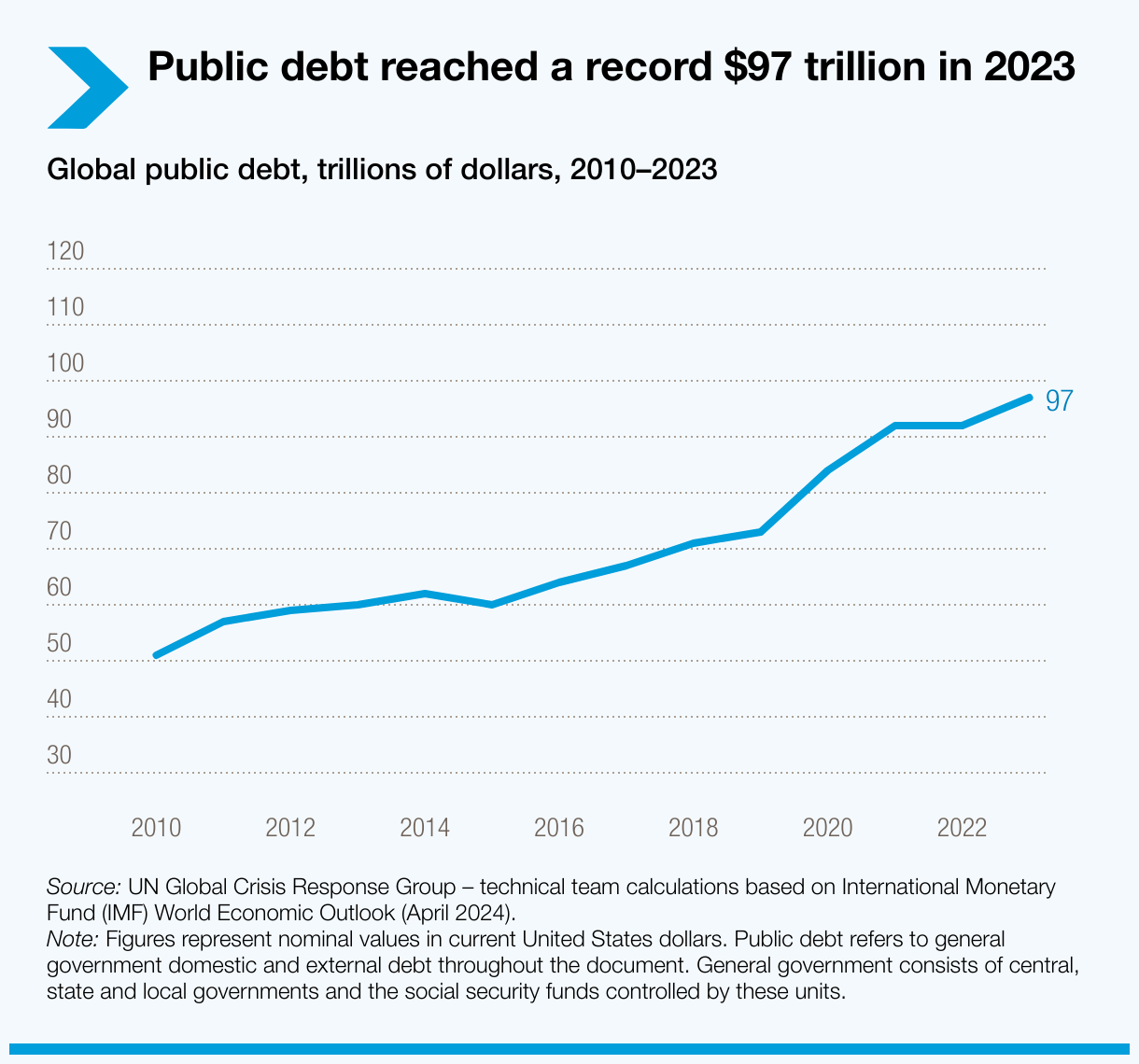

Global public debt has doubled since 2010, reaching a historic $97 trillion in 2023. More than 40% of the world’s population live in countries that spend more on debt interest payments than on education or health.

As UN Trade and Development (UNCTAD) celebrates its 60th anniversary, it’s crucial to examine issues that will shape the future of trade and development.

The "Forward together" series explores pivotal topics that hold big promises and significant challenges for developing countries, such as public debt.

Forward together series

- Navigating the growing challenges of public and external debt

- Making e-commerce and the digital economy work for all

- Building more diverse and resilient economies

- Making trade work better for the planet

Rising public debt profoundly constrains economic growth and limits investment in sectors critical for development, such as infrastructure, healthcare and education. High public debt also leads to a vicious cycle of borrowing and repayment, risking defaults and economic crises, as seen during the 1980s Latin American debt crisis – a period often referred to as a “lost decade”.

Global public debt has doubled since 2010, reaching an all-time high of $97 trillion in 2023. Currently, about 3.3 billion people – more than 40% of the world’s population – live in countries that spend more on debt interest payments than on education or health.

"There is an alarming tendency among the international community to regard debts in the developing world as sustainable because they can, after some sacrifice, be paid off,” UN Trade and Development Secretary-General Rebeca Grynspan says.

“This view overlooks the skipped meals, foregone investment in education, and lack of health spending, not to mention reduced investment in infrastructure, that forcibly make room for interest payments."

A looming widespread debt crisis

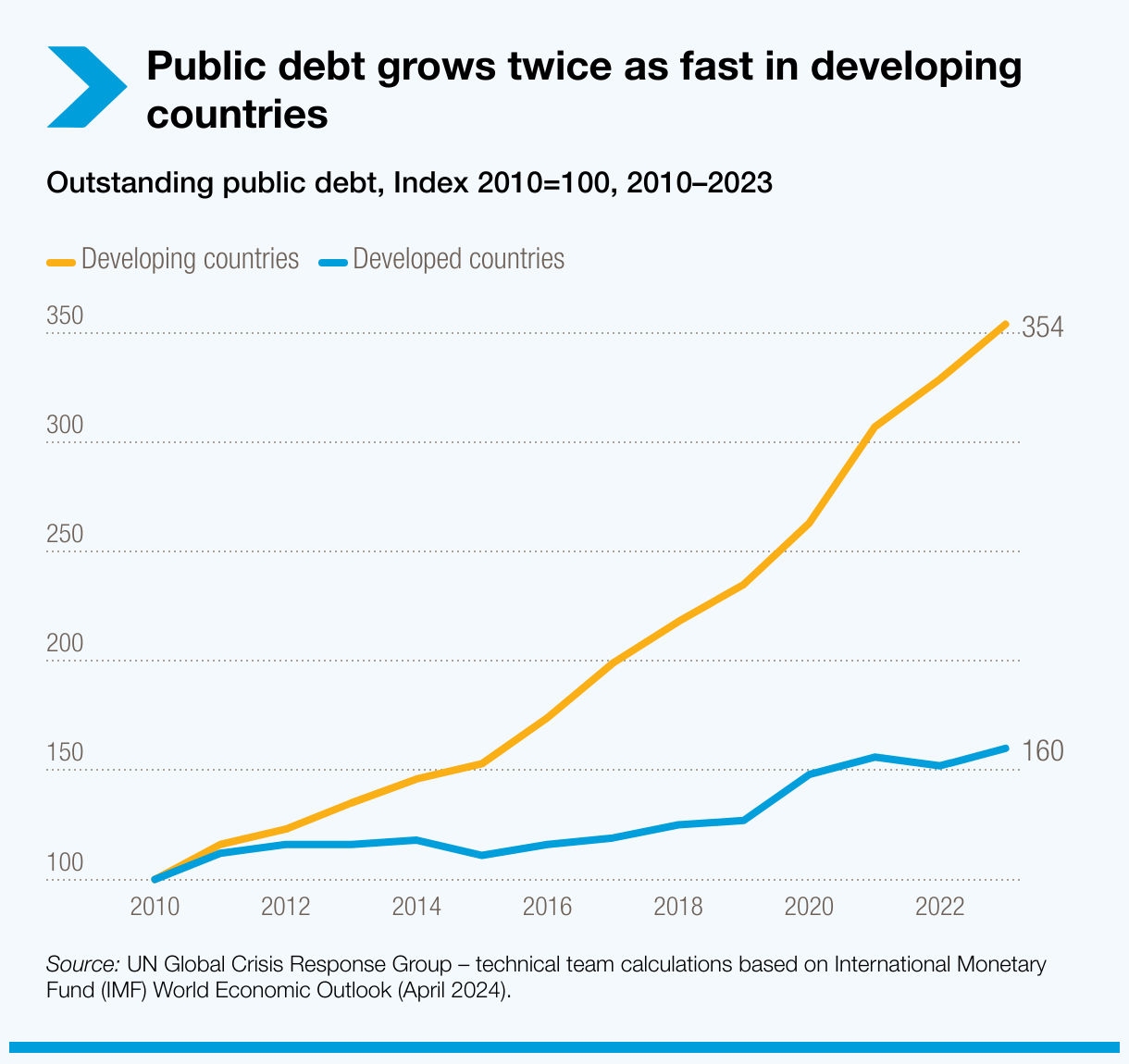

Over the past decades, developing countries have seen a significant increase in external public debt, driven by a combination of factors such as borrowing for development projects, fluctuating commodity prices and the need to finance deficits.

The COVID-19 pandemic exacerbated the situation, as countries borrowed extensively to mitigate the economic fallout and support public health measures.

By the end of 2022, developing countries’ external debt – funds borrowed in foreign currency – had increased by 15.7% to $11.4 trillion. With half of low-income countries and close to a quarter of emerging market economies in or near debt distress, the possibility of a global debt crisis is high.

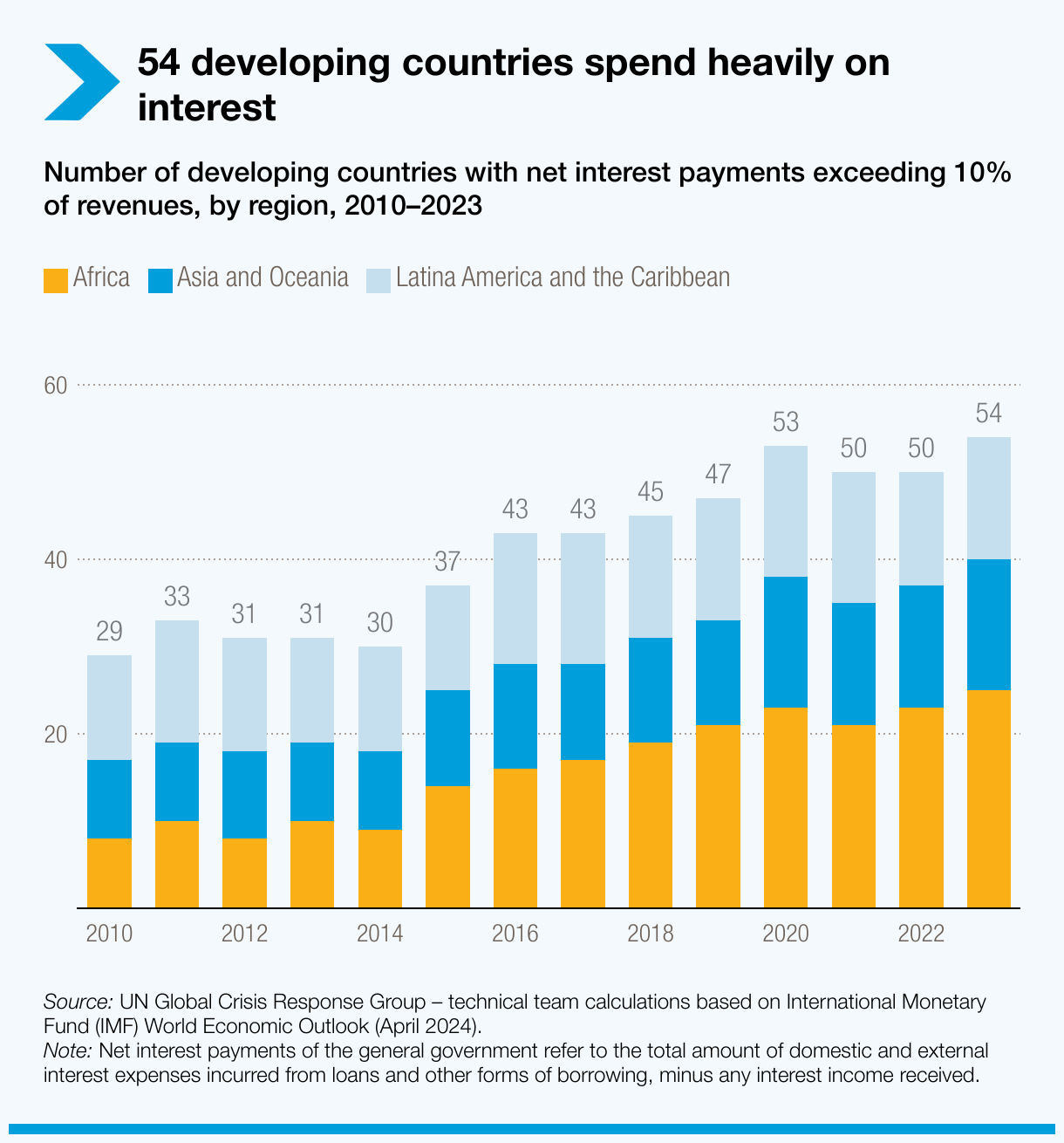

Equally alarming is the surge in public debt servicing costs, limiting budgets in developing countries.

In 2023, developing nations paid $847 billion in net interest, a 26% increase from 2021. They borrowed internationally at rates two to four times higher than the U.S. and six to 12 times higher than Germany. Moreover, in 2023, a historic 54 developing nations, with almost half in Africa, dedicated a minimum of 10% of government funds to debt interest payments.

UN Trade and Development’s role in supporting developing countries in their efforts to manage public debt

Through research, technical cooperation, and consensus building, UN Trade and Development helps developing countries manage public debt more effectively and advocates for realigning international debt architecture to meet their needs.

Research and analysis

We conduct rigorous research and policy analysis to inform global and national debt management strategies. We provide timely analysis of the most important developments and emerging issues in international debt.

Key publications include the annual Trade and Development Report and the United Nations Secretary-General´s report to the General Assembly on external debt, which analyze the key issues related to external debt in developing countries and facilitates negotiations on the debt resolution in the General Assembly.

Technical cooperation

We adapt our technical assistance to meet the changing debt needs of developing countries.

For example, since 1981, the Debt Management and Financial Analysis System (DMFAS) programme has helped more than 115 institutions in 75 countries, including least developed countries such as Mauritania and Chad, strengthen their capacity to manage public debt effectively.

By providing debt management tools and training, the programme enables countries to better record, monitor, analyze and report on their public finances and debt portfolios.

Our Sustainable Development Finance Assessment analyzes the COVID-19 crisis's impact on the external financial and public debt sustainability of selected developing countries. It identifies the finance needs of these countries to achieve key SDGs while ensuring compatibility with financial and debt sustainability.

Consensus building

UN Trade and Development organizes the biennial International Debt Management Conference. It brings together senior-level national and international debt managers and experts from around the world to discuss some of the most pertinent topics in external and domestic debt, debt management and public finance.

Similarly, we hold an annual intergovernmental group of experts meeting on financing for development, providing a forum to discuss issues and challenges in implementing the Addis Ababa Action Agenda to finance sustainable development and the 2030 Agenda for Sustainable Development. Also, we contribute to the G20 International Financial Architecture Working Group.

Central to the organization's consensus-building efforts are debt sustainability frameworks. In collaboration with international organizations, we promote these frameworks to guide responsible borrowing and maintain manageable debt levels.

Additionally, UN Trade and Development advocates for fair and transparent debt restructuring processes, supporting international discussions and negotiations to ensure inclusive and equitable debt relief measures.

Forward together towards sustainable and inclusive debt solutions

UN Trade and Development calls for comprehensive reform of the global financial architecture to prevent a widespread debt crisis and create a more sustainable, inclusive system.

Key recommendations include:

- Boosting concessional loans and grants. Increase the base capital of multilateral and regional banks to expand their lending capacity. Issue special drawing rights (SDRs), a type of international currency the IMF created for member countries to boost their monetary reserves.

- Enhancing transparency in financing terms and conditions. Reduce resource and information asymmetry between borrowers and lenders and introduce legislative measures to discourage predatory lending practices.

- Expanding developing countries’ access to foreign currencies through central bank swaps.

- Enhancing their resilience during external crises. Implement standstill rules on debtors’ obligations, such as climate-resilient debt clauses, to allow a halt in debt repayments and provide breathing space for crisis management.

- Developing rules for automatic restructurings within the global debt architecture and a better global financial safety net.

- Establishing a global debt authority to coordinate and guide sovereign debt restructurings.

As we look to the future, UN Trade and Development remains committed to supporting developing countries in navigating the complexities of external public debt. Through rigorous analysis, collaboration and forward-looking recommendations, we can realign the global debt architecture with developing countries’ needs.