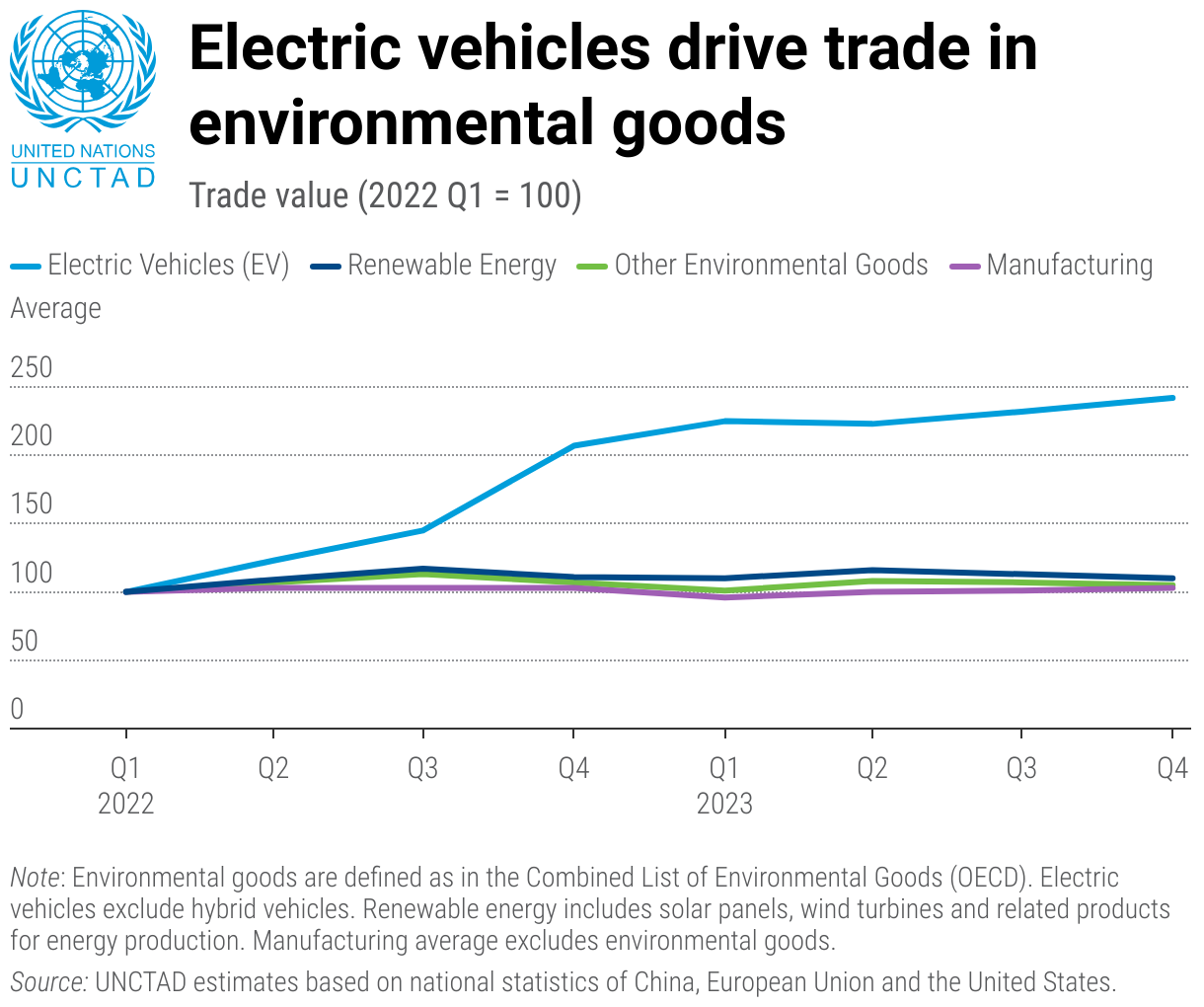

The overall outlook for trade in 2024 is positive, with increasing demand for environmental goods, especially electric cars, set to play a crucial role in driving growth.

© Shutterstock/seyephoto | Shipping containers in the Port of Ambarli, Türkiye.

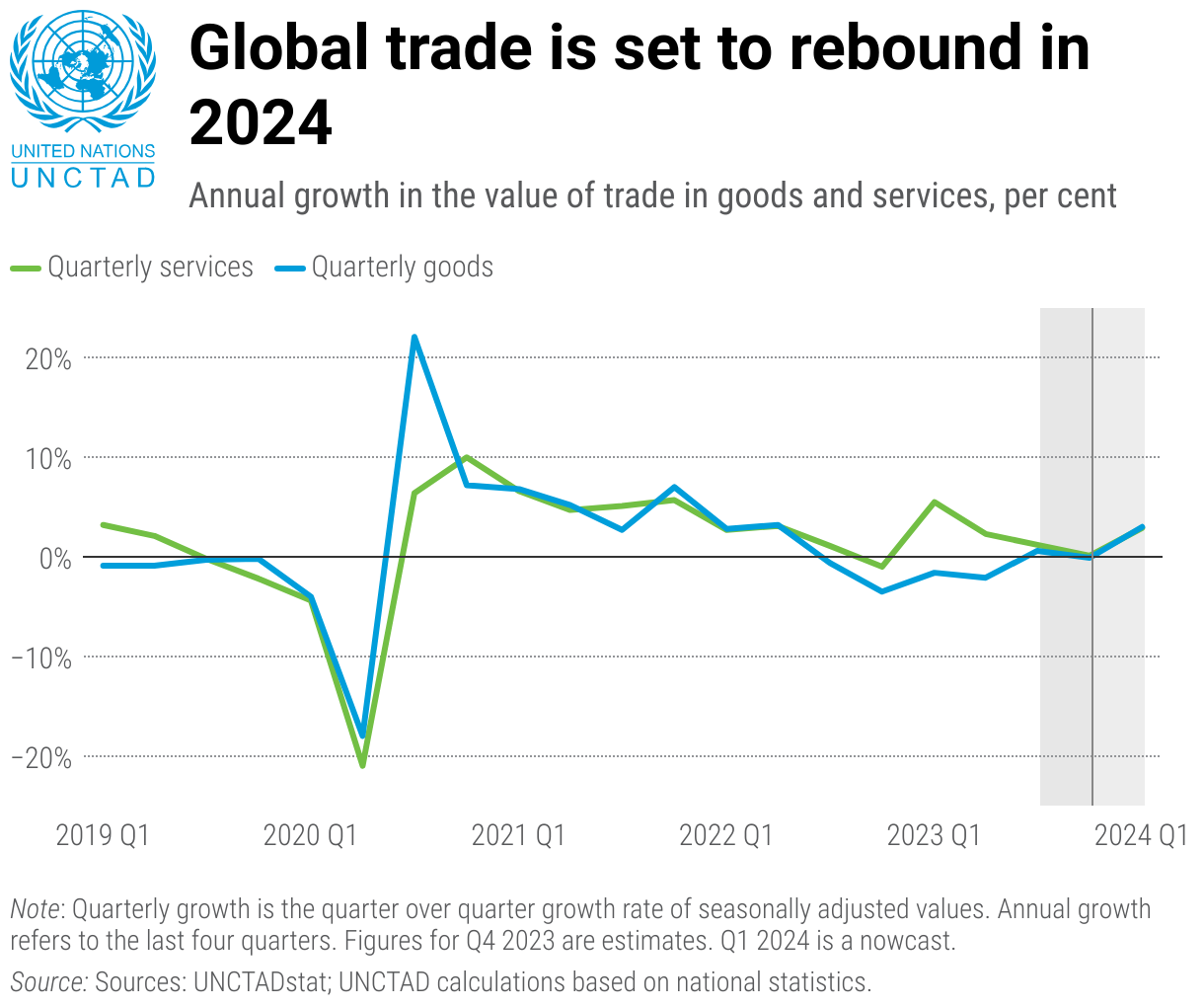

International trade is expected to rebound in 2024 after experiencing declines for several quarters.

Preliminary figures indicate a $1 trillion contraction in global trade in 2023, driven primarily by subdued demand in developed nations and weaker trade within East Asia and Latin American regions.

While trade in goods decreased during 2023, trade in services continued to grow, signalling resilience amidst challenging conditions.

After facing declines over several quarters, international trade is poised for a rebound in 2024, according to the latest Global Trade Update from the United Nations Conference on Trade and Development (UNCTAD).

In 2023, global trade saw a 3% contraction, equalling roughly $1 trillion, compared to the record high of $32 trillion in 2022. Despite this decline, the services sector showed resilience with a $500 billion, or 8%, increase from the previous year, while trade in goods experienced a $1.3 trillion, or 5%, decline compared to 2022.

The fourth quarter of 2023 marked a departure from previous quarters, with both merchandise and services trade stabilizing quarter-over-quarter. Developing countries, especially those in the African, East Asian and South Asian regions, experienced growth in trade during this period.

Regional dynamics

While major economies generally saw a decline in merchandise trade throughout 2023, certain exceptions emerged, like the Russian Federation, which exhibited notable volatility in trade statistics. Towards the end of 2023, trade in goods saw growth in several major economies, including China (+5% imports) and India (+5% exports), although it declined for the Russian Federation and the European Union.

During 2023, trade performance diverged between developing and developed countries, with the former experiencing a decline of approximately 4% and the latter around 6%. South-South trade, or trade between developing economies, saw a steeper decline of about 7%. However, these trends reversed in the last quarter of 2023, with developing countries and South-South trade resuming growth while trade in developed countries remained stable.

Geopolitical tensions continued to impact bilateral trade flows, as shown by the Russian Federation reducing its trade dependence on the European Union while increasing its reliance on China. Additionally, trade interdependence between China and the United States decreased further in 2023.

Regionally, trade between African economies bucked the global trend by increasing 6% in 2023, whereas intra-regional trade in East Asia (-9%) and Latin America (-5%) lagged behind the global average.

Mixed sectoral picture

At the sectoral level, most industries experienced declines in trade value, with exceptions such as pharmaceuticals, transportation equipment (largely due to increased demand for wide-body aircraft) and motor vehicles, which grew by 14%, primarily fuelled by the demand for electric vehicles.

Conversely, sectors like apparel, chemicals and textiles saw significant declines in 2023. However, most sectors rebounded in the fourth quarter of 2023, except for apparel, where trade further contracted.

Among services, tourism and travel-related services showed the strongest rebound, increasing by almost 40%t last year.

Prospects for 2024

Available data for the first quarter of 2024 suggests a continued improvement in global trade, especially considering moderating global inflation and improving economic growth forecasts. Additionally, rising demand for environmental goods, particularly electric vehicles, is expected to bolster trade this year.

However, geopolitical tensions and supply chain disruptions persist as pivotal factors influencing bilateral trade trends and require ongoing scrutiny. Disruptions in shipping routes, particularly those related to security issues in the Red Sea and the Suez Canal, as well as adverse climate effects on water levels in the Panama Canal, carry the potential to escalate shipping costs, prolong voyage times and disrupt supply chains.