Shifts in financial markets move global trade almost as strongly as real economic activity, influencing development prospects worldwide.

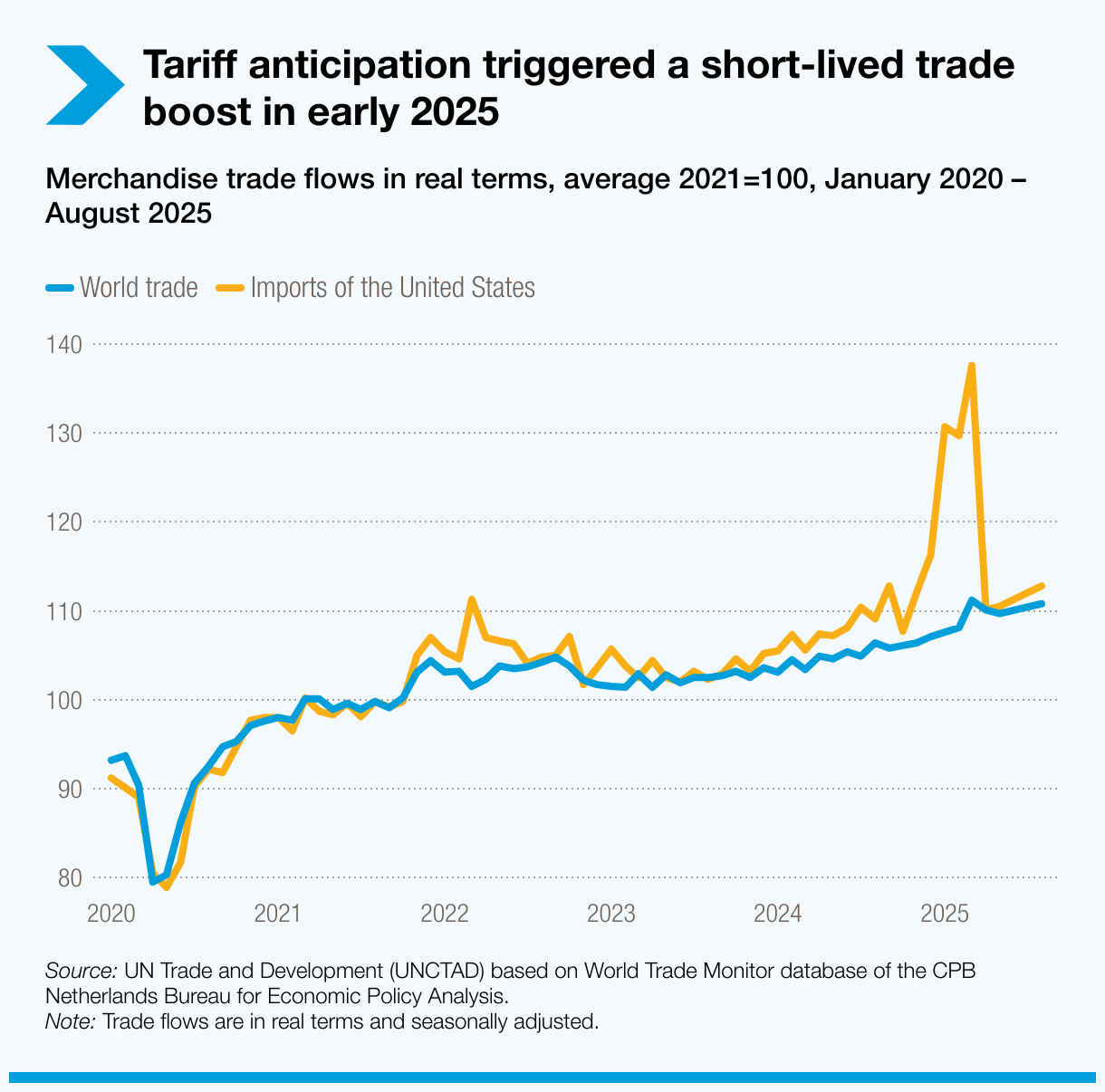

World trade began 2025 with what looked like a rebound. Shipments jumped as firms rushed to beat new tariffs in the United States, and investment in artificial intelligence gave an extra lift.

But once you remove these temporary boosts, the picture changes. Trade growth in the first half of the year drops from 4% to between 2.5% and 3% – and a slowdown looms on the horizon.

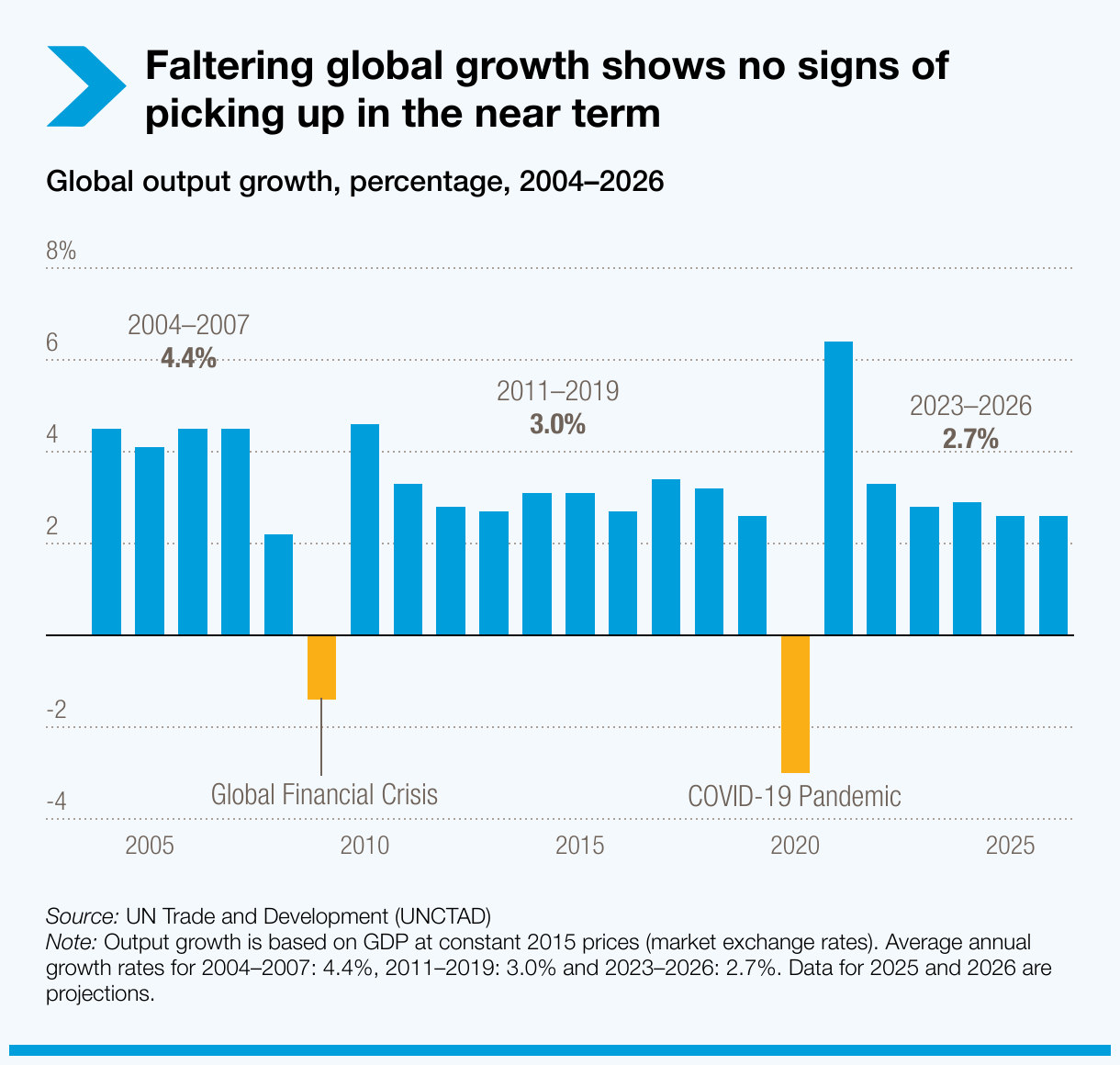

The wider economy tells a similar story. The Trade and Development Report 2025 projects global economic growth to slow from 2.9% in 2024 to 2.6% in both 2025 and 2026. This is below the pre-pandemic trend of 3% and far below the 4.4% average growth seen before the 2008-2009 financial crisis.

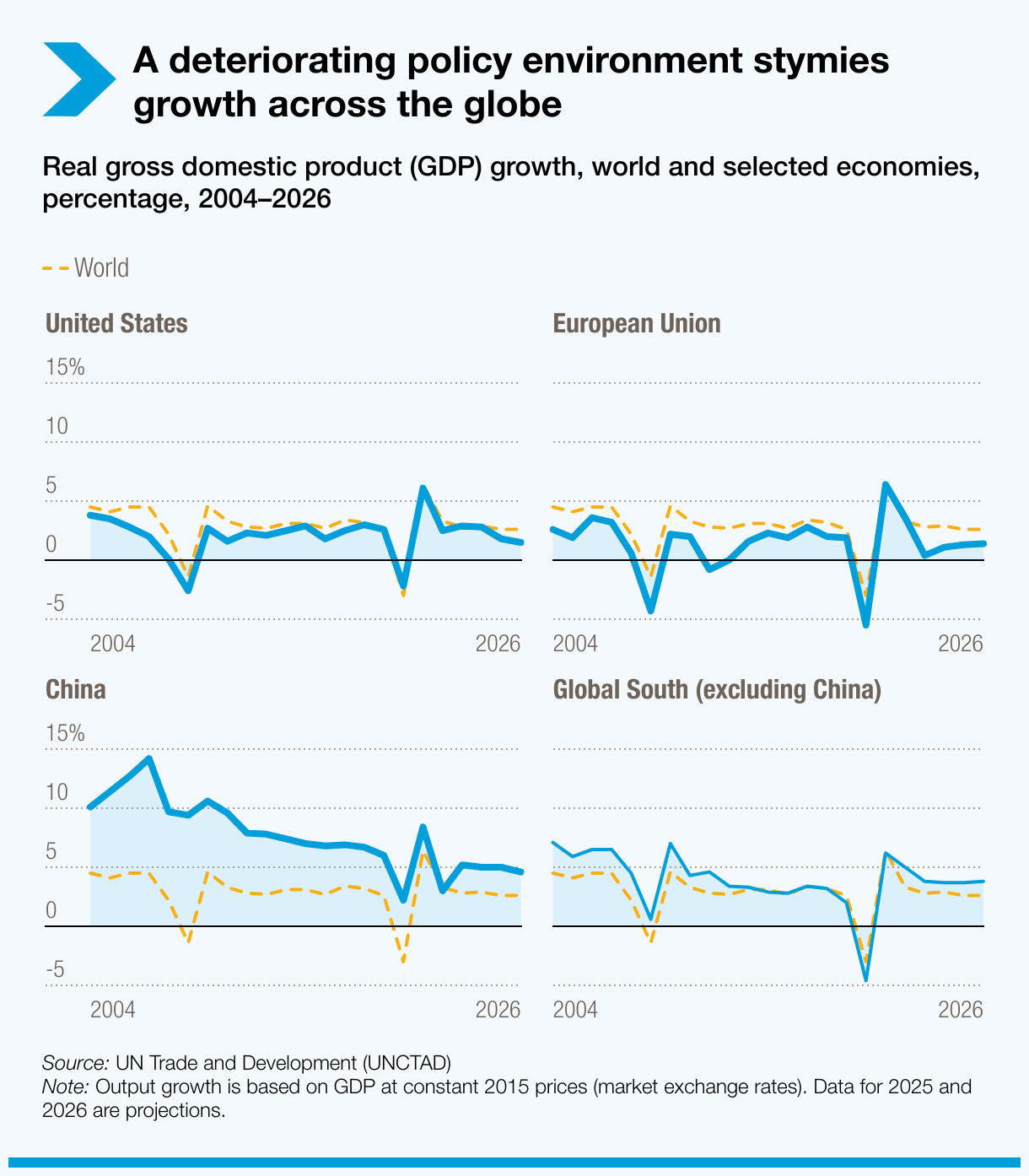

Major economies are also losing steam. In the US, economic growth is expected to slow to 1.8% in 2025 and 1.5% in 2026. China’s economy is slowing, too. Its growth is projected to fall from 5% in 2025 to 4.6% in 2026, down from an average of 6.7% in the years before the pandemic.

The resilience seen at the beginning of the year now looks much thinner.

Trade and finance increasingly move in sync

When we think about trade, we picture ports and shipping routes. But behind every shipment is a credit line. Behind every container is an exchange rate. And behind every trade route is a network of banks.

Today, more than 90% of world trade relies on trade finance. Banks, payment systems and financial instruments like derivatives increasingly determine who can trade, on what terms and at what cost.

Because of this, trade has become more sensitive to financial factors like changes in interest rates and shifts in investor sentiment.

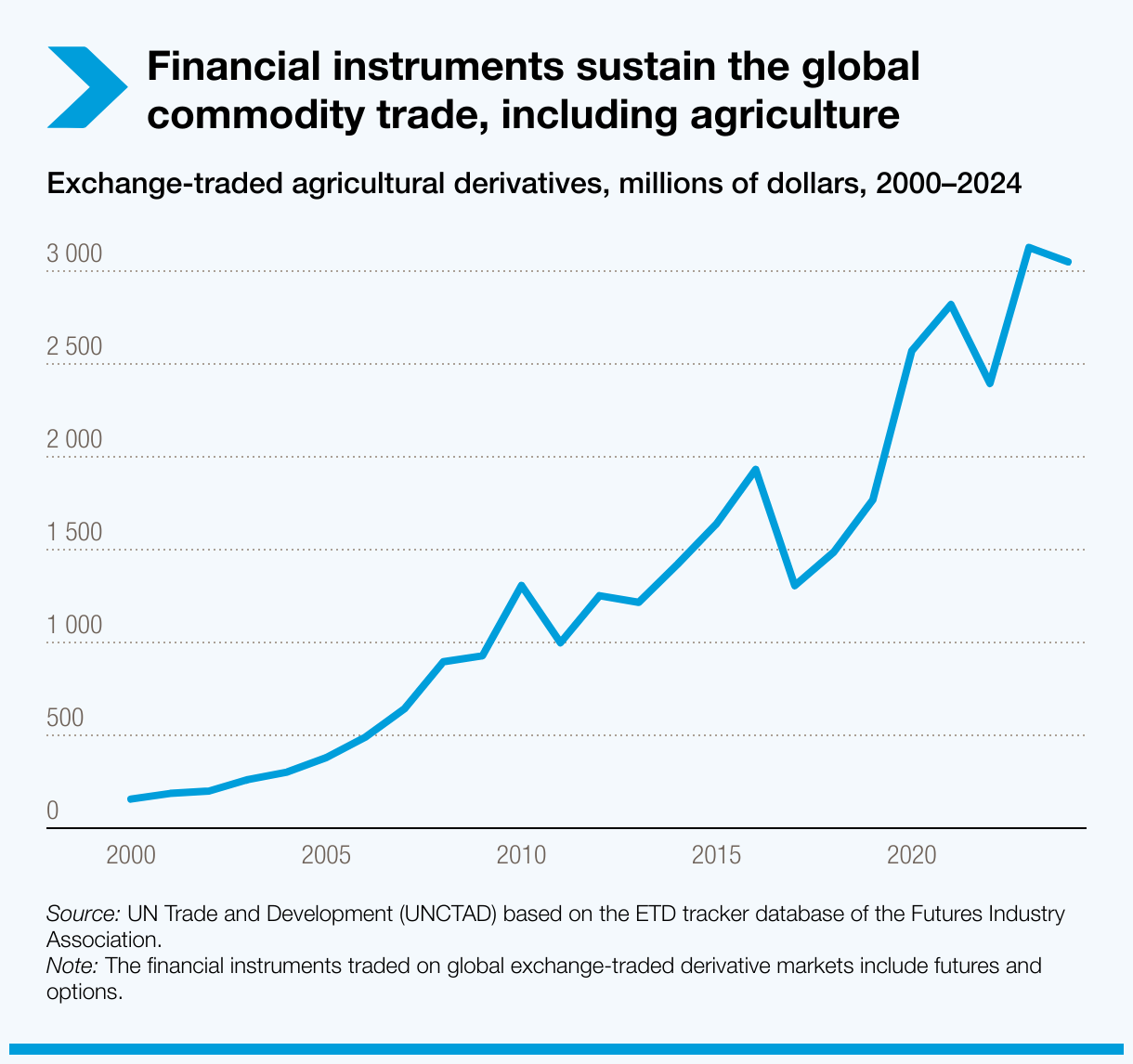

The tight link is clear in food markets. Over 75% of major food-trading companies’ income now comes from financial operations like agricultural derivatives – not from moving wheat, coffee, cocoa or other agricultural products.

When finance drives trade, vulnerabilities grow

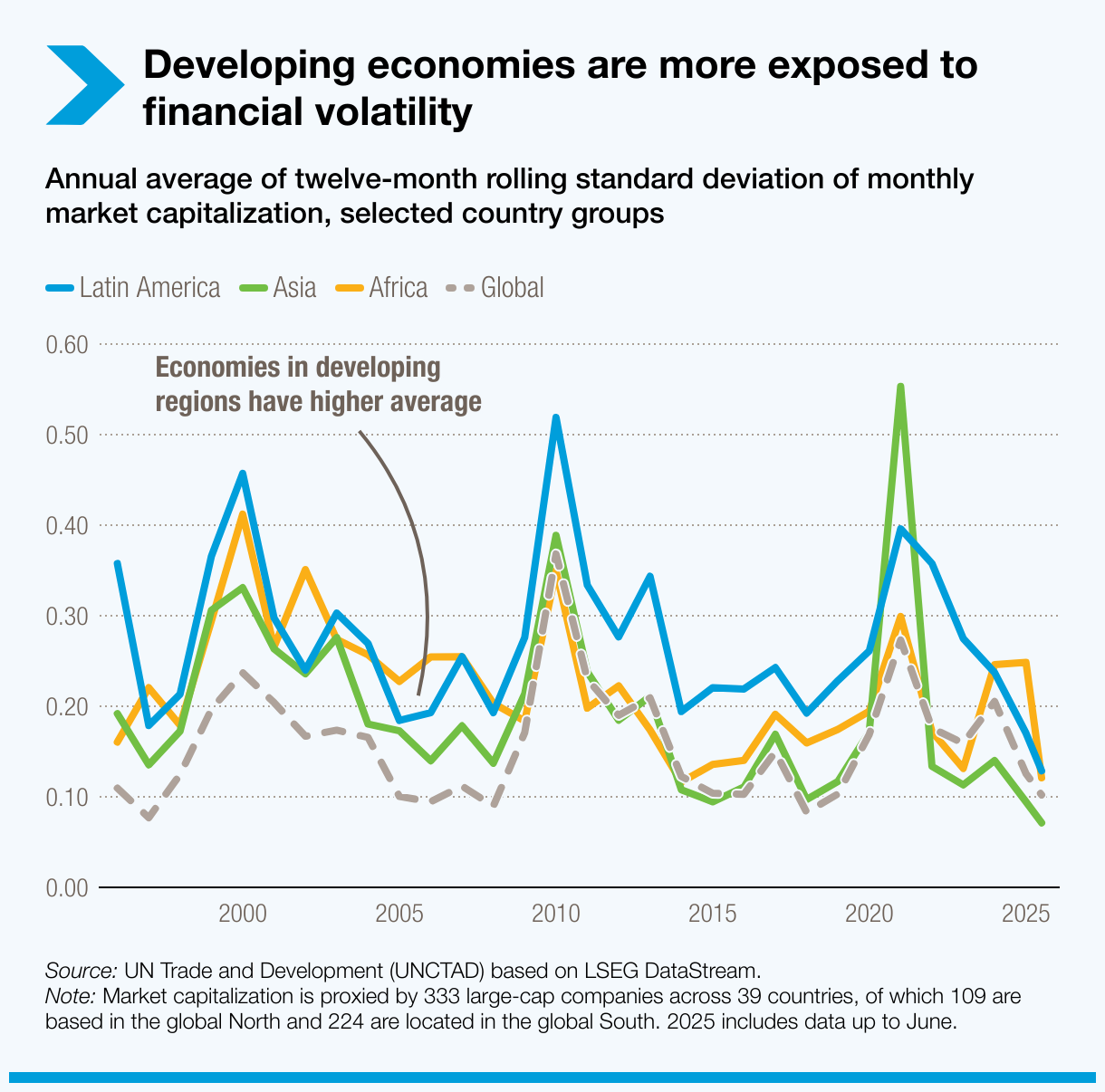

For developing countries, the growing role of finance in trade brings real vulnerabilities. Currency swings make imports and debt more expensive. Shifts in global risk appetite can cut off credit. And financial volatility tends to hit their markets harder and more often.

When prices move on financial signals rather than real economic conditions, their companies and producers compete on a more uneven playing field.

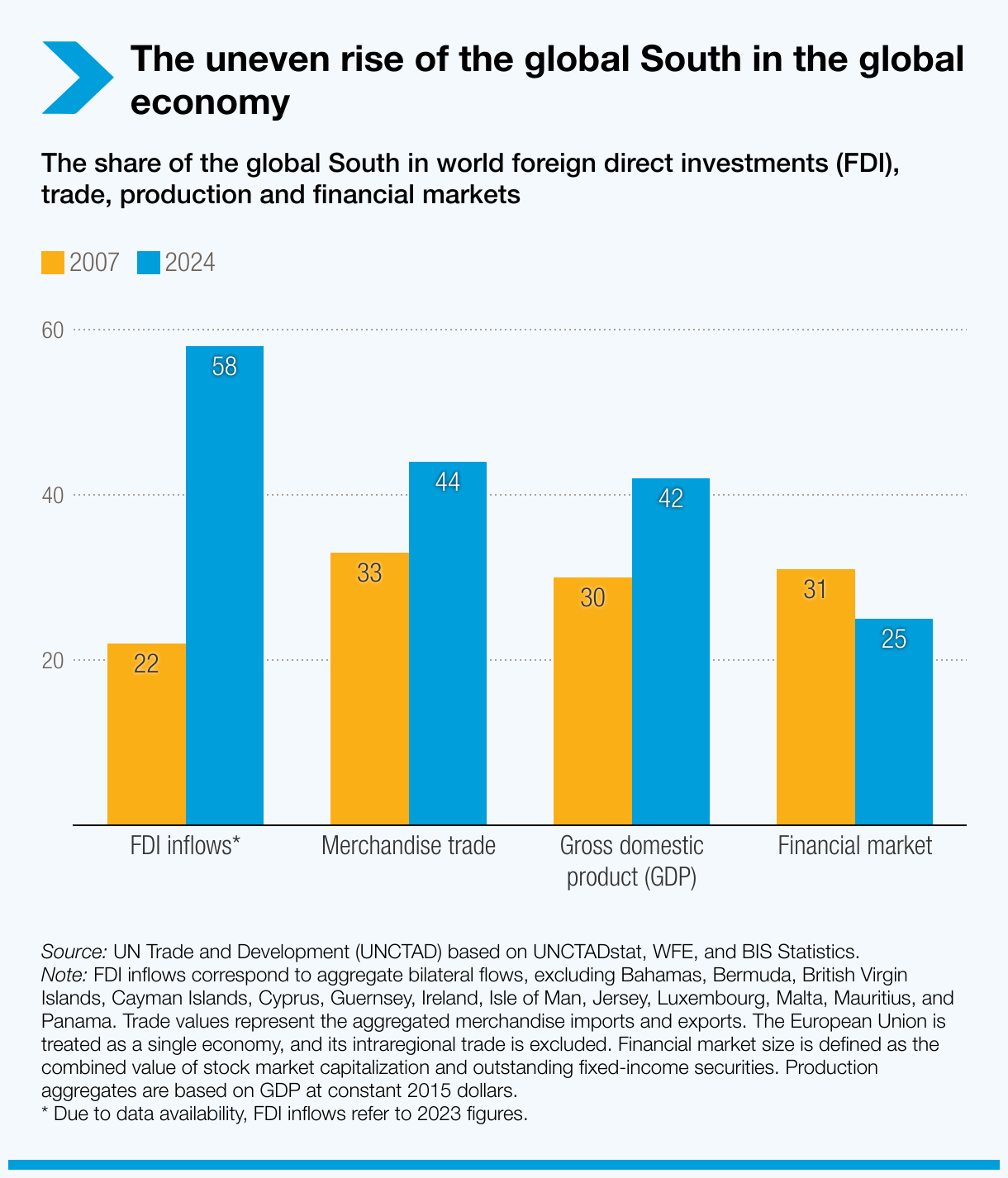

The UN Trade and Development report highlights a widening gap between developing countries’ growing weight in the world economy and their limited role in global financial markets.

They now account for over 40% of global output and merchandise trade, and attract nearly 60% of global foreign direct investment (FDI). Yet developing countries hold just 25% of global financial market value.

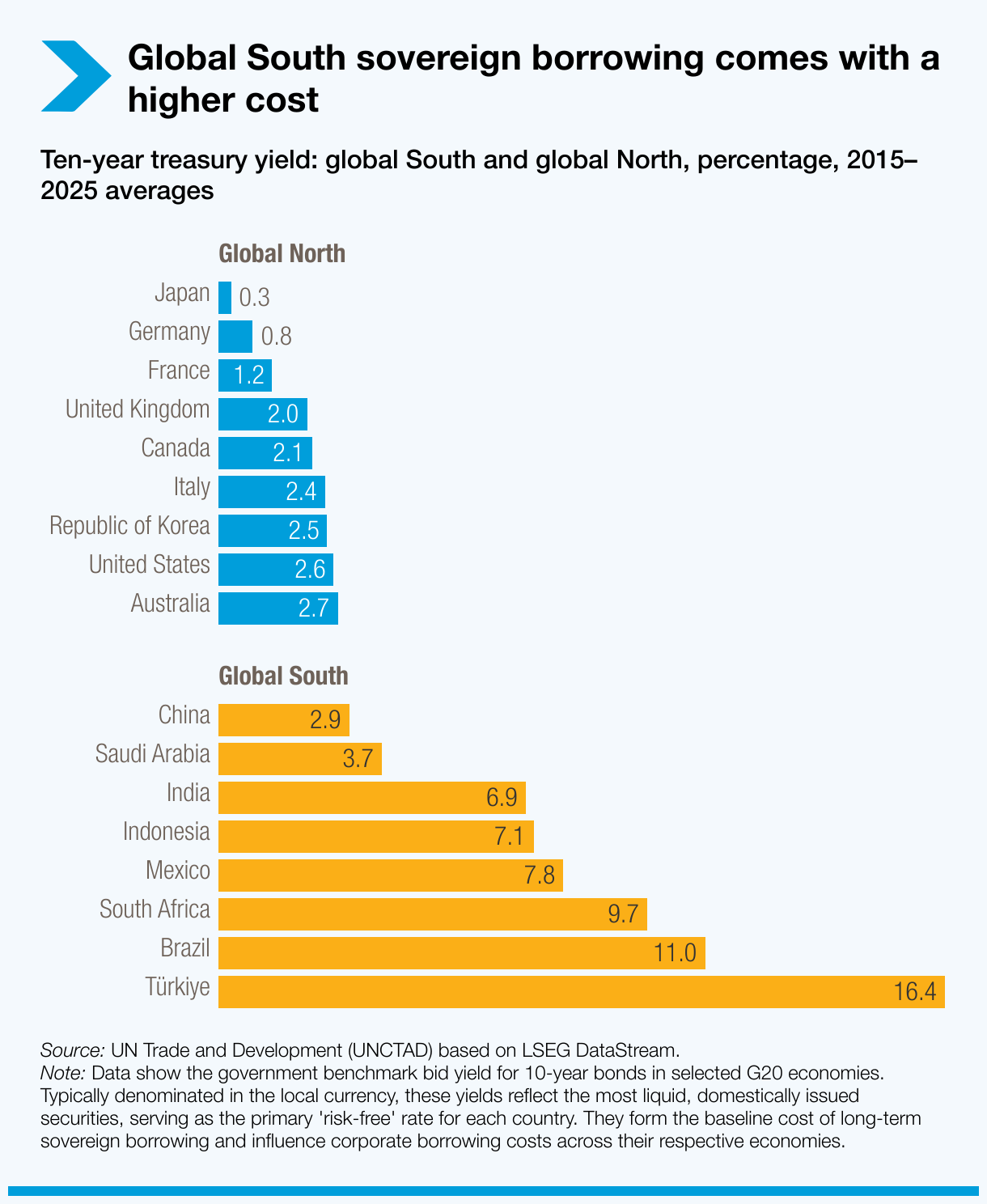

Their smaller and less liquid capital markets make it harder for firms to raise money. Many developing countries also remain dependent on foreign banks, paying higher and more volatile interest rates. Advanced economies typically borrow at 1% to 4%, while many emerging markets pay 6% to 12% for similar government bonds.

These higher costs undermine investment in infrastructure, innovation and climate resilience.

Targeted reforms needed to strengthen resilience

The Trade and Development Report 2025 outlines a set of practical reforms to reduce financial vulnerability and better align trade, finance and development. These include:

- Fixing the multilateral trade dispute system so rules are enforced and uncertainty is reduced.

- Closing data gaps on trade and investment statistics to better inform and coordinate policies.

- Reforming the international monetary system to limit harmful swings in currencies and capital flows.

- Strengthening regional and domestic capital markets so developing countries can raise affordable long-term finance.

- Improving transparency in commodity trading and expand access to affordable trade finance, especially for small businesses.

True economic resilience requires strategies that connect trade, finance and sustainability – and ensure developing countries can shape global economic shifts, not just absorb them.