For most developing economies, integration into global financial markets has up to now had only weak linkages to their long-term development goals, the UNCTAD Trade and Development Report, 20151 says. Coupled with increasingly large and volatile capital flows that have expanded vulnerabilities to external shocks, the effectiveness of the policy tools designed to manage growth and development is also being limited.

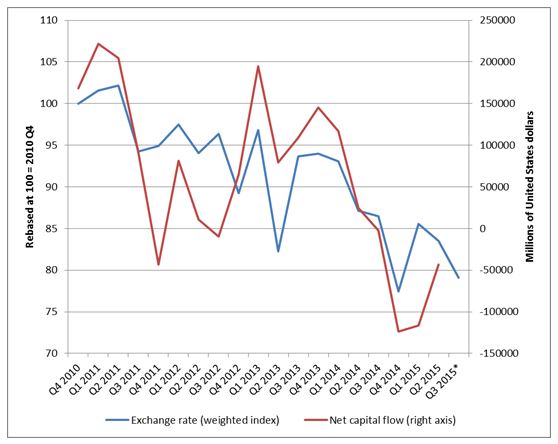

Since the early 2000s, private capital inflows to developing and transition economies have accelerated substantially. External inflows to these countries, as a proportion of gross national income, increased from 2.8 per cent in 2002 to 5 per cent in 2013, after reaching two historical records of 6.6 per cent in 2007 and 6.2 per cent in 2010. Worries of a sudden or substantial exit of inflows began with the economic slowdown and have become more pronounced with the increased volatility of recent months. The close ties between capital flows and key economic prices also increase the danger of a downward deflationary spiral (see figure).

Particularly after the crisis of 2008, those capital flows owed as much to policy decisions in advanced economies as to improved fundamentals in recipient countries. Prior to the crisis, borrowing and asset appreciation drove consumption booms and private investment bubbles in some major economies, and net exports in others. After the inevitable collapse that followed, developed country policies of quantitative easing, together with fiscal austerity, have largely continued this pattern of generating excess liquidity in the private sector.

In mid-2015, global financial markets were spooked by recessions in Brazil, the Russian Federation and South Africa and by signs of economic weakening in China. Global investors, already anticipating a hike in interest rates in the United States of America and a continuing fall in commodity prices, moved briskly to exit emerging economy equity and bond markets.

“Managing the persistent volatility of financial short-term flows requires an internationally coordinated policy response,” UNCTAD Secretary-General Mukhisa Kituyi said, not merely a financial correction with few serious consequences for the real economy. “With developing countries contributing over 60 per cent of global growth since 2011, the knock-on effects of recent emerging market difficulties could be widely felt.”

Overall, developing country growth is forecast to decline to around 4 per cent in 2015, continuing a slowdown that began in 2011 after what initially seemed to be a robust recovery from the crisis in 2008/09, when annual growth reached 7.8 per cent in 2010. That forecast, though, hangs on robust growth in the Asia region; downside risks could push the figures sharply lower in the final quarter of 2015.

For much of the last decade, many developing countries experienced strong growth and improving current accounts, accumulating considerable external reserve assets as a group. The promise of higher returns for investments in developing countries presented an attractive alternative to the low interest rates on offer in advanced economies for international investors.

These capital inflows, however, generated pressures for exchange rate appreciation. More open capital accounts also meant Governments had to conduct monetary and fiscal policy with an eye to the preferences of international finance. An estimated $2 trillion carry trade in emerging economy markets was “an accident waiting to happen”. A minor currency correction by Chinese authorities seems to have been the straw that broke the camel’s back.

Trade growth is also stalling, with the slowdown in most developing regions in 2014 expected to continue or accelerate this year. Commodity prices fell significantly during 2014 and the first half of 2015, extending their downward trend from peaks in 2011/12. The most dramatic fall was that of crude oil prices, but commodity groups whose demand is more closely linked to global economic activity experienced substantial decreases as well.

The resulting decline in the terms of trade for commodity exporters, coupled with increasing capital outflows, has severely weakened economic prospects for many developing countries, the report notes.

The associated depreciation in emerging market currencies does not, however, hold the promise of a recovery-inducing surge in exports. Instead, lower global prices are likely to result in more deflationary pressures than expanded trade given the ongoing weaknesses in global aggregate demand.

A monetary and fiscal policy mix aimed at better managing private capital flows, in particular those of an unstable or speculative nature, and their macroeconomic effects, would help developing countries to face the challenges and to enhance the gains made overall from integrating into global financial markets, the report argues. Measures at the national level, including the judicious use of capital controls and credit allocation policies, need to be supplemented by global measures that discourage the proliferation of speculative financial flows and provide more substantial mechanisms for credit support and shared reserve funds at the regional level. The recent financial turmoil has added urgency to adopting such measures.

Graph 1: Aggregate net capital flows and exchange rates

Note: Countries included are Brazil, China, India, Indonesia, Malaysia, Mexico, the Russian Federation, South Africa, Thailand, Turkey and Ukraine.

Abbreviation: Q, quarter.

Report: http://unctad.org/en/PublicationsLibrary/tdr2015_en.pdf

Overview: http://unctad.org/en/PublicationsLibrary/tdr2015overview_en.pdf