This report provides an assessment of global economic prospects for 2025. It highlights emerging risks – especially for vulnerable economies – and outlines key policy priorities to strengthen resilience in a fragile global economy.

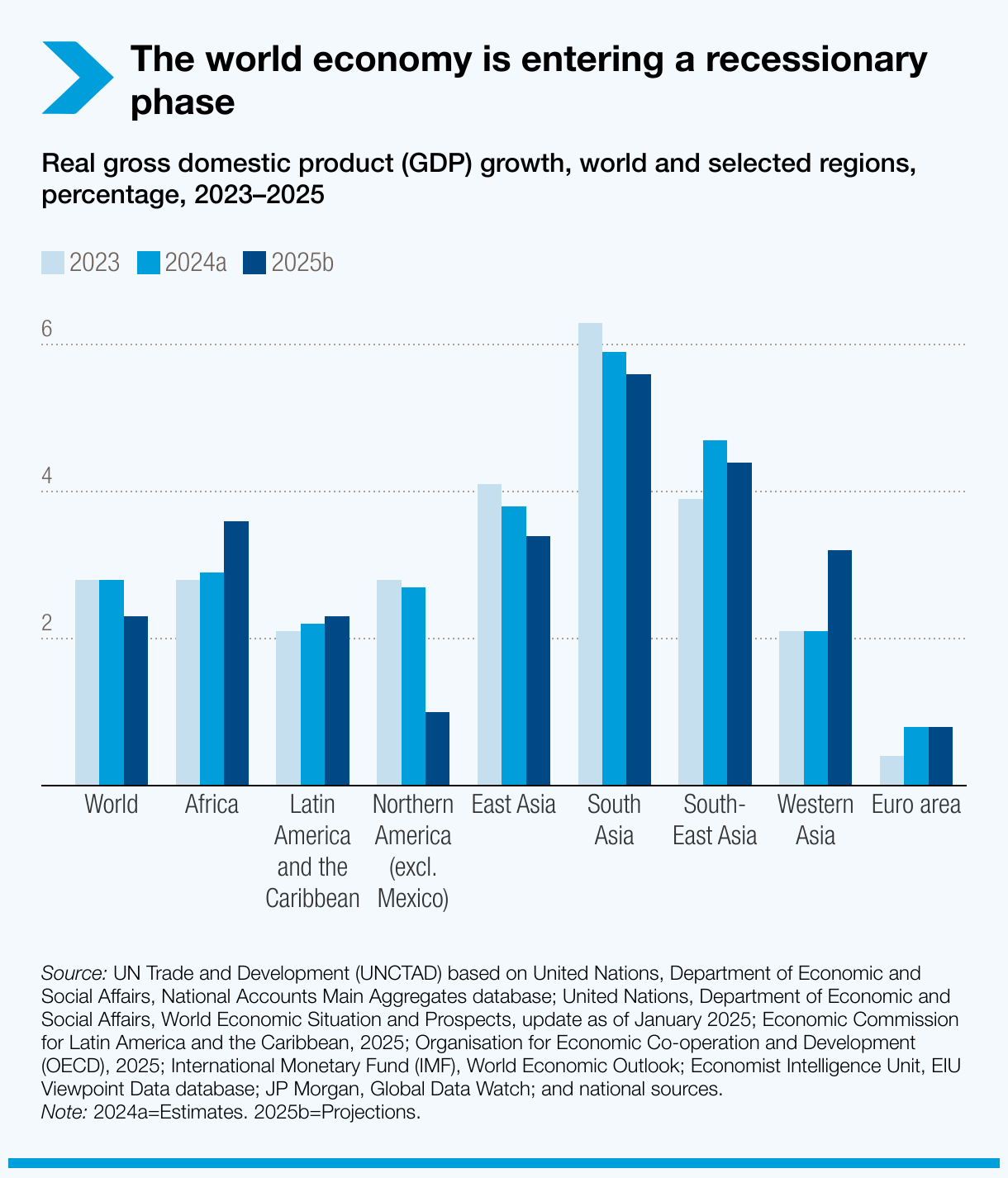

The world economy is on a recessionary trajectory

Global growth is expected to slow to 2.3% in 2025, falling below the 2.5% threshold that is often associated with a global recessionary phase. This marks a sharp deceleration compared to the average annual growth rates of the pre-pandemic period, which were already sluggish.

Subdued demand, trade policy shocks, financial turbulence and systemic uncertainty are intensifying pressures – especially for developing countries.

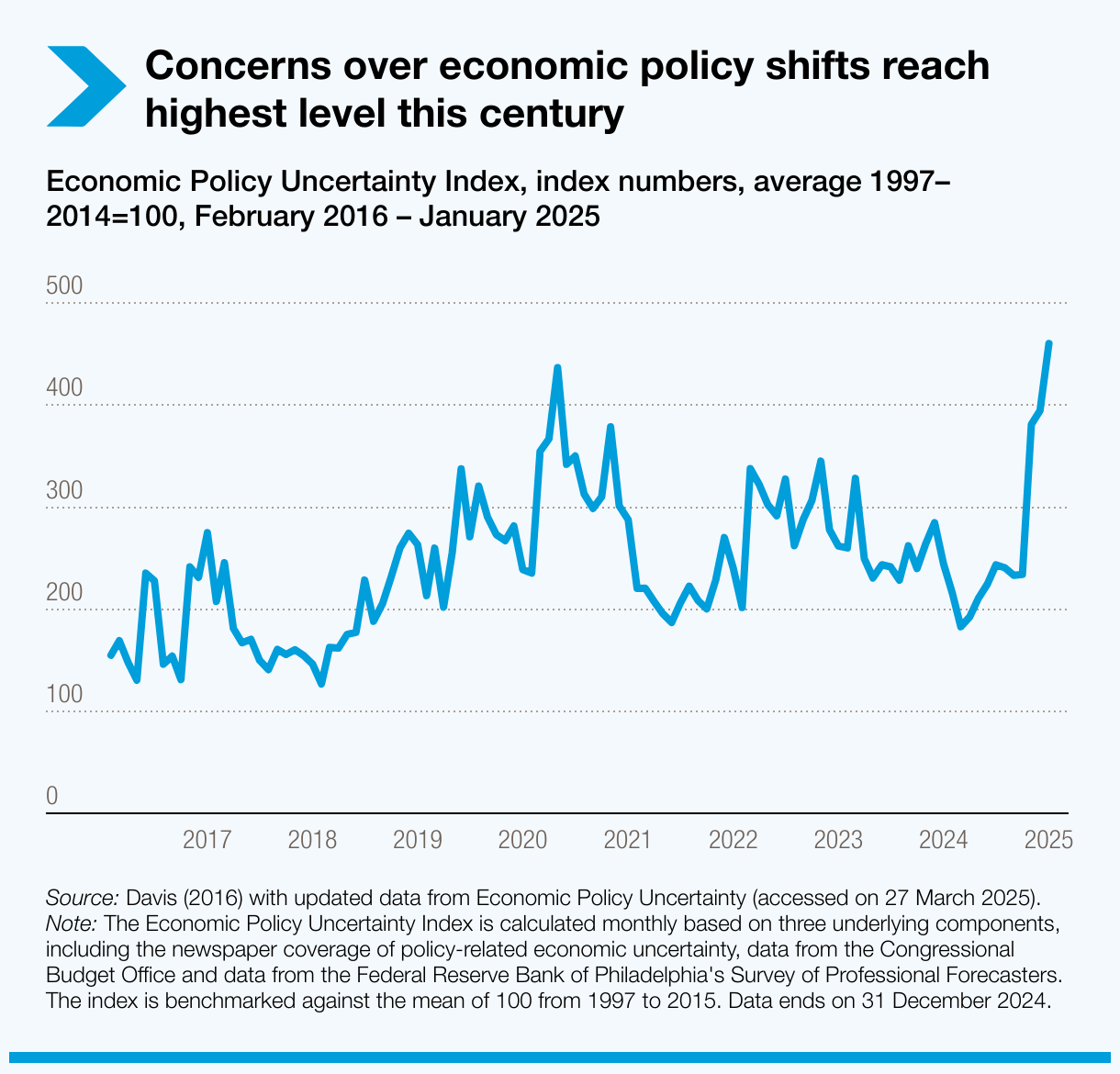

Uncertainty is driving lower growth expectations

The outlook is clouded by uncertainty. In early 2025, the Economic Policy Uncertainty Index reached its highest levels this century.

In April 2025, growing concerns over the global economic outlook and shifting trade policies triggered major financial turbulence. Markets saw sharp corrections and significant losses after weeks of volatility. The so-called financial “fear index” – a gauge of US stock market volatility – reached its third-highest level on record, behind only the peaks during the COVID-19 pandemic in 2020 and the global financial crisis of 2008.

The report warns that the ongoing geoeconomic fragmentation, if left unchecked, could deepen the downturn.

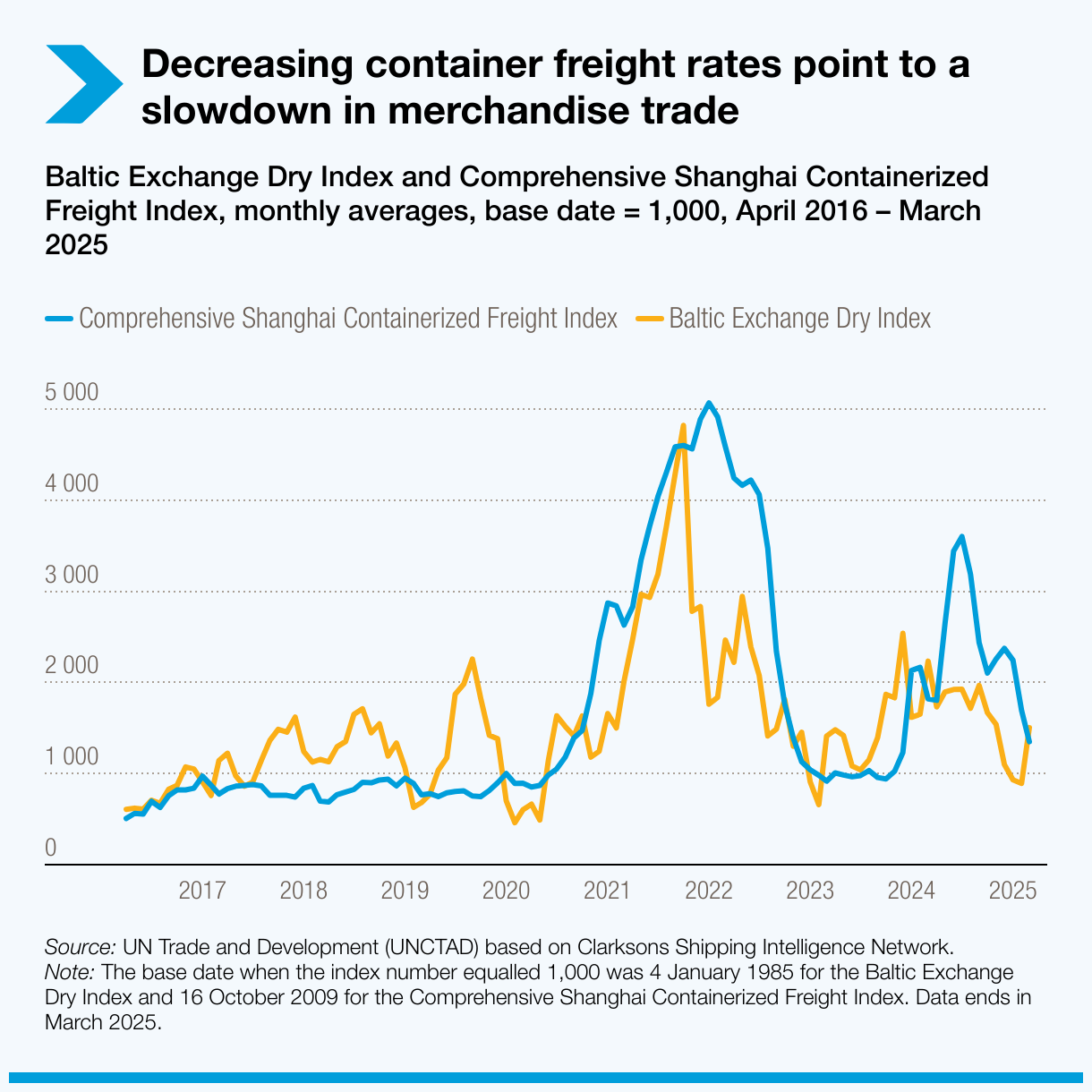

Merchandise trade dynamism is fading

The late-2024 and early-2025 uptick in global trade was driven in part by front-loaded orders ahead of newly announced tariffs. This momentum is expected to fade – or even reverse – over the year as new tariffs come into effect.

Between early January and late March 2025, the Comprehensive Shanghai Export Containerized Freight Index – a key barometer of international shipping and trade activity – fell by 40%, dropping to levels last seen in the pre-pandemic period, when global merchandise trade was already sluggish.

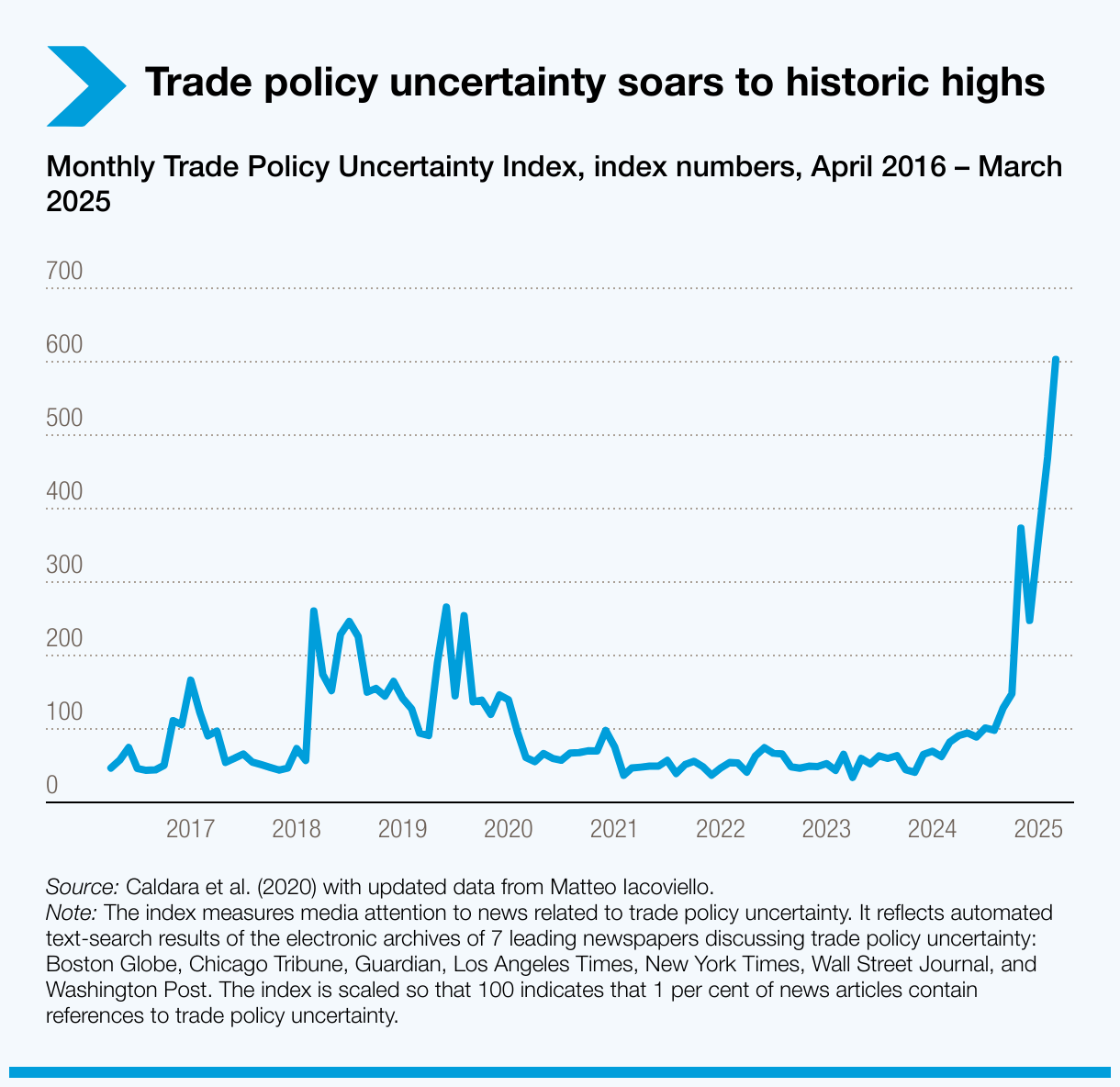

Trade policy uncertainty, now at historic highs, is weighing heavily on business confidence and long-term planning and reshaping global trade patterns. Manufacturers and investors are delaying decisions, reassessing supply chain strategies and stepping up risk management efforts.

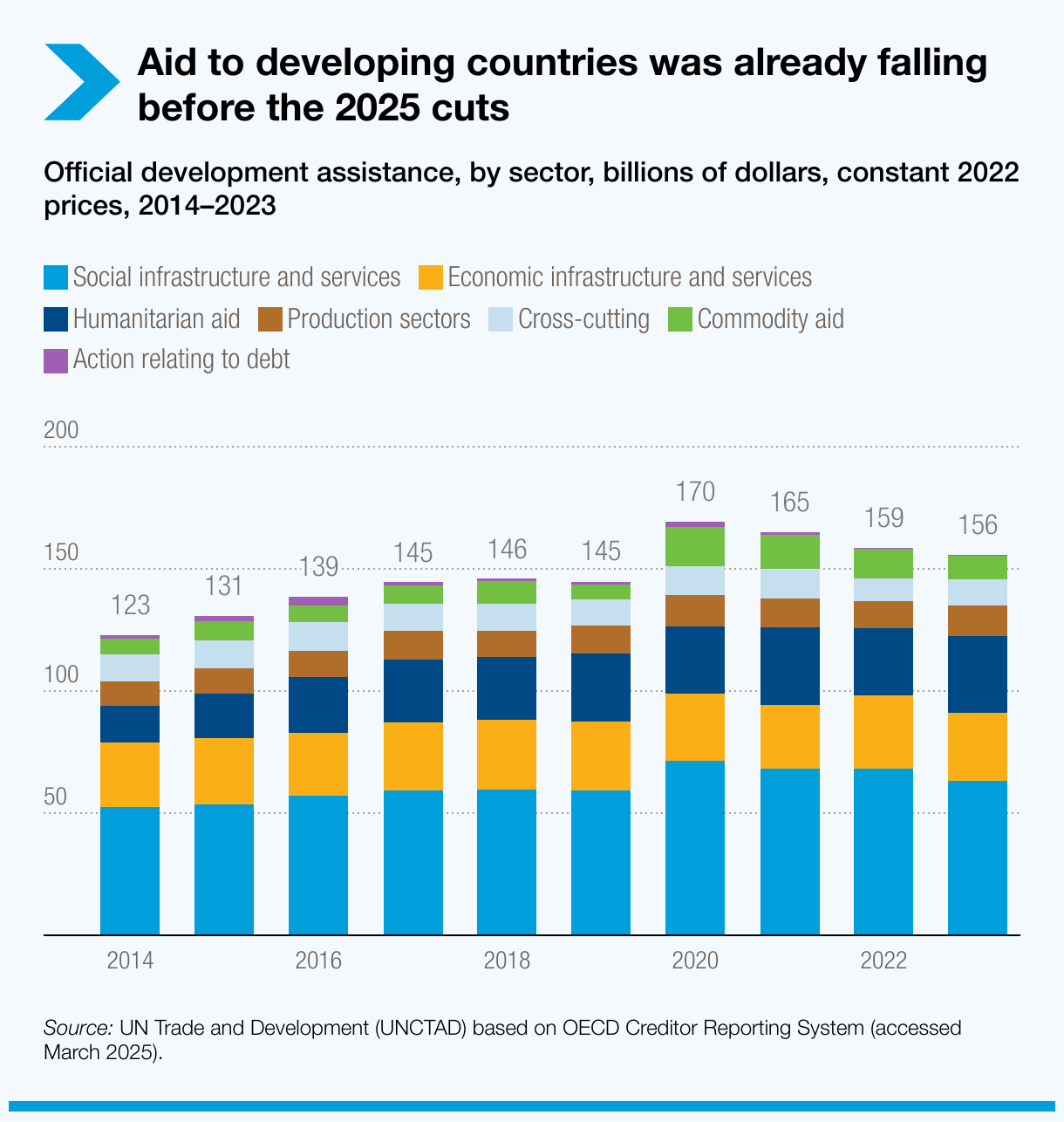

Development finance is increasingly under pressure

Fiscal priorities are shifting in major economies, with official development assistance (ODA) declining, social spending shrinking and defence budgets rising.

Preliminary estimates point to an 18% drop in ODA from major donors between 2023 and 2025. The announced cuts come on top of a broader downward trend in aid to developing countries, despite an overall increase in global ODA. Flows to developing countries fell from nearly $175 billion in 2020 to $160 billion in 2023.

The report warns that these changes risk undermining progress toward the Sustainable Development Goals. Meanwhile, investor caution – amid tight financial conditions and growing uncertainty – further threatens long-term development financing. For more on trends in ODA, see the report "Aid at the crossroads".

Developing countries face a ‘perfect storm’

Many low-income countries face a “perfect storm” of worsening external conditions, heavy debt burdens and weakening domestic growth.

More than a half of low-income countries (35 out of 68) are currently in debt distress or at high risk of debt distress. A rapid build-up of debt – especially in developing countries – combined with persistently tight financing conditions, is straining already limited fiscal space. With borrowing costs still high, governments have to increasingly divert resources from critical spending needs to cover debt-servicing costs.

Meanwhile, capital is increasingly flowing towards “safer” or more “stable” assets and markets – typically in advanced economies – to the detriment of financial flows to developing countries.

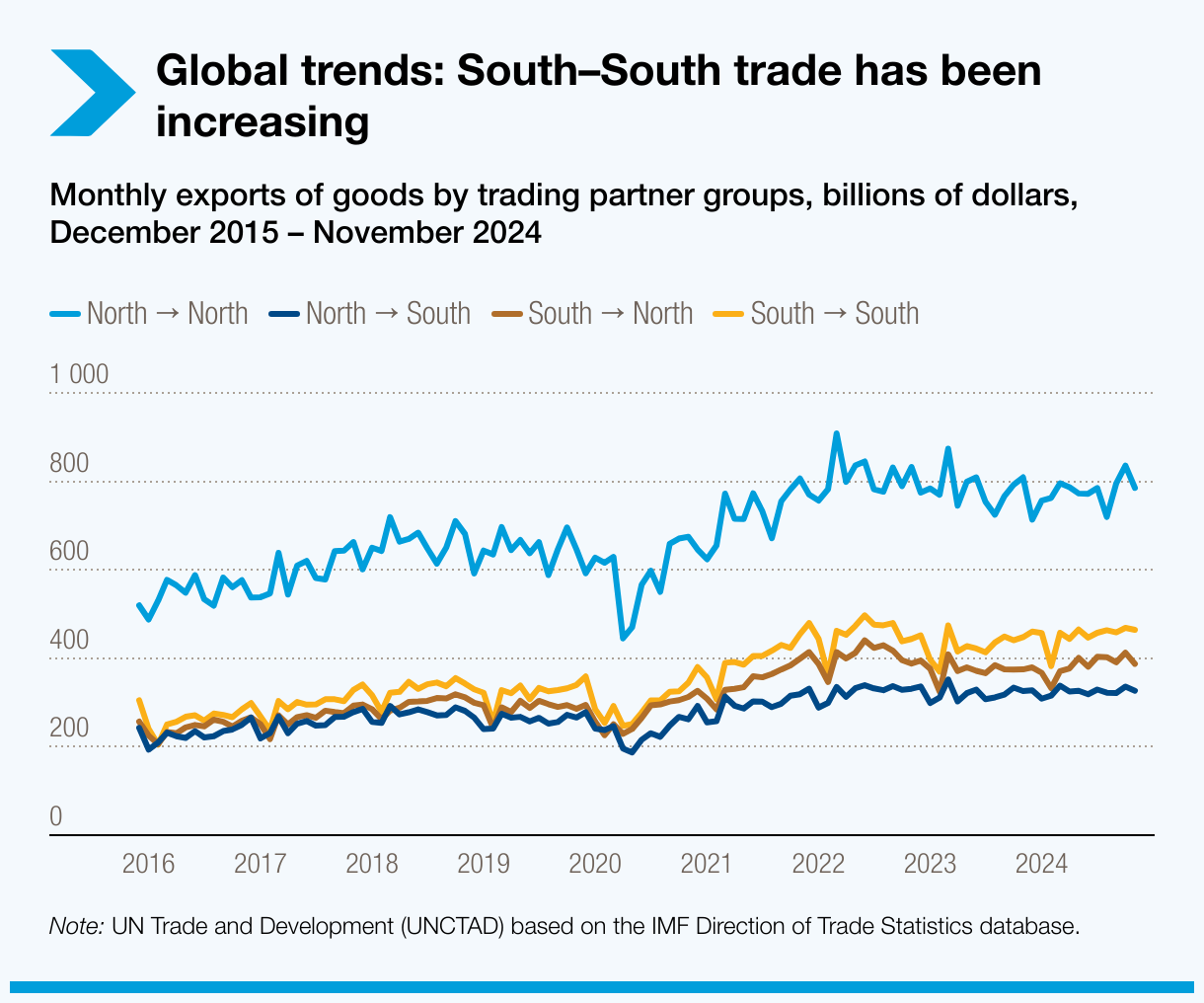

South-South trade and regional integration offer opportunities

The report, however, points to the growth of trade among developing countries (South-South trade) as a source of opportunities, resilience and a buffer against uncertainty. Already accounting for about one third of global trade, South–South trade is expanding faster than other trade flows. Intra-regional trade, particularly in East and South-East Asia, is helping drive this growth.

Policy priorities for building resilience

With trade tensions rising and global growth slowing, the report underscores the risks of economic fragmentation and geoeconomic confrontation.

The report calls for:

- Strengthening regional and international policy coordination to restore predictability in trade and financial flows.

- Enhancing multilateral cooperation to stabilize markets and protect vulnerable economies.

- Building on existing trade and economic links between developing countries as a pathway to resilience and a buffer against global shocks.

- Rebalancing of fiscal priorities, shifting away from surging military spending towards sustainable infrastructure, social protection and climate action.

- Aligning fiscal, monetary and industrial policies with long-term development goals.