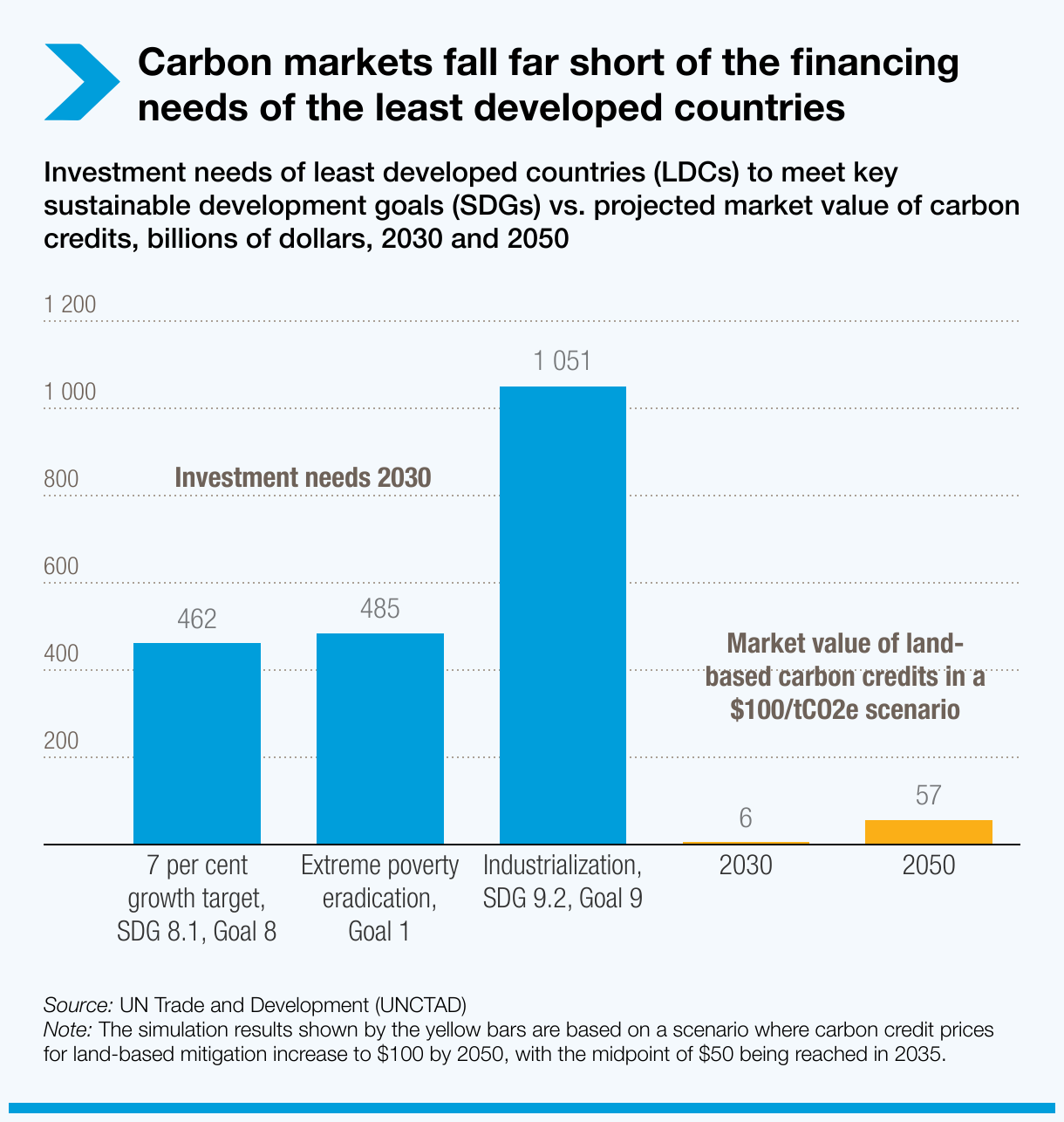

So far, these markets have provided limited funding compared to other sources. In 2023, LDC-sourced carbon credits were valued at $403 million – just 1% of net bilateral official development assistance and far below the $1 trillion needed annually for some SDG targets, such as inclusive and sustainable industrialization (SDG 9.2).

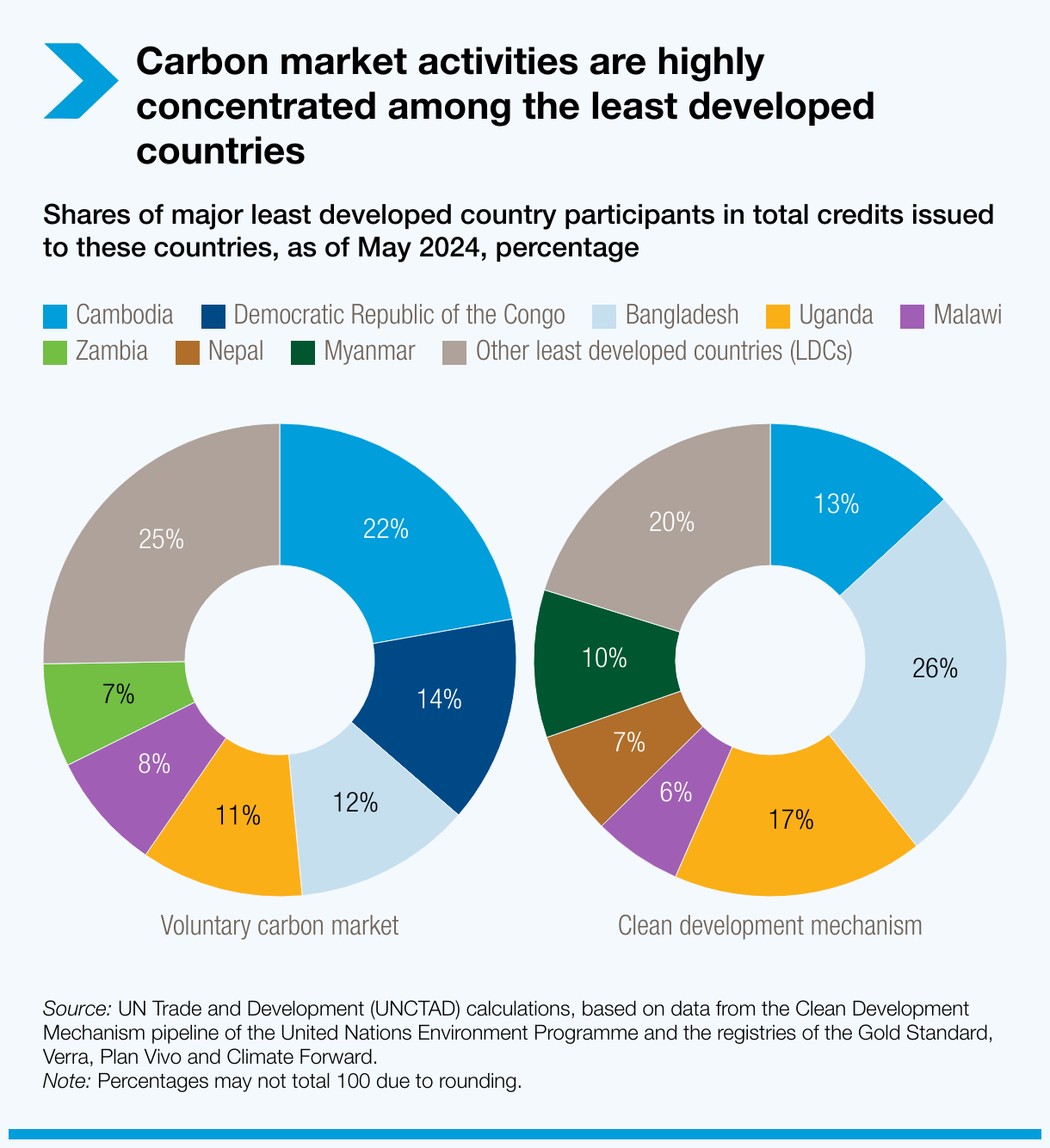

Market concentration in LDCs poses challenges. Since 2020, voluntary markets have been LDCs' primary credit source, focused mainly on nature-based solutions (52%). Under the Clean Development Mechanism (CDM), however, renewable energy dominates at 41%, offering promising support for LDC energy needs.

Geographic concentration is also evident. Just six LDCs account for over 75% of all voluntary market credits and 80% of CDM credits.

LDCs have significant land-based mitigation potential, equal to 70% of global aviation’s 2019 CO2 emissions. Yet, from 2020 to 2023, only 2% of this potential was realized, limited by low project feasibility and low carbon prices. If prices remain around $10 per ton, 97% of the mitigation potential will likely remain unused by 2050.

Transferred emissions add another challenge, as emissions transferred out of an LDC don’t count toward its targets, often requiring the country to pursue additional, costlier mitigation efforts to meet its own climate goals.

For LDCs, effectively leveraging carbon markets requires strategic management of these opportunities and risks.

UN Trade and Development calls for:

-

1LDCs to establish proactive, independent policy frameworks that set clear objectives, priorities and engagement strategies for carbon trading.

-

2Development partners to strengthen capacity-building initiatives, equipping LDCs with the skills and resources necessary for effective carbon market participation.

-

3Development partners to enhance LDC access to compliance markets under Article 6 to secure predictable funding flows and foster equitable participation.

-

4The international community to set high-integrity certification standards to ensure transparency, credibility and genuine environmental impact of carbon credits generated in LDCs.

-

5Investors to diversify support for carbon projects in LDCs beyond nature-based initiatives, expanding into renewable energy and other high-impact areas to unlock LDCs' mitigation potential.

Drawing lessons from

LDCs' experiences in carbon markets

Evidence is limited that LDCs gained significant capabilities from hosting carbon projects under the Kyoto Protocol, which could ease their transition to Article 6 of the Paris Agreement. Case studies suggest that the anticipated benefits of carbon markets – such as technology transfer, education and community development – are uncertain for LDCs.

LDC participation in the Kyoto Protocol’s Clean Development Mechanism (CDM) was hindered by structural constraints, like their small economies and limited capacity to attract foreign investment.

By the end of 2023, the 45 LDCs accounted for just 1.5% of the 7,842 CDM projects. They registered only 217 projects from 2004 to 2020, with most occurring after 2013.

Although 32 of the 45 LDCs have some CDM experience, most of the activity was concentrated in just 12 countries. The majority hosted fewer than five projects. External developers managed most compliance aspects, resulting in limited skill-building for LDCs in project design and oversight, as well as few financial or technological co-benefits.

These findings highlight the need for greater attention to ensuring carbon markets contribute effectively to sustainable development, with more emphasis on equitable terms to support meaningful LDC participation.

Many LDCs still lack the infrastructure, technology and institutional capacity needed for meaningful participation. Strengthening their domestic regulatory institutions and frameworks for carbon markets will be essential but requires significant upfront investment.

UN Trade and Development calls for development partners to:

-

1Strengthen capacity-building in LDCs to enhance the quality of participation in carbon markets, based on their needs for human resources and skills, laws, regulations and institutions.

-

2Differentiate carbon finance from climate finance to ensure funds raised through carbon markets are additional to the $100 billion annual climate finance goal and other development finance commitments.

-

3Invest in programmes that enhance LDC capabilities in carbon project design, development and verification, reducing dependence on external developers and build in-country expertise.

-

4Encourage carbon projects that support knowledge transfer, technology upgrades and capacity-building, aligning projects with LDC national development plans to ensure benefits extend beyond carbon finance alone.

Strengthening domestic policies and

institutions for carbon market success

Among the 45 LDCs, 32 plan to leverage carbon markets to meet their Nationally Determined Contribution (NDC) targets, requiring $1.48 trillion by 2030 to achieve these commitments.

Effective participation demands strong state involvement, particularly for LDCs, to manage partnerships for transferred mitigation outcomes (Article 6.2), global carbon trading (Article 6.4) and non-market approaches (Article 6.8) that support finance, technology and capacity-building.

Participation in Article 6 mechanisms requires substantial infrastructure, including national registries and rigorous monitoring, reporting, and verification protocols. While some LDCs are updating policies in preparation, additional resources are crucial to bridge gaps in institutional readiness.

While carbon market revenues can support domestic climate efforts, they should not replace climate finance, as carbon markets do not adhere to the principle of common but differentiated responsibilities, which acknowledge LDCs’ lower historical emissions and current development needs.

To optimize resources, LDCs could explore regional frameworks with shared inventories, monitoring bodies and standards, leveraging South-South cooperation to manage costs.

Article 6.8 of the Paris Agreement provides a framework for non-market approaches, which could further unlock financial, technological and capacity-building support for LDCs. This could complement carbon market activities and support broader climate and structural transformation. However, current resource commitments toward these initiatives have fallen short of the identified needs.

UN Trade and Development calls for LDCs to:

-

1Align carbon market policies with development goals to ensure market participation actively supports national priorities.

-

2Leverage carbon markets as part of broader structural transformation efforts, complementing other policies like industrial policy, fiscal policy, and policies for science, technology and innovation.

-

3Strengthen national regulatory institutions for carbon markets, developing robust laws, regulations, and monitoring, reporting and verification systems.

-

4Establish clear domestic regulations for carbon project operations and benefit-sharing, specifying rules for participation, revenue distribution and emissions reductions retained by the host country.

-

5Explore South-South cooperation at regional or subregional levels to jointly establish institutions that might otherwise be too costly for individual countries.

UN Trade and Development calls on development partners to

-

1Support LDCs in building capabilities to integrate carbon market policies into broader policies aimed at structural transformation, prioritizing collaborative approaches to technical cooperation.

-

2Implement the principle of common but differentiated responsibilities within multilateral carbon market regulations, ensuring provisions for LDCs that recognize their lower emissions and special development needs.

-

3Strengthen institutional frameworks in LDCs to ensure effective participation in Article 6 mechanisms, including robust monitoring, reporting and verification systems.

-

4Provide targeted capacity-building and technical support to enable LDCs to develop the necessary infrastructure and expertise to effectively engage in compliance and voluntary carbon markets.

-

5Enhance funding commitments under Article 6.8 to provide critical non-market support, such as finance, technology transfer and capacity-building, enabling LDCs to fulfil their Nationally Determined Contributions.

LDC facts and figures

Where are LDCs located?

The UN established the LDC category 51 years ago. The list of LDCs has expanded from an initial 25 countries in 1971, peaking at 52 in 1991, and stands at 45 today, with only seven countries having graduated – stopped being an LDC – to date.

They are distributed among the following regions:

- Africa (33): Angola, Benin, Burkina Faso, Burundi, Central African Republic, Chad, Comoros, Democratic Republic of the Congo, Djibouti, Eritrea, Ethiopia, Gambia, Guinea, Guinea-Bissau, Lesotho, Liberia, Madagascar, Malawi, Mali, Mauritania, Mozambique, Niger, Rwanda, Sao Tome and Principe, Senegal, Sierra Leone, Somalia, South Sudan, Sudan, Togo, Uganda, United Republic of Tanzania and Zambia.

- Asia (8): Afghanistan, Bangladesh, Cambodia, Lao People’s Democratic Republic, Myanmar, Nepal, Timor-Leste and Yemen.

- Caribbean (1): Haiti.

- Pacific (3): Kiribati, Solomon Islands and Tuvalu.

See UNCTAD's page about the least developed countries for more information.

How do countries ‘graduate’ from least developed country status?

The list of LDCs is reviewed every three years by the Committee for Development Policy (CDP), a group of independent experts who report to the UN Economic and Social Council (ECOSOC). Following a triennial review of the list, the CDP may recommend to ECOSOC, countries for addition to the list or graduation from LDC status.

To graduate from the LDC category, a country must meet the established graduation thresholds of at least two of the three criteria for two consecutive triennial reviews: namely: (i) income per capita, (ii) an index of human assets, and (iii) an index of economic and environmental vulnerability.

Countries that are highly vulnerable, or have very low human assets, are eligible for graduation only if they meet the other two criteria by a sufficiently high margin. As an exception, a country whose per capita income is sustainably above the “income-only” graduation threshold, set at three times the graduation threshold, becomes eligible for graduation, even if it fails to meet the other two criteria.

The seven countries that have graduated from least developed country status since the creation of the category are:

- Botswana in December 1994

- Cabo Verde in December 2007

- Maldives in January 2011

- Samoa in January 2014

- Equatorial Guinea in June 2017

- Vanuatu in December 2020

- Bhutan in December 2023