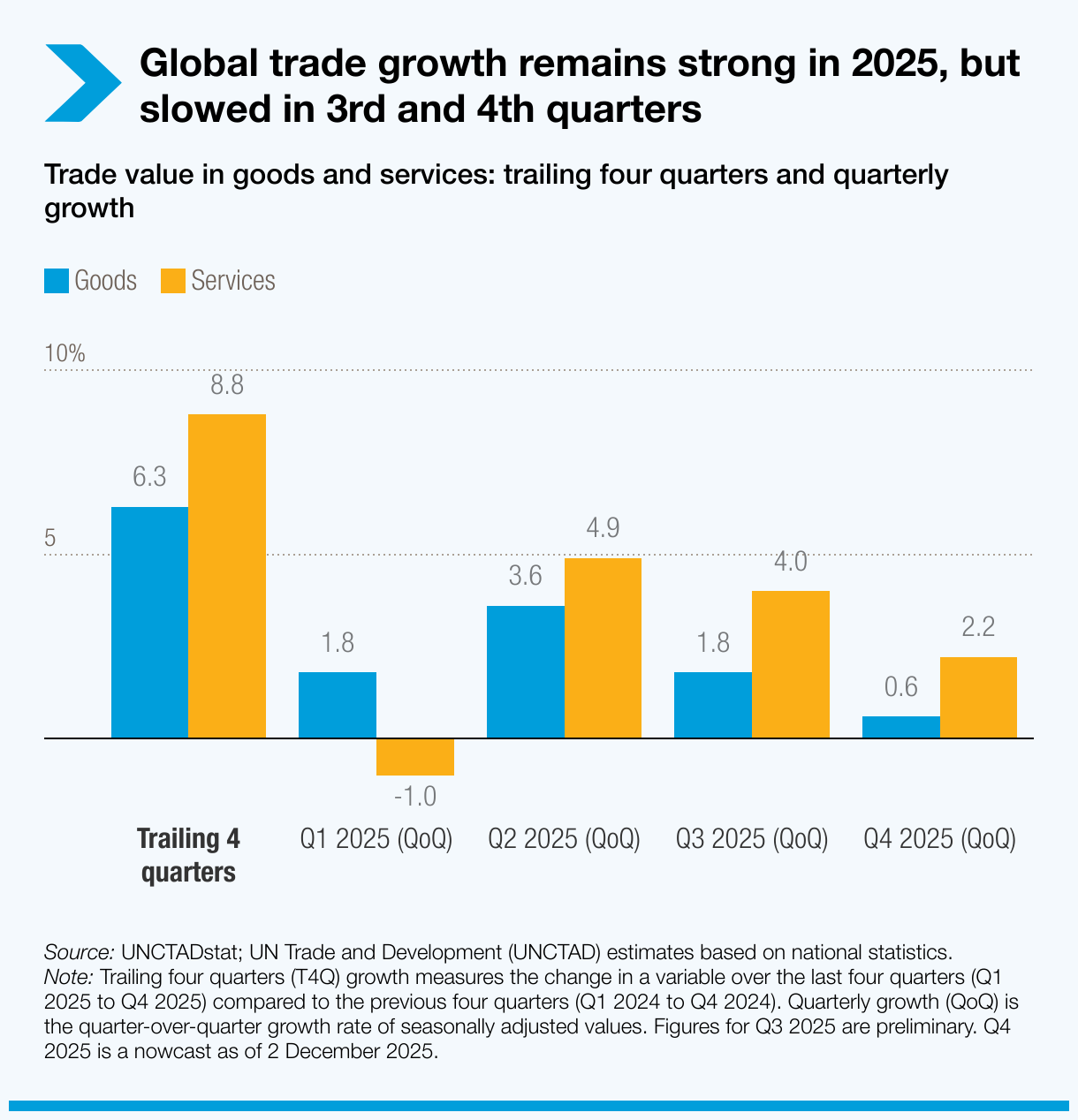

Global trade in goods and services continued to grow through the second half of 2025. If projections hold, global trade this year will exceed $35 trillion for the first time – an increase of about $2.2 trillion, or around 7%, compared with 2024.

Trade in goods will account for about $1.5 trillion of that rise, while services are set to grow by roughly $750 billion, nearly 9%.

UN Trade and Development (UNCTAD) expects growth to remain positive in the fourth quarter, though at a slower pace: 0.5% for goods and 2% for services.

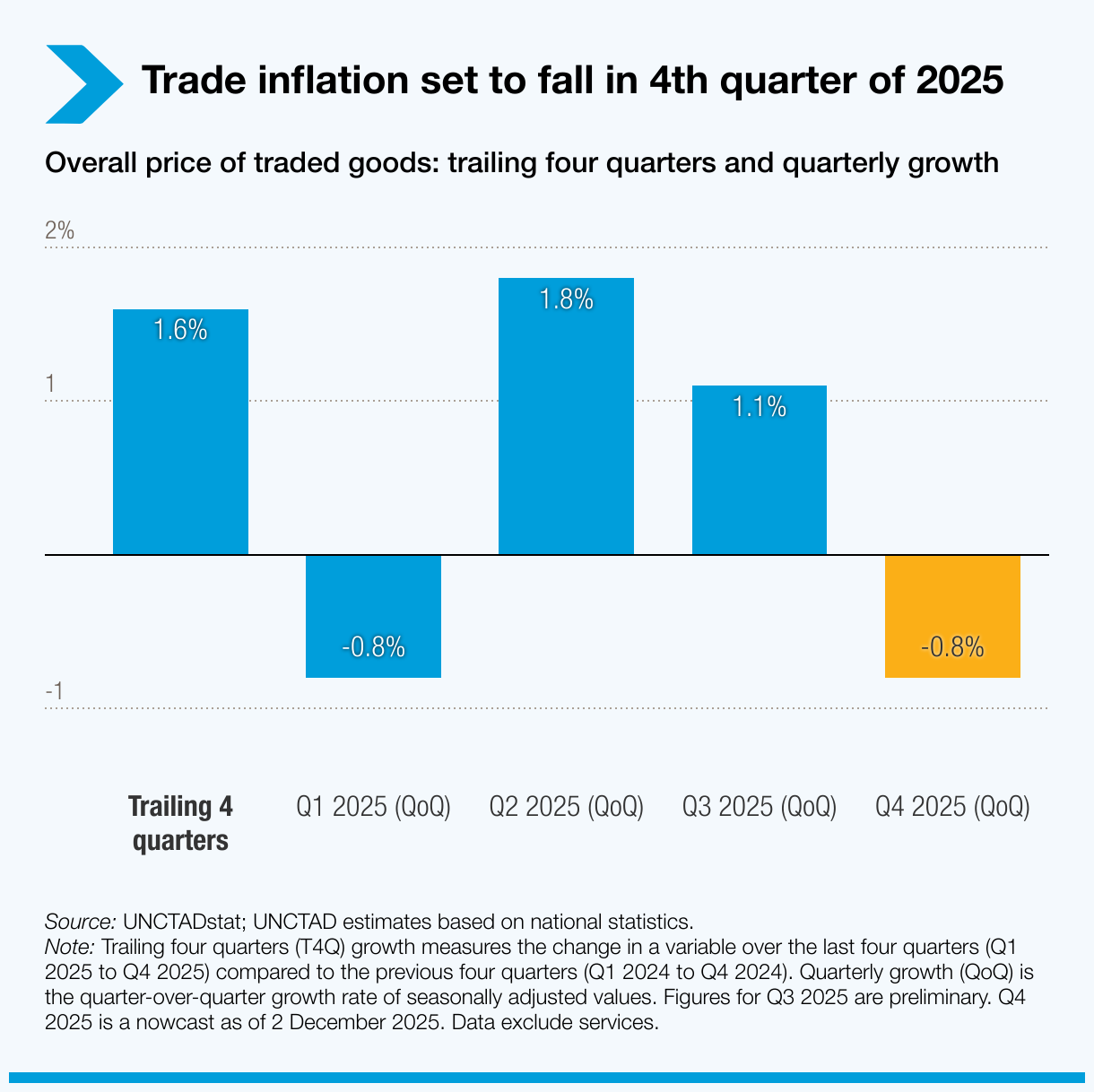

Earlier increases were partly driven by higher prices. But after rising for two consecutive quarters, the prices of trade goods are expected to decline in the fourth quarter – meaning volumes, not prices, will drive trade growth toward the end of the year.

Looking ahead, momentum is expected to weaken in 2026. Slower global growth, rising debt, higher trade costs and continued uncertainty are likely to weigh on trade flows.

Here are the key regional and sectoral trends between the fourth quarter of 2024 and the third quarter of 2025.

South–South trade outpaced the global average

- Trade between developing economies – known as South-South trade – expanded by around 8% over the last four quarters, showing growing resilience across developing regions.

- But debt pressures continue to weigh on many developing economies.

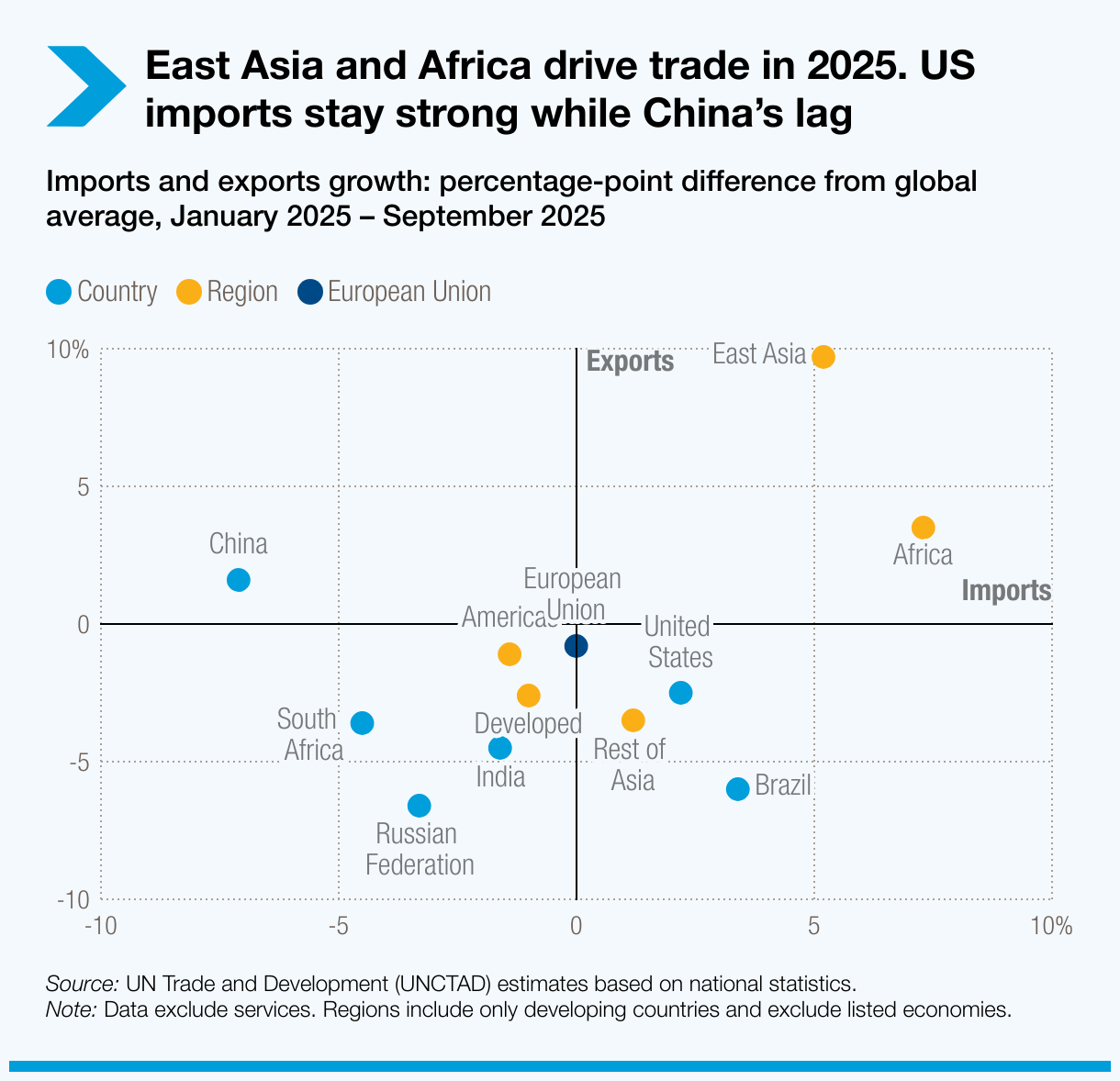

Regional trends: East Asia and Africa see the strongest growth

- East Asia’s exports recorded the strongest growth over the past four quarters (9%), with intra-regional trade growing by 10%.

- Intra-regional trade was also strong for South America, with trade within the region rising 3% in the third quarter and 7% over the last four quarters.

- Africa showed solid growth in imports – 10% over the last four quarters and 3% in the third quarter. Its exports also performed well over the past four quarters, growing at 6%.

- North America’s exports fell by 3% in the third quarter but grew 2% over the last four quarters. Imports were stronger, rising 6% over the same period.

- Europe continued to grow in the third quarter, though at a slower pace. European exports rose 2% in the quarter and 6% over the last four quarters, while imports increased by 1% in the third quarter and 8% over the same period.

Sector trends: Manufacturing remains strong, agriculture rises

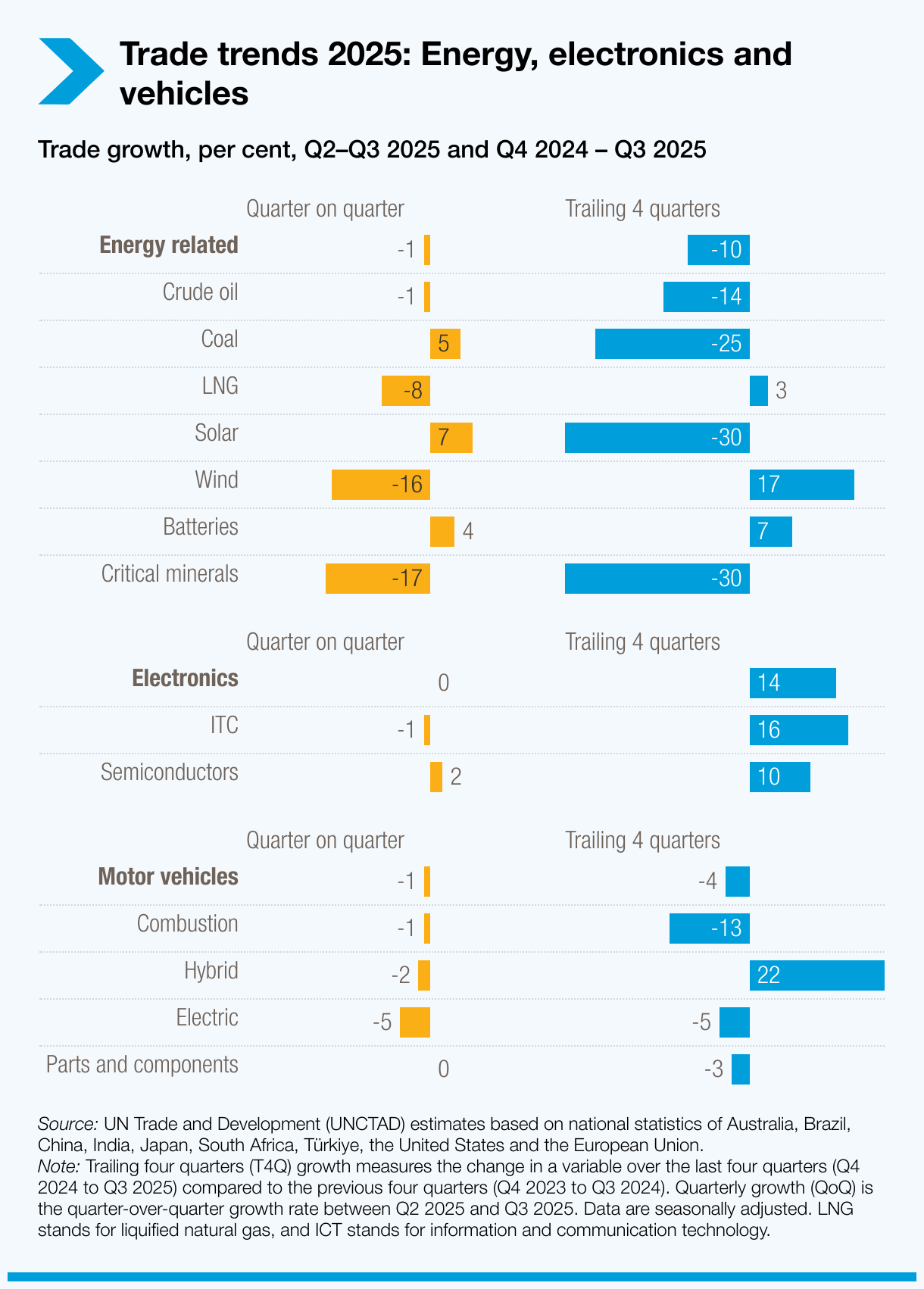

- Manufacturing remained a major engine of global trade in the third quarter, growing 3% and expanding 10% over the past four quarters. Electronics lead the way with 14% growth during the same period, supported by strong AI-related demand.

- Agriculture trade rose strongly in the third quarter (+8%), with notable gains in cereals (+11%), fruits and vegetables (+11%) and oilseeds and oils (+9%). Over the past four quarters, the overall sector grew 6%.

- The automotive sector remained weak. Trade fell 1% in the third quarter and 4% over the past four quarters. The growth in the automotive sector during the last four quarters came almost entirely from hybrid vehicles, which rose 22%, while trade in combustion-engine vehicles declined 13% and electric vehicles fell 5%.

- In commodities, iron and steel saw the sharpest increase, rising about 40% since the third quarter of 2024. But overall natural-resource trade remained subdued, weighed down by lower prices for mineral fuels.

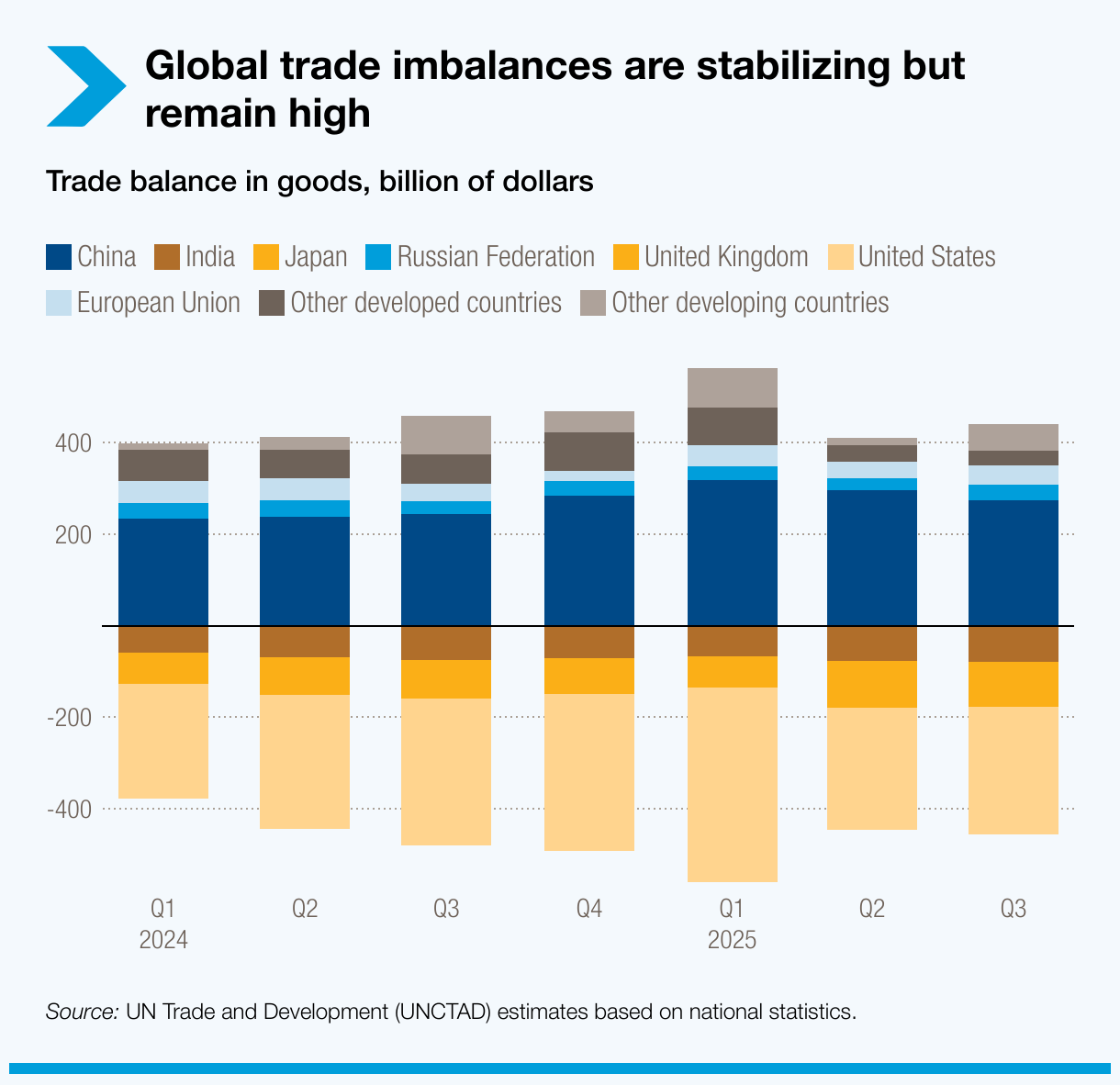

Trade imbalances remain high

- Global goods-trade imbalances are stabilizing but remain high. China’s goods surplus narrowed in the third quarter of 2025, but it was still about $30 billion higher than in the third quarter of 2024.

- The United States’ overall trade deficit also narrowed, improving compared with both the second and third quarters of 2025.

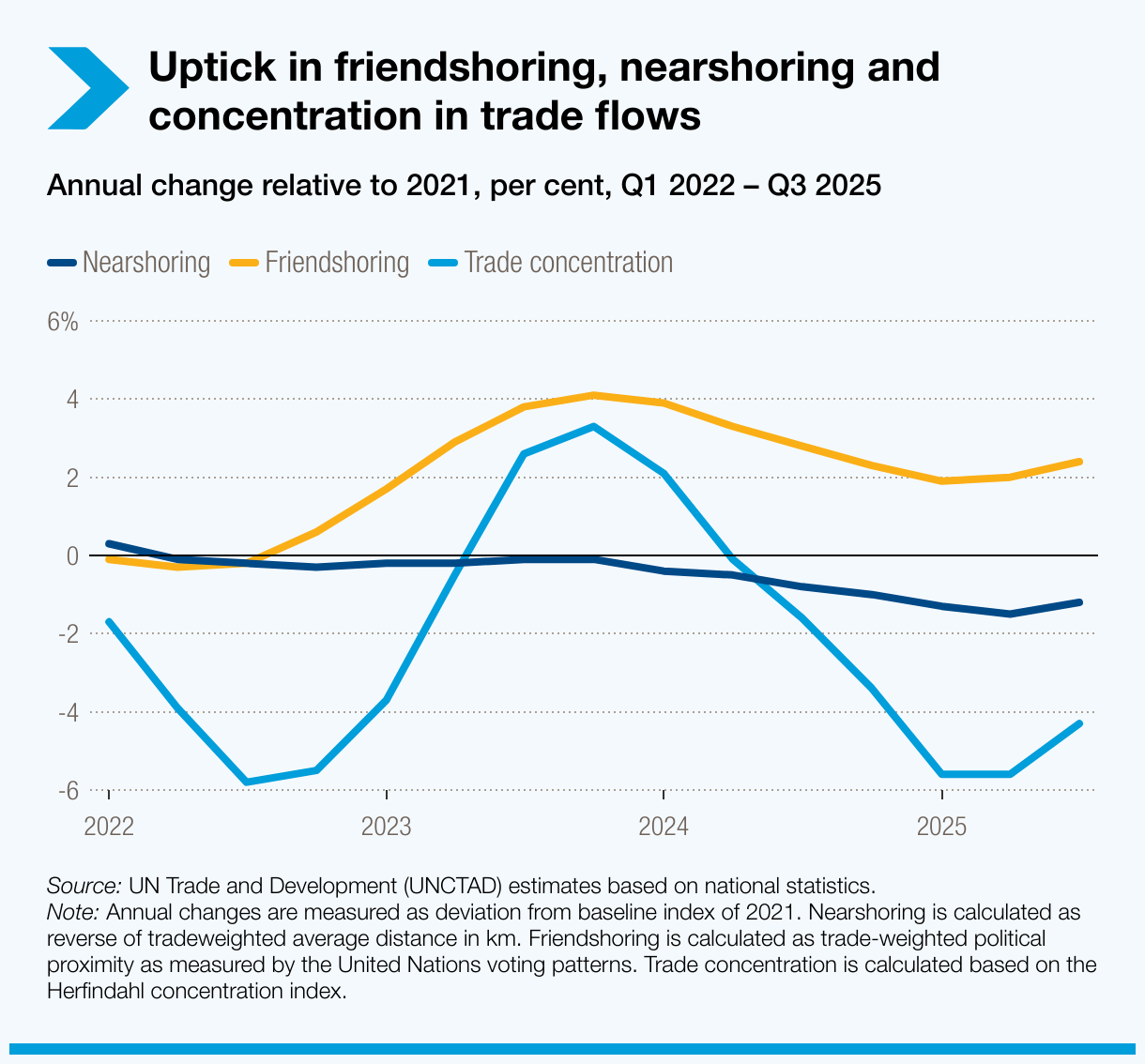

Closer geographic and political trade ties

- Friendshoring and nearshoring strengthened again in the third quarter, with both indicators rising toward their 2021 long-term averages – a reversal from the declines seen earlier in the year. Friendshoring refers to trade shifting toward politically aligned partners, while nearshoring reflects a shift toward geographically closer ones.

- Trade concentration among the largest economies also increased, signalling that a growing share of trade is flowing through a smaller group of major players.