From supporting responsible production and consumption to promoting circularity and sustainable alternatives, trade must be part of the solution to plastic pollution, not part of the problem.

© Shutterstock/Fotos593 | Plastic pollution washes ashore along the Panama Canal.

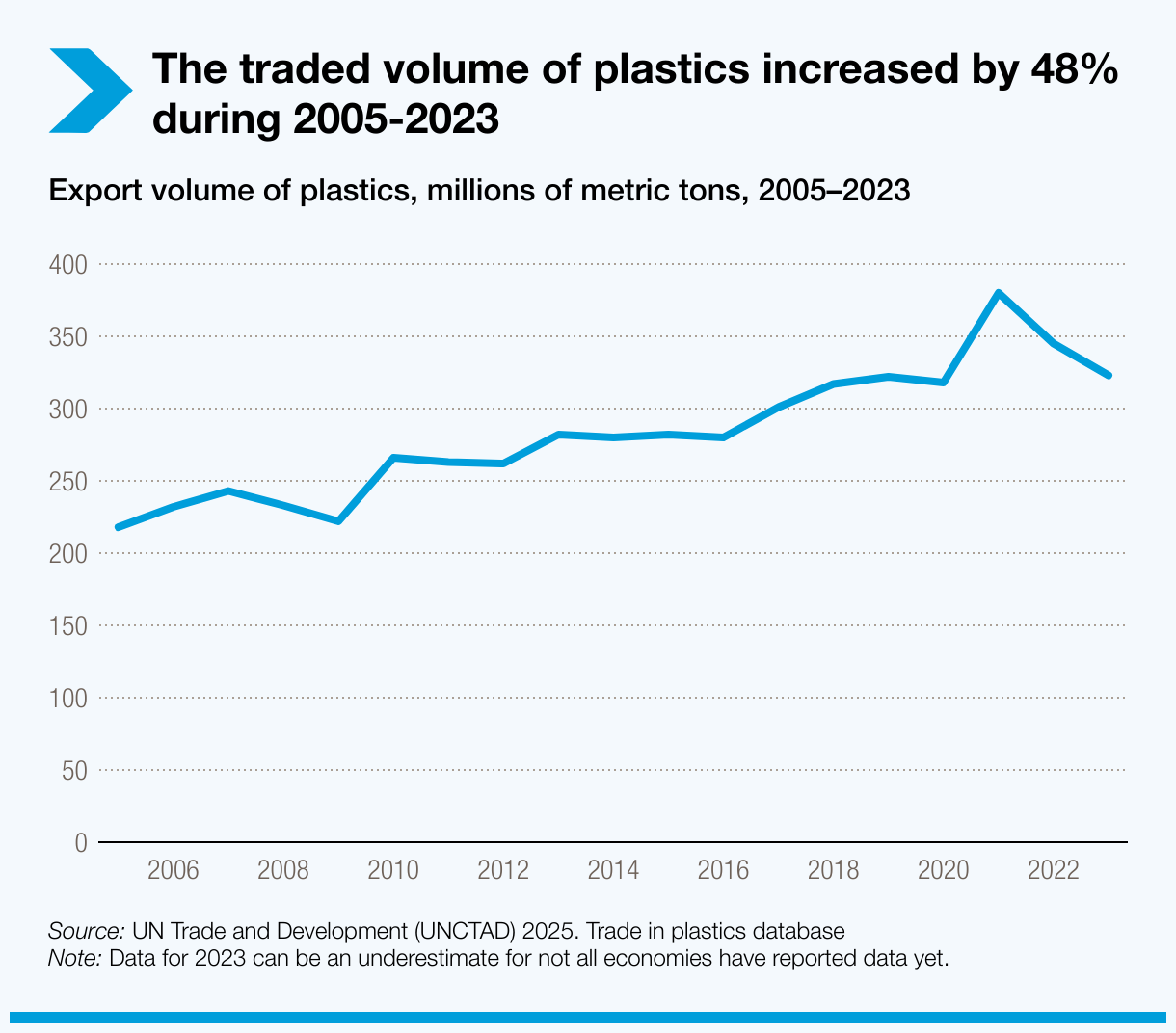

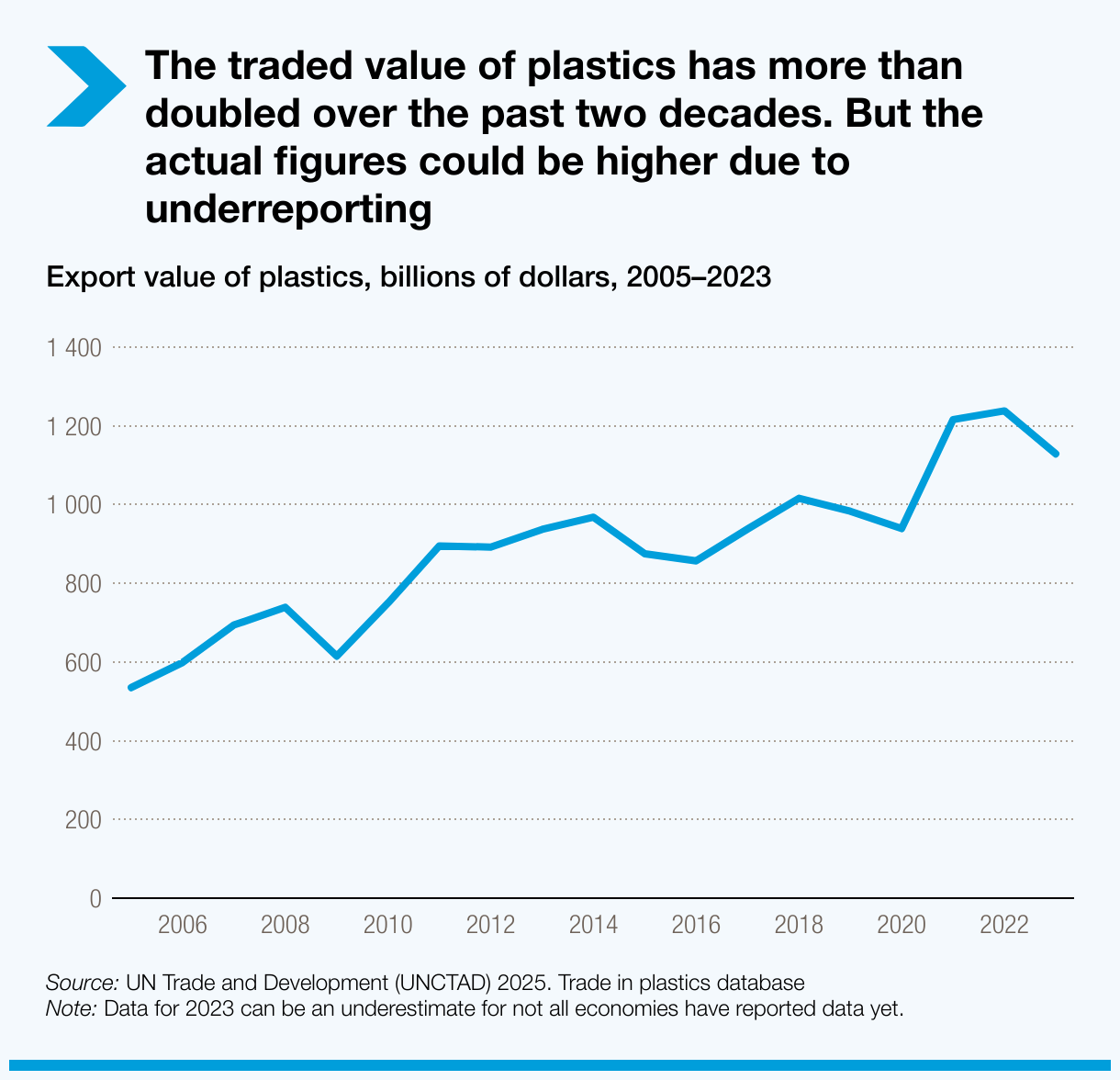

The latest Global Trade Update shows that plastic production reached 436 million metric tons worldwide in 2023, with the traded value surpassing $1.1 trillion and accounting for 5% of total merchandise trade.

Despite driving global growth across industries, plastics exact a heavy toll on environmental and planetary health.

Alarmingly, 75% of plastics ever produced have become waste and mostly ended up in the world’s oceans and ecosystems.

Such pollution also threatens food systems and human well-being, especially in small island and coastal developing countries with limited capacity to cope.

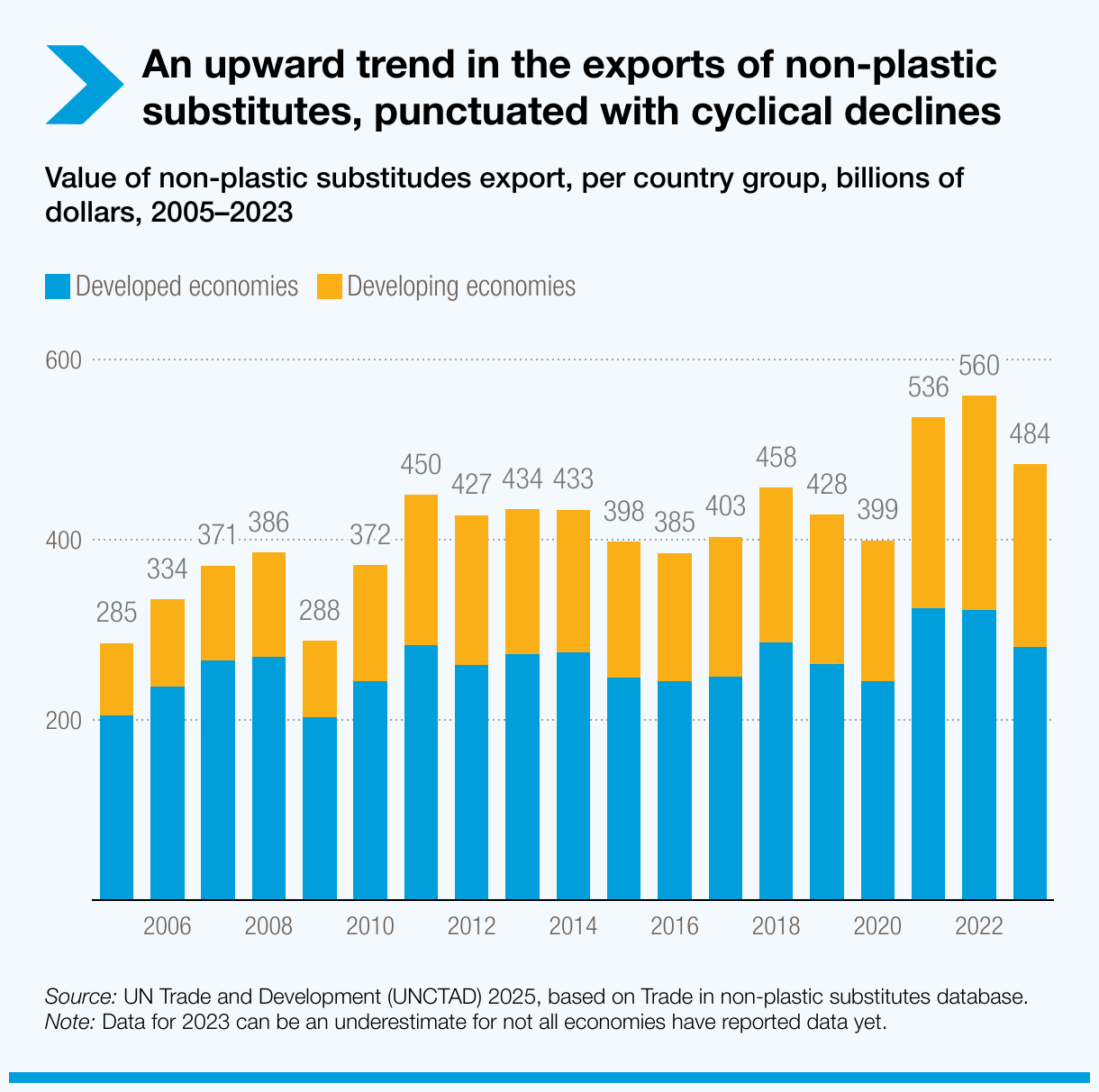

Non-plastic substitutes gaining traction but remain largely untapped

Also in 2023, global trade in non-plastic substitutes reached $485 billion, with an annual growth of 5.6% in developing economies.

These material substitutes can be recycled or turned into compost, often deriving from natural sources such as minerals, plants or animals.

But to scale up these options, the world needs to address a myriad of challenges related to tariff and non-tariff measures, limited market access and weak regulatory incentives.

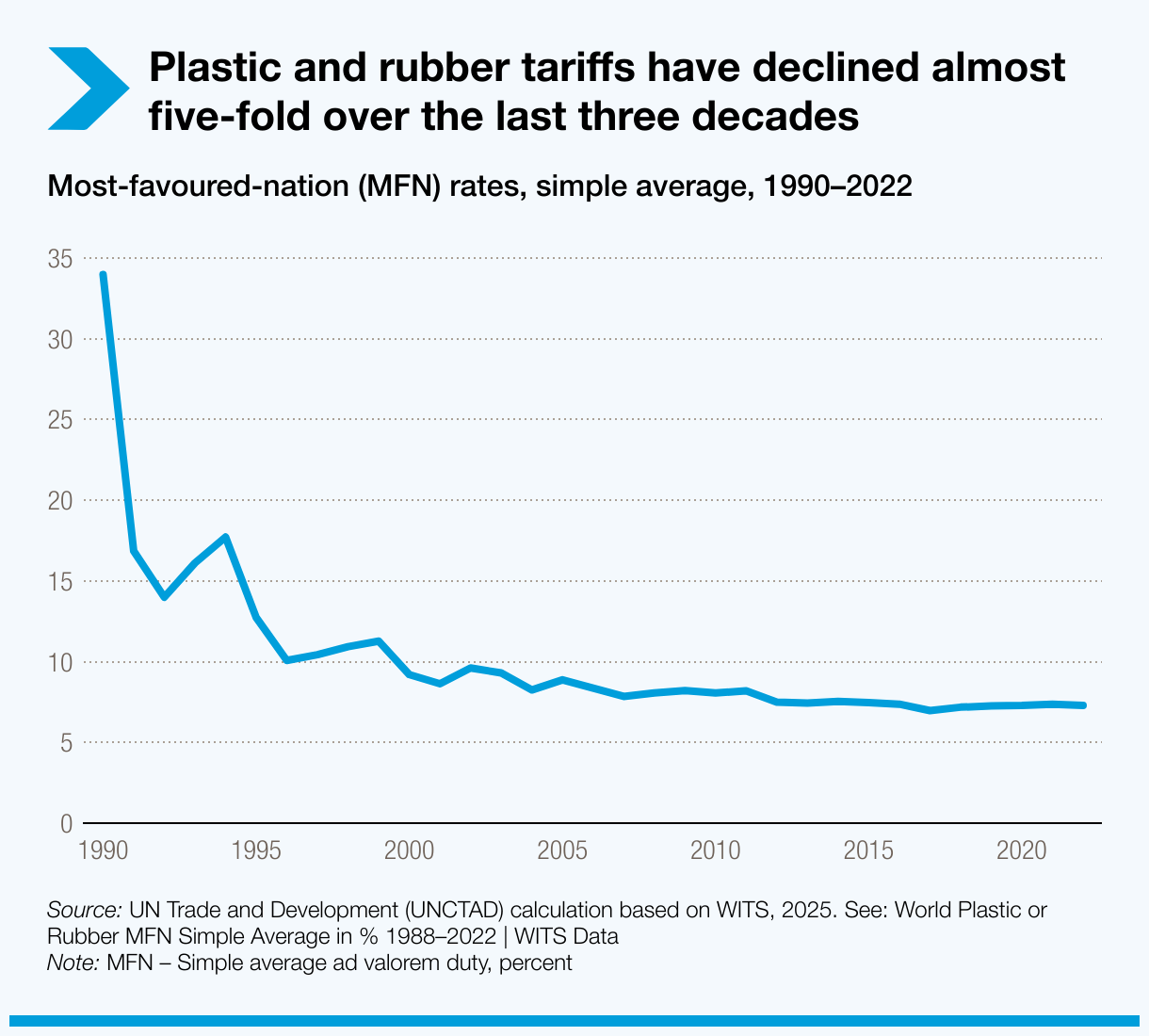

Tariffs make plastics cheaper while discouraging natural substitutes

Over the past three decades, the average most-favoured-nation (MFN) tariffs on plastic and rubber products have dropped from 34% to 7.2%, in part making fossil fuel-based plastics much less expensive.

In contrast, MFN tariffs average at 14.4% for non-plastic substitutes such as bamboo, natural fibres and seaweed.

The disparities risk hampering investment in alternative products, undermining innovation in developing countries and slowing the transition away from fossil fuel-based plastics, UN Trade and Development (UNCTAD) warns.

Regulatory fragmentation hinders effective response

With 98% of plastics derived from fossil fuels, emissions and environmental damage, if left unchecked, could continue worsening.

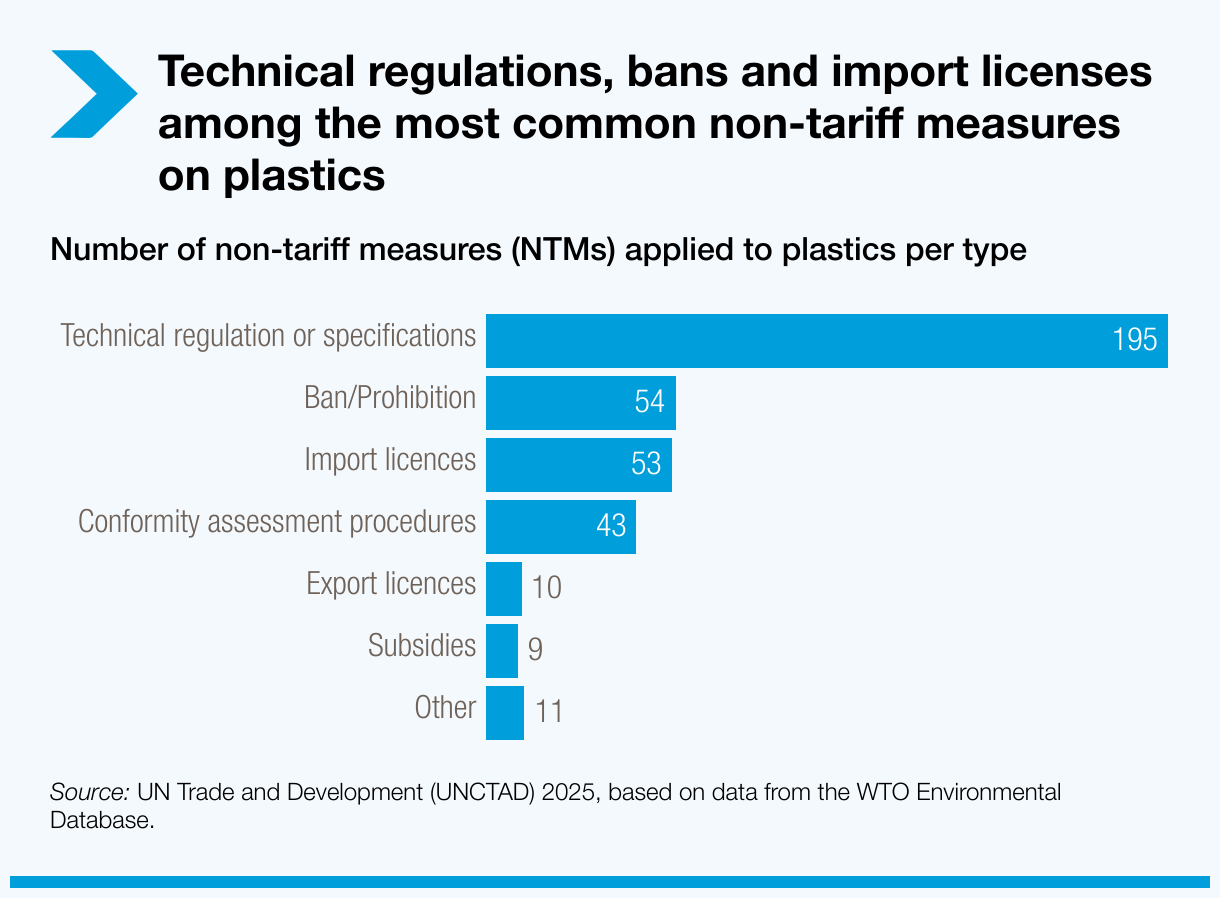

In response, many countries use non-tariff measures (NTMs) to restrict the flow of harmful plastics through bans, labeling requirements and product standards.

But existing regulations differ in requirements, sometimes even inconsistent, leading to a fragmented landscape and higher compliance costs.

Small businesses and low-income exporters particularly struggle in this regard, limiting their ability to participate in, and benefit from, sustainable trade.

Long-awaited global treaty nearing the finish line

The global push to end plastic pollution by 2040 is gaining fresh momentum.

On 5-14 August, countries are set to convene in Geneva for the final round of UN-led negotiations – known as INC-5.2 – aimed at developing a legally binding international instrument against plastic pollution.

The treaty would encompass the entire lifecycle of plastics – production, consumption and waste – within a fair and comprehensive framework.

It also presents a critical opportunity to integrate trade, finance and digital systems into a coherent global response.

Ahead of the high-stakes negotiations, UN Trade and Development underlines that a successful treaty needs to include:

- Tariff and NTM reforms to support sustainable substitutes

- Investment in waste management and circular infrastructure

- Digital tools for traceability and customs compliance

- Policy coherence across agreements reached through the World Trade Organization, the United Nations Framework Convention on Climate Change, the Basel Convention and related regional frameworks.