Slower growth, rising protectionism and structural shifts in value chains, services and regulation are redefining trade flows, creating new risks and opportunities.

Global trade had a record year in 2025, with preliminary data pointing to a 7% increase to exceed $35 trillion for the first time. While growth is expected to remain positive in 2026, the pace will slow.

UN Trade and Development’s first trade report of the year points to a more complex and fragmented global environment. Geopolitical tensions, shifting supply chains, accelerating digital and green transitions and tighter national regulations are reshaping trade flows and global value chains.

The January Global Trade Update highlights ten trends shaping global trade in 2026 – and the policies and actions needed to help countries navigate change and seize emerging opportunities.

1. Global growth slows, weighing on developing economies

Global economic growth is projected to remain subdued at 2.6% in 2026, with developing economies excluding China slowing to 4.2%.

Major economies are also losing momentum:

- United States: growth projected to slow to 1.5%, from 1.8% in 2025.

- China: growth expected at 4.6%, down from 5%.

- Europe: Fiscal stimulus offers limited support, while demand will remain modest.

Slower growth weakens export demand, tightens financial conditions and raises exposure to shocks. Developing countries will need stronger regional trade, diversification and digital integration to build resilience.

2. Trade rule reform reaches a crossroads

The World Trade Organization’s 14th ministerial conference will take place in Yaoundé amid rising unilateral tariffs, geopolitical tensions and growing use of trade restrictions, putting pressure on multilateral trade rules.

For developing countries, priorities are clear:

- Restoring dispute settlement, particularly the Appellate Body, to ensure rules can be enforced.

- Preserving policy space, including special and differential treatment, which provides greater flexibility and time to implement trade rules.

- Advancing talks on agriculture, fisheries, digital trade and investment facilitation.

Trade–climate links will also feature prominently, with discussions on subsidies and standards affecting competitiveness. Outcomes will determine whether global trade rules adapt – or fragment further.

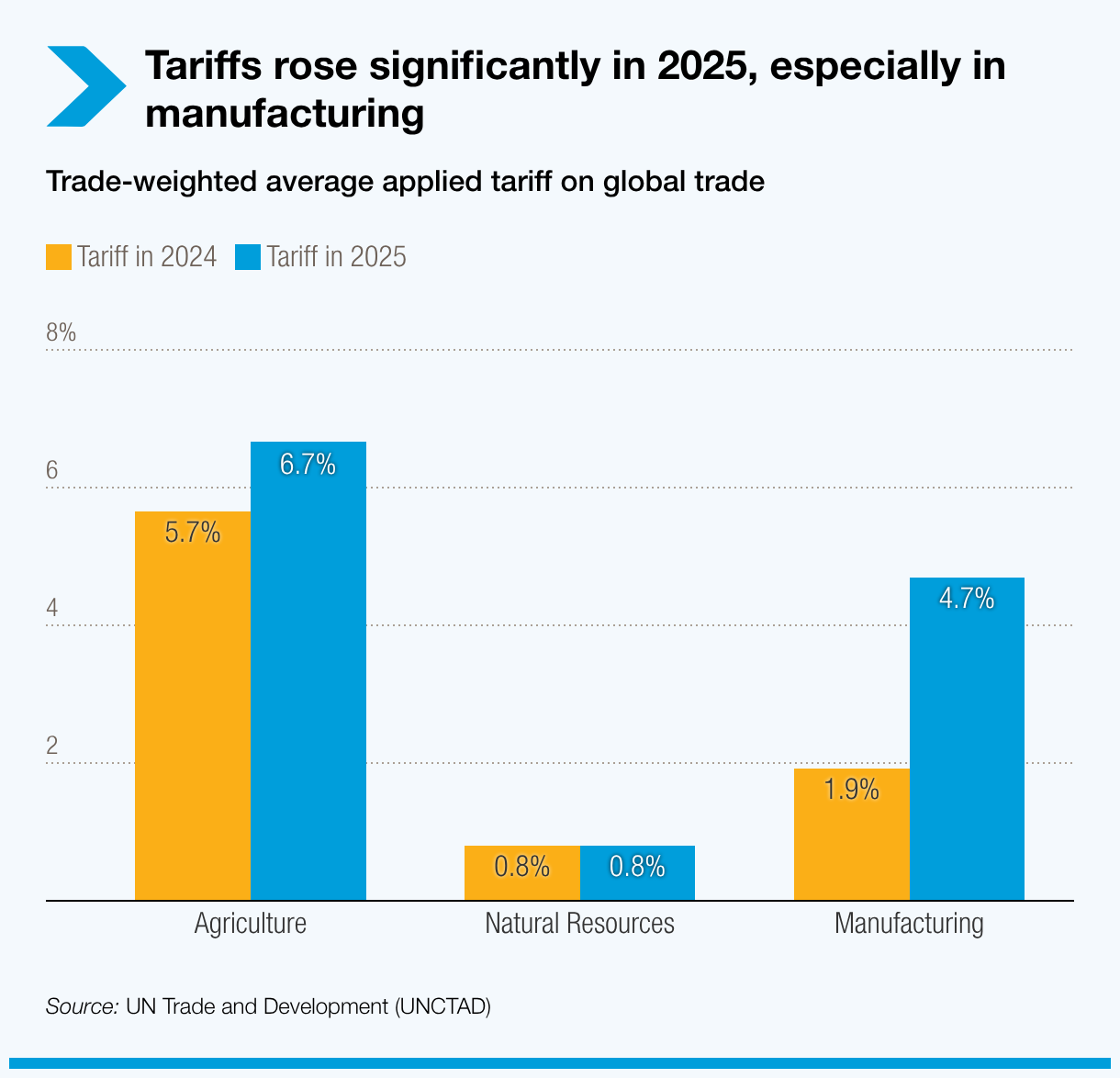

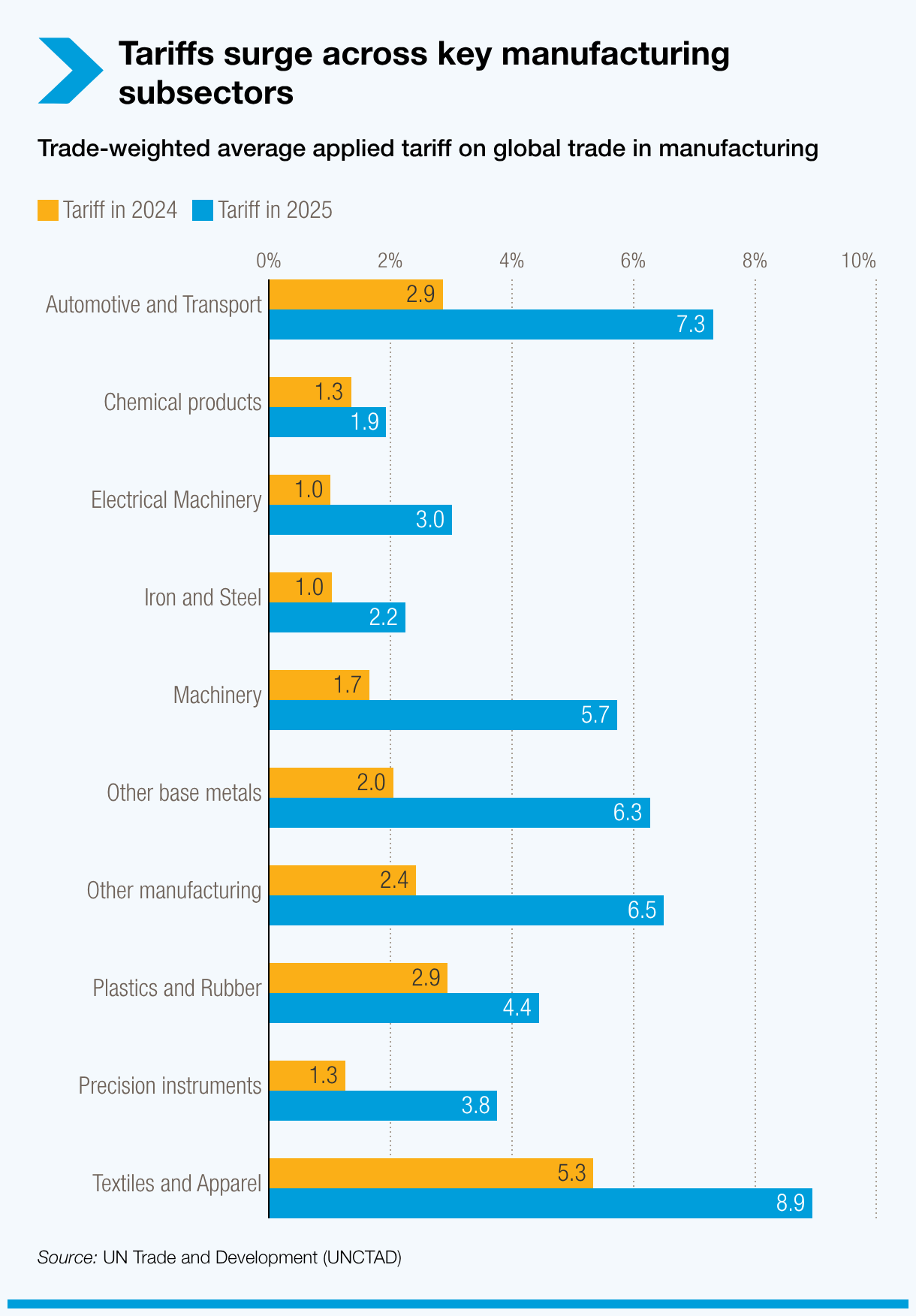

3. Rising tariffs fuel trade uncertainty

Governments are expected to continue using tariffs as protectionist and strategic tools in 2026. Their use rose sharply in 2025, especially in manufacturing, led by US measures tied to industrial and geopolitical objectives, lifting average global tariffs unevenly across sectors and trading partners.

Tariffs disrupt trade even before they take effect:

- Higher costs weaken demand and shift sourcing.

- Policy volatility discourages investment and planning.

Smaller, less diversified economies are most exposed, with limited capacity to absorb higher costs or redirect exports. Rising tariffs risk revenue losses, fiscal strain and slower development, particularly in commodity-dependent economies.

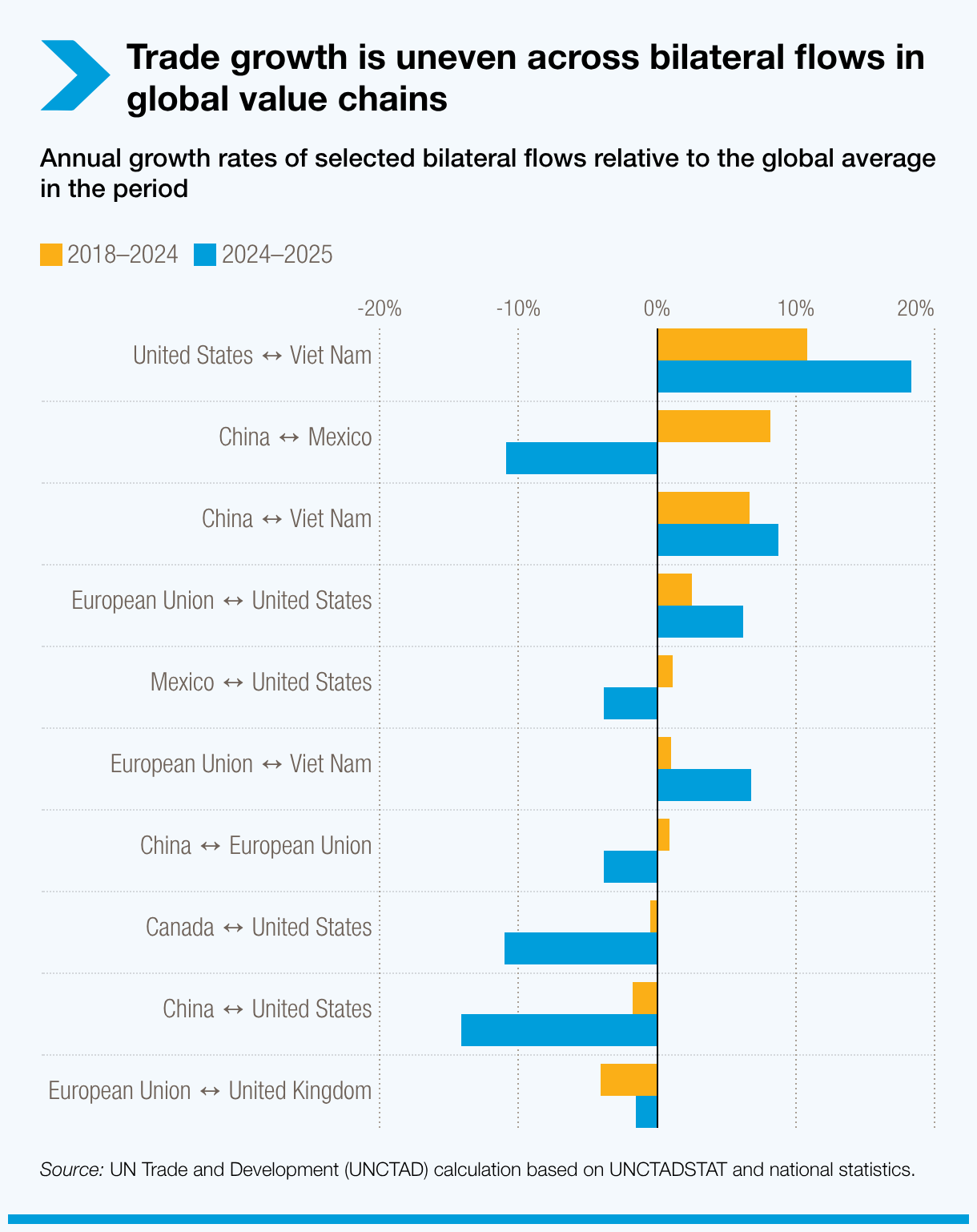

4. Value chains reconfigure as geopolitics reshape trade and investment maps

Global value chains continue to shift as firms move away from cost-driven offshoring towards risk management. Geopolitical tensions, industrial and climate policies, and technological change are driving:

- Supplier diversification.

- Production relocation closer to end markets.

- Firms controlling more of their supply chain to secure key inputs.

Nearly two thirds of global trade takes place within value chains, and their reconfiguration is creating new hubs and routes. While diversification can strengthen resilience, it may also reduce efficiency and weigh on trade growth.

For developing economies, potential outcomes diverge:

- Well-positioned countries with strong infrastructure, skills and stable policies can attract investment.

- Peripheral economies risk marginalisation unless they improve logistics, upgrade skills and strengthen the investment climate.

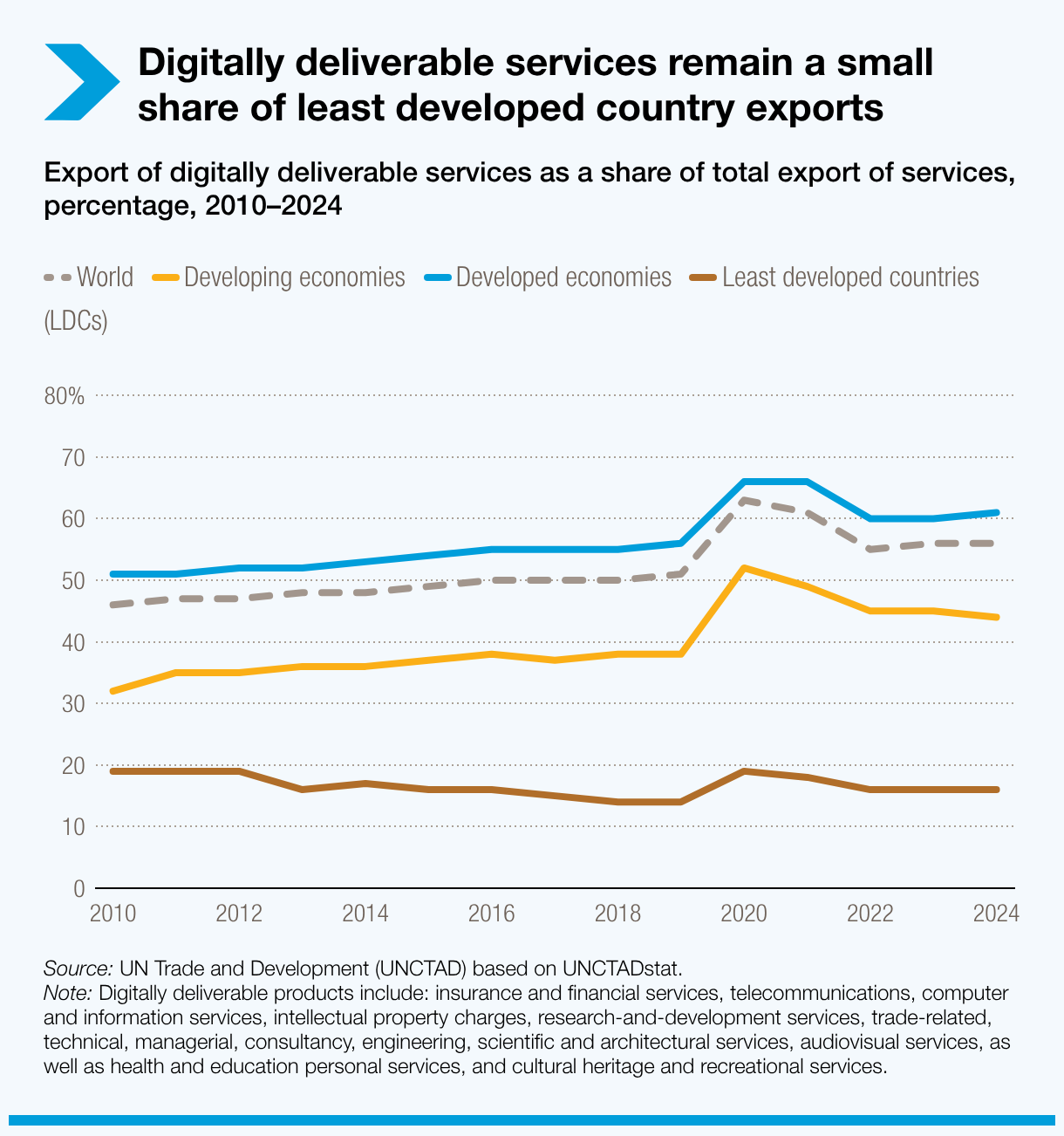

5. Services drive trade growth, widening digital gaps

Services account for 27% of global trade and grew by about 9% in 2025, far outpacing goods. They also underpin production, making up 71% of global intermediate inputs, including large shares in manufacturing.

Digitalization is accelerating this shift and widening gaps:

- Digitally deliverable services now account for 56% of global services exports.

- In developed economies, about 61% of services exports are delivered digitally.

- In least developed countries, the share is just 16%, highlighting a wide digital gap.

Meanwhile, new barriers are emerging as digital trade rules tighten. Closing the digital divide – through infrastructure, skills and supportive regulation – will be critical if developing countries are to benefit from the fastest-growing segment of global trade.

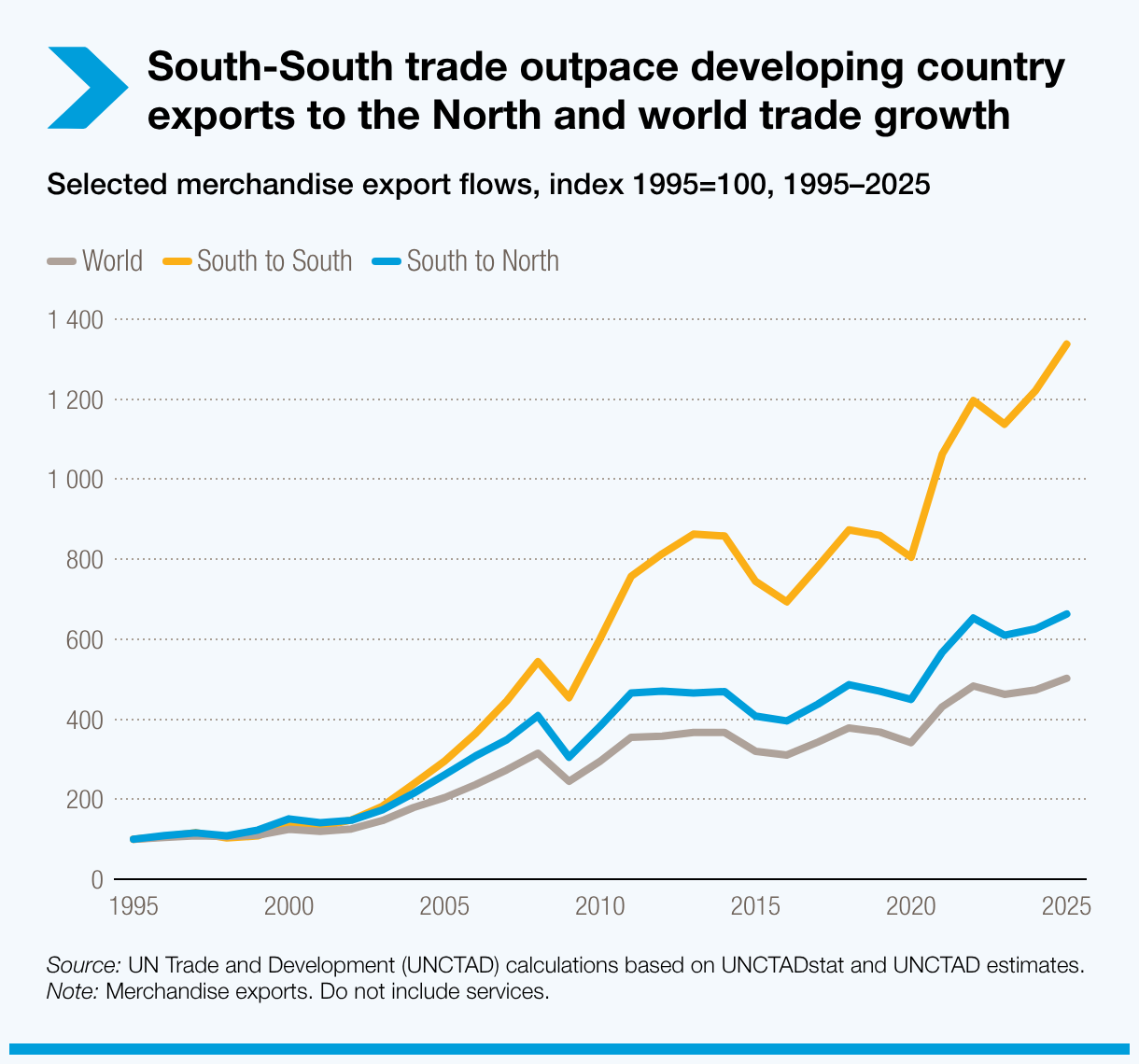

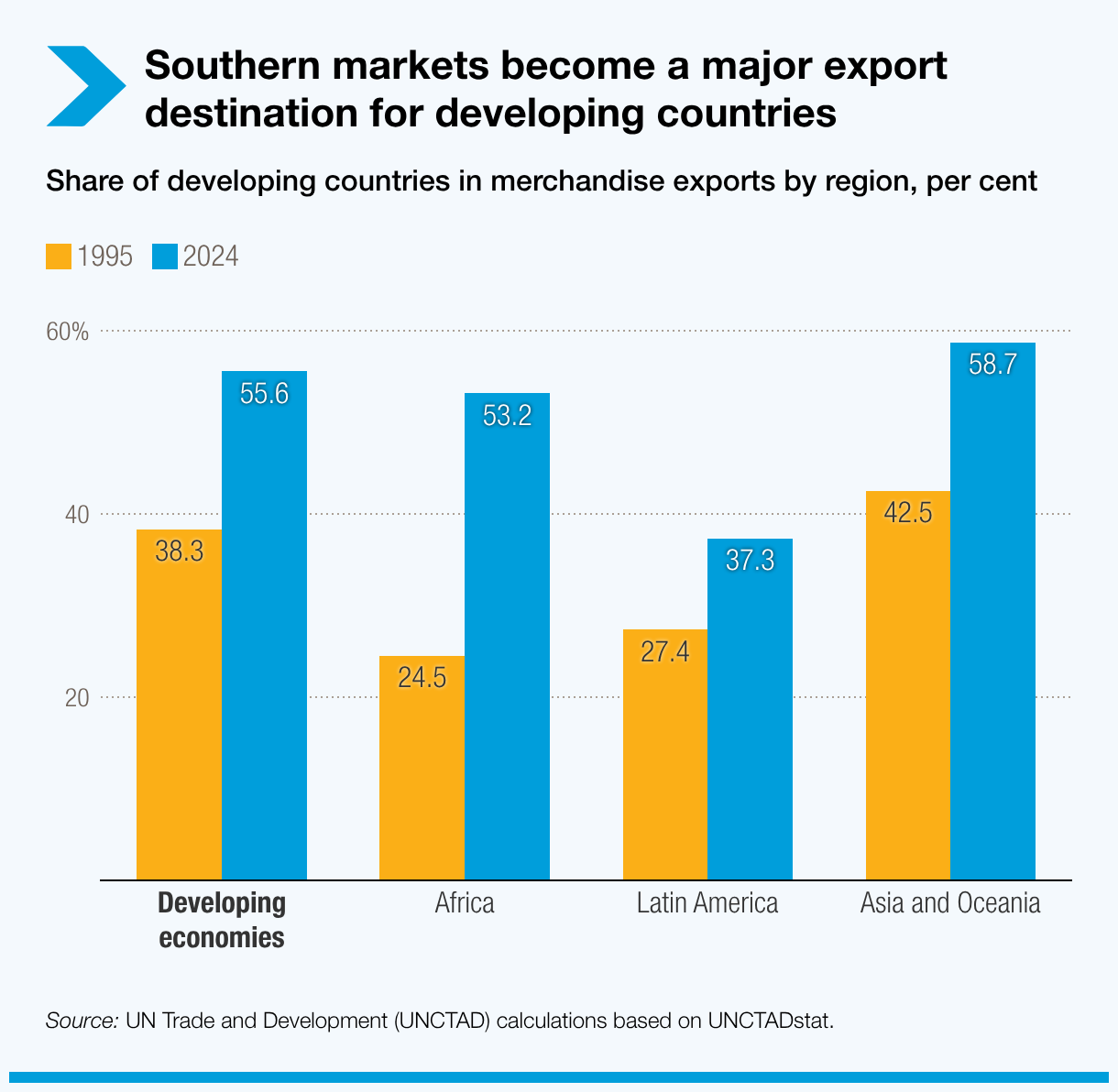

6. South–South trade surges as developing countries drive export growth

South–South trade – trade between developing countries – has become a major engine of global trade growth. Between 1995 and 2025, South–South merchandise exports surged from about $0.5 trillion to $6.8 trillion. Today, 57% of developing-country exports go to other developing economies, up from 38% in 1995.

- The surge has been driven largely by Asia’s regional value chains, particularly in East and Southeast Asia, where high and medium-tech manufacturing dominates.

- South–South trade is also deepening elsewhere. More than half of Africa’s exports now go to developing markets.

As demand growth weakens in advanced economies, South–South trade is likely to expand further. Strengthening regional and interregional links – especially between Africa and Latin America – could boost resilience across global trade networks.

7. Environmental concerns remain a key part of global trade initiatives

Environmental priorities are increasingly shaping global trade as climate commitments move into implementation. Enhanced pledges by 113 countries could cut global emissions by about 12% by 2035.

Clean-energy technology markets could reach $640 billion a year by 2030, accelerating trade in green goods and services. Climate and trade are converging through:

- Carbon pricing and regulation, including the European Union’s carbon border mechanism from 2026

- Clean-energy industrial policies, reshaping market access and competitiveness

For developing countries, access to green finance, technology and technical assistance will be critical as environmental standards tighten.

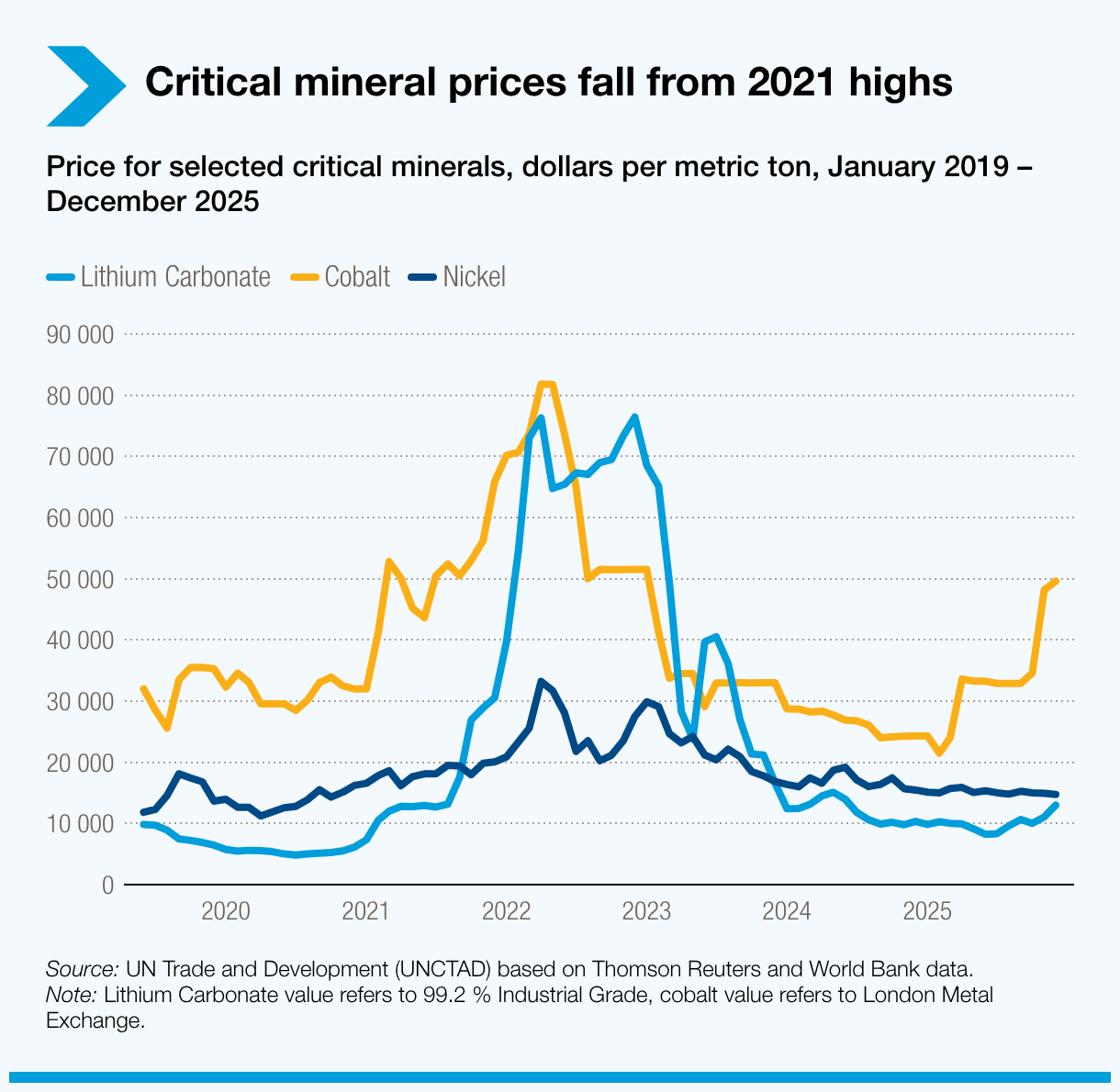

8. Critical minerals face volatility amid oversupply and geopolitical risks

By late 2025, prices of key clean-energy minerals were 18% to 39% below their peak 2021-22 levels, reflecting oversupply, slower battery demand and technological shifts that reduce mineral intensity.

Lower prices have eased costs for electric vehicles and renewables, but are weighing on investment:

- Mining investment growth slowed to 5% in 2024, down from 14% in 2023 and 30% in 2022

- Financing remains focused on near-mine projects, with limited appetite for new greenfield development

Despite lower prices, supply risks remain. Export controls have tightened, including cobalt restrictions in the Democratic Republic of the Congo and rare-earth controls in China. Countries are responding by stockpiling and striking bilateral deals, increasing the risk of fragmented value chains. Resource security will remain a strategic trade issue in 2026.

9. Agricultural trade remains vital for food security

Food and agricultural products account for around one third of commodity exports, with food products making up nearly 87%. Many developing countries rely on imports to meet basic needs.

Food markets remain highly vulnerable to shocks:

- Conflicts, trade restrictions and extreme weather continue to disrupt supply.

- Droughts and floods are reducing yields and increasing price volatility.

- Fertilizer prices surged in 2025 and remain high, raising production costs.

Developing countries are particularly exposed, with limited fiscal and policy buffers to absorb price spikes. Keeping food trade open will remain critical to food security in 2026.

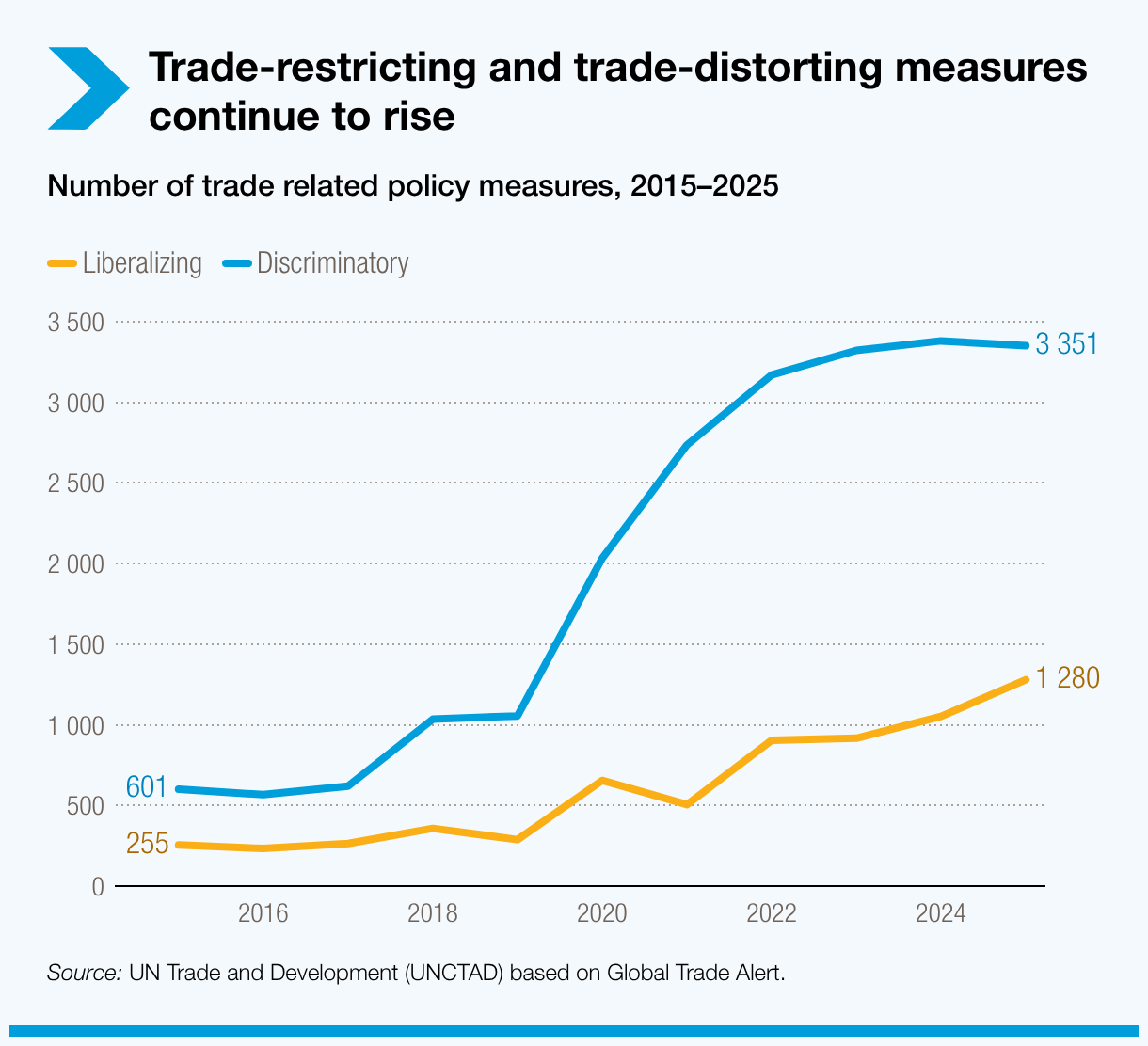

10. Trade regulations tighten as national policies reshape commerce

Trade-restricting and trade-distorting measures are on the rise as governments use trade policy to pursue domestic goals. Since 2020, around 18,000 discriminatory trade measures have been introduced. Technical regulations and sanitary standards now affect about two thirds of world trade.

Regulatory pressures are coming from multiple fronts:

- Security and industrial policy, including strategic trade controls.

- Environmental measures, such as carbon border taxes and deforestation-related rules.

- Social and public health standards, adding new compliance requirements.

In 2026, non-tariff measures are expected to expand further. While often addressing legitimate objectives, their impact will fall unevenly, with smaller exporters and lower-income economies facing the highest compliance costs. Flexible rules and targeted assistance will be key to keeping trade inclusive.

Navigating a more fragmented trade landscape

As these dynamics evolve, timely data, analysis and policy support will be critical. UN Trade and Development will continue to track these shifts and support countries in navigating change, managing risks and identifying opportunities in an increasingly fragmented trade environment.