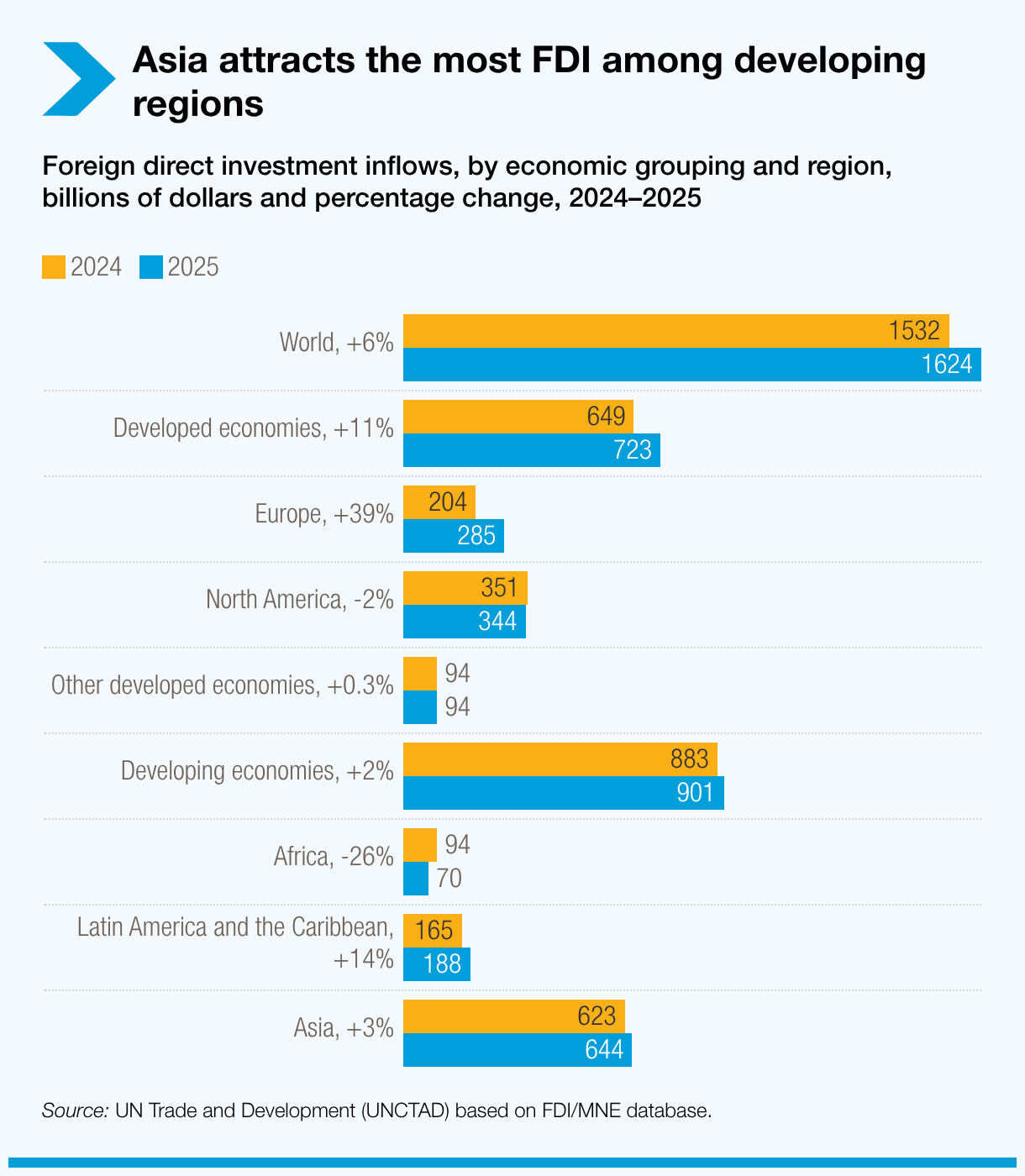

- Developing Asia attracted $644 billion in foreign direct investment (FDI) in 2025, remaining the world's largest developing-region recipient.

- South-East Asia overtook East Asia as the region's largest recipient subregion.

- India recorded a 44% increase in inflows, helping drive growth in South Asia.

- FDI remains highly concentrated, with eight of the ten largest developing-economy recipients located in Asia.

© Shutterstock/Abdul Razak Latif | An engine assembly plant in kedah, Malaysia.

Developing Asia remained the world's largest destination for foreign direct investment among developing regions in 2025. But the region's significance increasingly lies not only in the volume of investment it attracts, but also where within the region that investment is going.

That shift matters for development because FDI can help economies move into higher-value production, digital services, logistics and regional supply chains, but only if investment is connected to domestic firms, skills and infrastructure.

According to the World Investment Report 2026 by UN Trade and Development (UNCTAD), developing Asia received $644 billion in FDI in 2025. This represented about 40% of global FDI and more than 70% of flows to developing economies.

At the same time, investment patterns within the region continued to shift as companies reassessed supply chains, governments competed for new industries and investors looked for growth opportunities in an increasingly uncertain global economy.

Asia is not only attracting investment. It is increasingly shaping where future industries are being built, even as investment patterns within the region change. China remained one of the world’s largest FDI recipients, despite a decline in inflows from about $116 billion to $105 billion, while continuing to attract commitments in higher value-added activities, research and development and pharmaceutical manufacturing.

Overall, the region’s FDI performance reinforces Asia's central role in global investment decisions, while also showing that the balance within Asia itself continues to evolve.

South-East Asia gains ground

One of the most notable developments in 2025 was the rise of South-East Asia as the largest recipient subregion in developing Asia.

While inflows declined in East Asia, investment increased in South-East Asia, South Asia, West Asia and Central Asia. India played a major role in that shift, recording a 44% increase in FDI inflows and helping drive growth across South Asia.

At the country level, concentration remains high: eight of the ten largest developing-economy recipients of FDI are in Asia, together accounting for about 60% of total inflows to developing economies and more than 80% of regional inflows.

Taken together, the subregional shifts and country-level concentration suggest that investment opportunities are spreading across more parts of Asia, even though the largest and most competitive economies continue to capture the bulk of flows. Countries across Asia are increasingly competing for projects linked to manufacturing, services, logistics and emerging industries.

Why Asia matters in a changing investment landscape

The shifts taking place in Asia reflect wider changes in the global economy.

Around the world, investment is increasingly flowing into sectors linked to semiconductors, digital infrastructure, artificial intelligence, advanced manufacturing and energy-transition technologies and services. Together, these industries accounted for 44% of global greenfield investment in 2025, up from 16% five years earlier.

Many Asian economies enter this period with important advantages, including established manufacturing capacity, supplier networks, large consumer markets, growing industrial ecosystems and deep integration into regional production networks. But these advantages are uneven and not all economies can compete for the same projects.

These strengths have helped the region to benefit from changes in global investment patterns, even as competition for capital becomes more intense.

For policymakers, the priority is not simply to offer more incentives. The report points to the need for investment facilitation, stronger supplier ecosystems, reliable energy and logistics, workforce skills and regional integration that allows smaller economies to connect to larger production networks. These policies can help turn investment inflows into industrial upgrading and wider development gains.

The next phase will be more competitive

Success in attracting investment is becoming harder to take for granted.

Governments across the world are using industrial policies, including incentives and other tools to attract projects linked to future growth industries. Investors, meanwhile, are becoming more selective about where they commit long-term capital.

For Asian economies, the challenge is no longer simply attracting foreign investment. It is remaining competitive in a world where capital, technology and industrial capabilities are increasingly concentrated in sectors seen as strategic.

Asia remains central to the new investment landscape, but the next phase will depend on which economies can connect foreign investment to industrial upgrading, jobs, supplier networks and broader regional development.